(B)(N) The Federal Bank Casino Market

The Federal Reserve Bank in New York

Drama. They say that investors are getting ready to pull the trigger and sell their long-term (30 years) government bond holdings and shorter term (months to maybe ten years) treasury bills because they sense (hope, pray) that interest rates are going to go up and they expect that the demand for new debt in mortgages and government spending (and not so much in corporate bonds) will increase as the government tapers-off its buying program for “quantitative easing” and begins to sell what it has in the float market and if the interest rates are rising, the prices on these old debts will need to fall for ready cash (Bloomberg, April 9, There’s a Big Reason Volatility Might Be Coming Back).

But we’ve used the term “investors” guardedly because these folks aren’t investors at all and they are quite literally betting their sizable capital – which is mostly our money in pension plans – on basis-points sized spreads in yields to get an income in capital gains on their (our) money because 50 basis points doesn’t buy a lot of bread.

We’ve also tried to dumb-down this equation (as above) without going into the details of mortgage-backed securities and the global government bond and treasury bill and currency exchange rate markets which are all and only about speculation, big bets, and good luck or not, as “investors” try to get an income on their money that is not just an interest income counted in basis points.

But all investors have the same problem – if they can’t get an income on their money that somebody else pays for in their investments then they might have to spend their own money (their capital) to pay their bills and, before they know it, they might be dropped-off or demoted on the Forbes Billionaires List.

The Federal Bank Casino Market

We’re not really interested in this market because we have a World Market in real equities (which these folks call the “risk market” for some reason) in which a week of the daily float dwarfs all of their yearly concerns for money and, of course, treasury bills don’t pay dividends or have a coupon and so all of their work is about making money from each other; please see our recent Post on (P&I) The [New] Power Law & Volatility Smile.

However, we can work this market of bonds as easily as we work the equities market with just a stock chart, a ruler, and a good eye because the principles and drivers are exactly the same – how do we obtain an income on our money with 100% capital safety guaranteed – and these investors have a “solution” which doesn’t work except by chance and we have another solution which always works as long as we have them and their chance and the long/short portfolio in these bonds has tripled our money in the five years since 2012 for an average return of +25% per year while they’ve been sitting on their basis points and waiting for tomorrow and another chance because the investors, despite all of their sophistication (please see below), don’t have any idea what the yield is at any time.

Please see Exhibit 1 below for an example using the Germany 10-year Treasury Bond Yields (and click on it and again to make it larger as required) and the Appendix below for an explanation of the price of risk and why this always works.

Appendix A: The Nash Equilibrium and its Stock Price

The “Nash Equilibrium” finds the extreme outcomes of repeated cooperative (that is, enforceable) and non-cooperative bidding processes; we’ll prove the theorem below and, then, what it found.

If (X) is an array of all of the bid and ask “prices” for one “company” or many, perhaps all of them, then a Nash Equilibrium is obtained when the market is cleared as the prices in (X) are moved from one position to another in successive bidding and asking until there is no “economic free good” that is acquired by any of the parties; that is, no party can make further gains without a “loss” to at least one other party and “gains” and “losses” are not necessarily linked only to money but they are defined by the choices that the parties make in order to improve their position with respect to the “company” which could be just a set of “values”; for example, bidding on the ownership of a coal producer is not only about money if one of the parties is bidding to own the company (and, therefore, all of the stock or none of it) in order to close it down but other investors are bidding to keep it open.

In order to prove the Nash Theorem, suppose that (X) is an array of bid and ask prices that we will call an “offer”; a “counteroffer” to the offer (X) is an array with content similar to that of the offer (X) in which every investor in (X) has improved their position relative to the offer that they made in (X) and, in general, for every offer (X) there will be many counteroffers so that the mapping from an offer (X) to counteroffers is “set valued” with results that are similarly structured to (X) and which all look like “offers”.

The Nash Theorem (1950) then says that with two other conditions on offers, there will always be an offer that is in the set of its counteroffers and which, therefore, cannot be improved upon and it is, therefore, the “best offer” although there will also be, in general, many “best” offers and the investors are necessarily indifferent as to which one is implemented.

The two additional requirements without which the result is provably false, are that if (X) and (Y) are offers, then (Z) = λ(X) + (1-λ)(Y) is also an offer where λ(X) means “some of (X)” and (1-λ)(Y) means “a complementary amount of (Y)” and we can say that the set of offers is “convex” with that meaning.

We also note that if (X) is an offer then the set of counteroffers to (X) is a non-empty set (because if (X) cannot be improved, then it is the best offer) and convex in the above sense; that is, if (X1) and (X2) are both in the set of counteroffers to (X) and both improve on (X), then, as above, “some of X1” and a “complementary amount of X2” will also be an offer that improves on (X).

The second condition is a notion of “continuity”, if (Xn) is a sequence of offers that “converges” to an offer (X) and (Yn) is a sequence selected from the counteroffers to the (Xn) and (Yn) converges to the offer (Y), then (Y) is in the set of counteroffers to (X) and the notion of “convergence” is defined by indifference; in other words, (X) is common to all but finitely many of the (Xn) and (X) is also contained in infinitely many of the (Xn) (which are the usual lim inf and lim sup definitions for sets to “converge” but “infinite” is only a boundary condition in our situation of finitely many companies and investors).

With those two conditions, the set-valued “Fixed Point Theorem” of Shizuo Kakutani (1941) assures that there is always an intersection between the offers and the counteroffers, as required.

The Preference Relations Defined by the Price of Risk

The Nash theorem provides us with an “existence” proof, but what is it that “exists” in our case?

It is the “price of risk” which we have defined as “the least stock price at which a company is likeable” and the evidence for “likeability” is that investors who own the stock prefer cash now to owning the stock and investors who have cash now are prepared to buy the stock at that price and the situation is, obviously, conflicted because the investors who are selling might have to sell for reasons of liquidity or they might have other options to meet that requirement (which will generally be true) and they will not sell if the price is too low; and, similarly, investors who have cash will not buy the stock (in most cases but not always because “low” and “high” are generally subjective) if the price is too high but having bought the stock and made that decision, they might very well be willing to buy more depending on their cash and their needs for it (although that is only an expectation and not a requirement but we often see it in “momentum” buying).

In effect, a trade at the price of risk implies that the seller is happy, but not too happy, and that the buyer is also happy, but not too happy and the same could be said if we replace the words “happy” with “unhappy” in both cases which is exactly how we state the “enforceability” requirement in “cooperative games” for our purpose.

In order to “monetize” that preference relationship and enforce the notion of “happy, but not too happy” and at the same time, “unhappy, but not too unhappy”, we need to refer to the Theory of the Firm (please see the references) which develops “economics” from the very simple basis of the “societal standards of bargaining practice and risk aversion” that are demonstrated in the debt or equity transaction that we might make as opposed to holding cash; cash guarantees our liquidity now but probably (almost certainly) not in the future as long as there is an economy in which we can make that decision between holding cash and holding an investment of our cash that (we hope) means more cash later.

To solve that problem, we need to answer this question: If the investors or owners have (N) and the bond holders have (B) and the investors approach the bond holders to strike a new deal with respect to forming or buying a company, or to restructuring the debt of the company that they own, what is the best outcome within the demonstrated societal standards of risk aversion and bargaining practice?

The question appears to be one-sided in that the “investors or owners” with (N), an equity, basically, are approaching the owners of cash to join them in their enterprise in the context of the bond holders (B) who have already done so and, therefore, have already made that decision to join them but to see the other side, we note that the equity holders (N) have an enterprise which is or has the possibility of producing more cash and, of course, “more cash” will reduce the purchasing power of the holders of cash who are not producing more cash and, so, it should not be surprising that the owners of cash might be receptive to that idea and might even initiate it, in which case the equity holders need to think about what that means for their earnings in the enterprise which they own in lieu of more cash now.

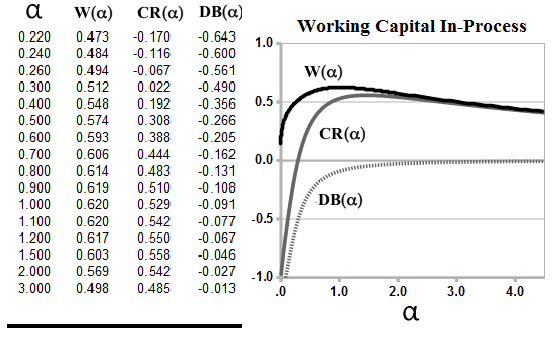

The solution to that problem is the Theory of the Firm in which we develop the “N/B/W” – Financing Model in which the new factor, W, is the unsecured “working capital” that we can expect to acquire for a firm with equity (N) and bond debt (B) in the context of “the societal standards of bargaining practice and risk aversion” and we don’t need to “speculate” on its value – we can calculate it based on what is actually done, but there are also reasons (please see below) that it has the values that it has and none other and so it is not just a matter of “data” although we could also call-up our banker and they will verify that if they want to stay in business; please see Figure A-1 below.

Figure A-1: The Working Capital In-Process

The Theory of the Firm is an abstraction in which the firm values are between 0 and 1 “in process” and neither of the boundary values are ever actually obtained; in the chart above, the parameter α is the entropy of the process which is described only in terms of the payables and receivables of the firm coming to cash that can be attributed to the firm and its trading connections (neither exists without the other); CR(α) and DB(α) are the “cash value” of the credit and debit “float” and the “Working Capital” W(α) = CR(α) – DB(α) is their difference; it’s similar to the “working capital” defined by the accountants but in our case, “time” is defined by systemic growth in process, not clocks.

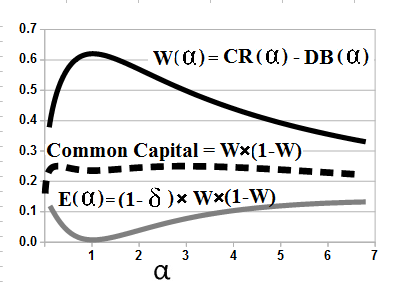

However, we’re still not done because in order to ensure the “convexity requirement”, we need to go beyond W to “indifference” which is the “common capital” (W)(1-W) and the “credit” that is equally accessible to all of the parties – cash, (N), (B), firm, and the trading connections – and, therefore, not of any special value to any of them but it can be used by an “enterprise” (which we define below as the Coase Dividend) to “create” the working capital W that it requires for its own growth and success as long as there is an enterprise and an “economy” and the “investors” all have the same decision – is their cash “worth” (a subjective reduced to a hard currency) as much to them as the same cash is to the enterprise?

Figure A-2: The Common Capital

Delta, δ = log(1 + GW*) where GW* is the “balance sheet worth of the trading connections” (Coase) and it is the result of working the working capital forward as GW* = W/(1-W) = W + W² + W³ + ….; the quantity, E(α) = (1- δ)×W×(1-W), is the lowest “unit” of exchange and we think of it as the “first penny” or hard unit of exchange that is created in this economy; it is the discounted value of the common capital by the growth constant (or “rate of interest”), δ, and we also note that there is very little variation in the common capital which tends to be about 25% of the combined net worth (N) and bond debt (B) of the “firm” that we started with and the quantity, GW*, monetizes the “intangible” described by Ronald Coase:

“In order to carry out a market transaction it is necessary to discover who it is that one wishes to deal with, to inform people that one wishes to deal and on what terms, to conduct negotiations leading to a bargain, to draw up the contract, to undertake the inspection needed to make sure that the terms of the contract are being observed, and so on. These operations are often extremely costly, sufficiently costly at any rate to prevent many transactions that would be carried out in a world in which the pricing system worked without cost.” – Ronald H. Coase 1960, The Problem of Social Cost, Journal of Law and Economics.

We have developed and documented the Theory of the Firm in the references below; however, there is a simpler definition in terms of general processes, (a) and (b), which define each other if they have the same entropy, one with respect to the other, as Ω(a;b) = – ∫ a×log(a) db and Ω(b;a) = – ∫ b×log(b) da on the probability measures (a) and (b) in the usual sense and we can say that they are “in process” if α = Ω(a;b) = Ω(b;a) is their common entropy and the necessary and sufficient condition for that is the two “Power Equations” a × log(a) = α × log(b) and b × log(b) = α × log(a); there are also two boundary conditions that enforce the Theory of the Firm and, in general, whenever there is a “Conservation Law” such as the balance sheet in our case.

References:

[1] Nash, J.F. 1950. “Equilibrium Points in N-person Games”. Proceedings of the National Academy of Sciences. 36.48-49.

[2] Nash, J.F. 1950. “The Bargaining Problem”. Econometrica. 18:2.155-162.

[3] Kakutani, Shizuo. 1941. “A Generalization of Brouwer’s Fixed Point Theorem”. Duke Mathematical Journal 8:457-459.

[4] Border, Kim C. 1985. Fixed Point Theorems with Applications to Economics and Game Theory. Cambridge, UK: Cambridge University Press.

[5] Tobin, James. 1958. “Liquidity Preference as Behavior Towards Risk”. The Review of Economic Studies. 25:2.65-86.

[6] Coase, R.H. 1960, “The Problem of Social Cost”. Journal of Law and Economics.

[7] Coase, R.H. 1937. “The Nature of the Firm”. 4 Economica 386.

[8] Rubinstein, A. 1982 “Perfect Equilibrium in a Bargaining Model”. Econometrica, 50:1.97-110.

[9] Halmos, P.R. 1950. Measure Theory. New York. D. Van Nostrand Company.

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy, UFOs and the High Flying Techs, and The Coal War which is heating-up again now; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that as well as The Great Rotation & Twenty Hot Canadians 2017.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.