(B)(N) Extreme Economics – Green Energy

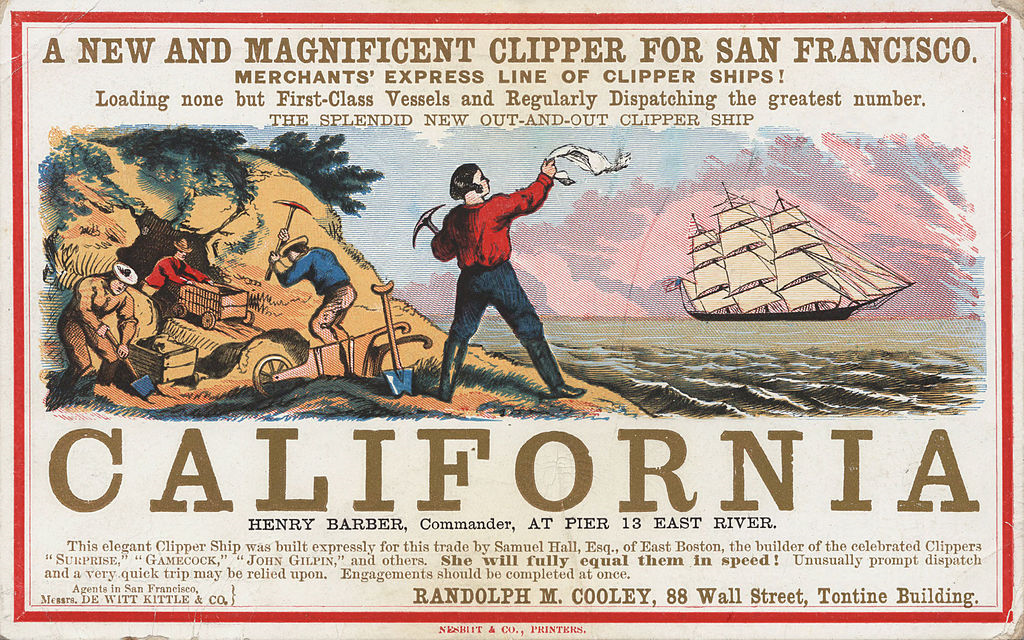

Figure 1: California Here We Come 1849

Drama. The rush to “Green Energy” is already a crowded space and it’s not unlike the California Gold Rush of 1849 which drew over 300,000 fast gold-diggers into California from all over the World before California was even a state (1850) and before there were laws to decide who owned what, when, and how.

The “Green Energy Rush” is like that and also like the microchip revolution that began in the 1980s (Moore’s Law) and we can now buy a terabyte (1,000 gigabytes) of data storage for less than $100 off-the-shelf and 100 of those will store the Library of Congress for us.

But “Green Energy” today is an industry with a mostly negative return on the shareholders equity that barely breaks even in aggregate and doesn’t pay any dividends to speak of; and it’s an industry that is sometimes wildly inflationary in the same way as, for example, Brazil and Argentina, and sometimes in a deep depression that is worse than that of America in the 1930s; and it’s an industry in which the (B)-class portfolio returned more than +800% in the last five years and we will do it again in the next five years.

And our problem today is to solve that problem.

The Green Energy Economy

Figure 1 And it comes in attractive roof tiles too.

The industry has hundreds of publicly-listed firms and also offers lots of entrepreneurial opportunities for engineers, construction firms, and roofers in privately owned firms whereas natural gas or gas liquids, coal, hydroelectric, and nuclear-powered plants are waning and a tough sell to governments everywhere when it’s easy to imagine a wind farm or a solar roof on every house and independence from the national grid for every home.

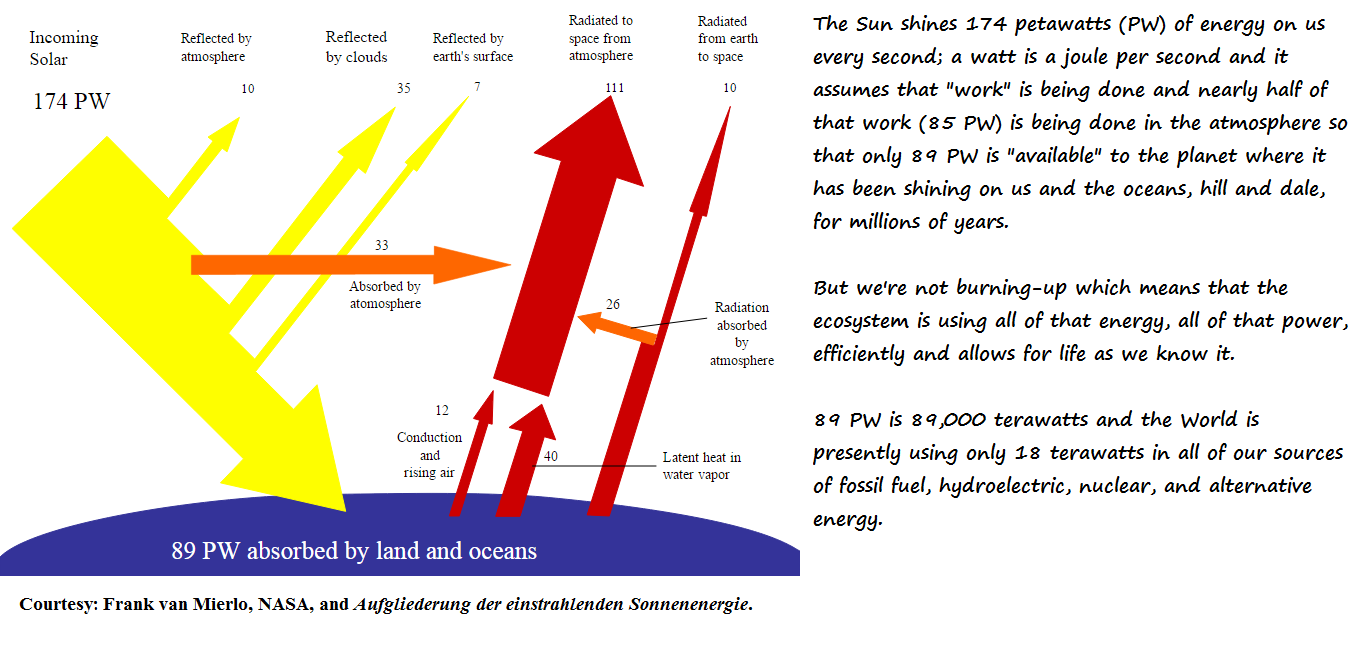

Figure 3: NASA and the Germans are really on top of this.

But there is a problem – neither wind nor solar can replace the energy that we need from fossil fuels, hydro, or nuclear and a “fan” on every street and a “cell” on every roof will change our environment and the Sun doesn’t give us any “surplus” power because if it did, we’d be like Mercury or Venus and if less, like the far side of the Moon; please see Figure 2 and 3 on the right for more details (and click on it and again to make it larger as required).

And like the California Gold Rush, there are diggers, miners, and mines, and a “service industry” that hooks it all together, and we need to think about how we’re going to invest in that and not freeze our assets (so to speak).

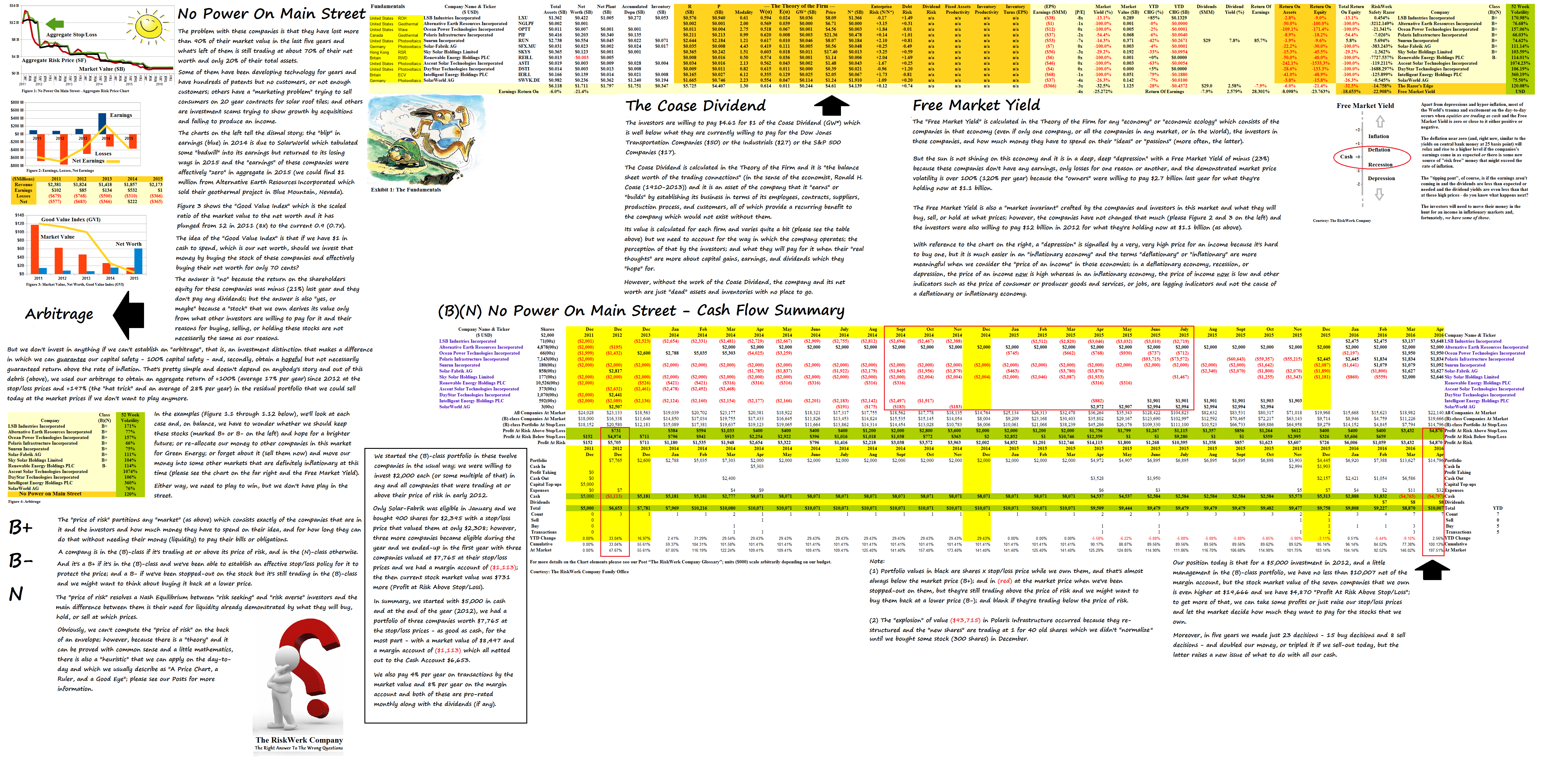

No Power on Main Street

How does a $200 stock become a 10 cents stock for a company that makes and sells solar battery chargers (ASTI Ascent Solar Technologies Incorporated); or a $800 stock that makes “thin film copper indium gallium diselenide (“CIGS”) solar products” become a 5 cents stock with 10 employees (DSTI DayStar Technologies Incorporated)? And vice versa.

We have over 160 Green Energy companies in our global World Trade portfolio and they divide into services such as AC/DC converters and storage; applications such as cars and solar-powered telephones and clothing; and producers in bio-renewables, fuel cells, free-running water, solar, and wind; and these divide further into financial “sink holes” and also into proven viable firms in each segment (as above) and with an independent stock market performance that has next to nothing to do with whether these companies are “good” or not.

We’ve pulled-out a dozen (of more than forty) of the most bizarre cases of companies that are still trading and listed in the stock exchanges and we don’t have any idea of whether these companies have ever been “good”, are “good” now, or will ever be “good” again, past, present, or future.

But that’s not the point – the issue is can we invest in them with 100% capital safety guaranteed and a hopeful but not necessarily guaranteed return above the rate of inflation – and what can we do to make sure that that is so?

For example, the (B)-class portfolio in these companies has done the “hat trick” and tripled our money (+197%) since 2012 at the current market prices of our residual portfolio; please see Exhibit 1 below.

But, more importantly, we returned +100% at the current and realized stop/loss prices since 2012 even as the combined market value of these companies has plunged from $15 billion in 2012 to the current $1.5 billion and the “investment” problem now is the same for these companies as for any other portfolio because we don’t have to know the difference between good, bad, or indifferent companies – our only interest is in what the market will pay for them now.

Exhibit 1 is a tutorial on bad investors in a difficult market; to turn these companies around we would have to buy control and bring in some new management and attitudes.

Figure 4: More Power On Main Street

Not to be discouraged, we played our game in the broader market for Green Energy (110 companies in more than a dozen countries) and we killed this market – we murdered it – with +815% in dividends and capital gains at the stop/loss prices (that’s an average of 67% per year) in five years.

And we’re going to keep on doing it because the current portfolio has an interest in more than half of them and there’s no reason for us to change our policy; please see Exhibit 2 below for more details.

Exhibit 1: No Power on Main Street

|

Figure 1.1 LXU LSB Industries Incorporated (B+) |

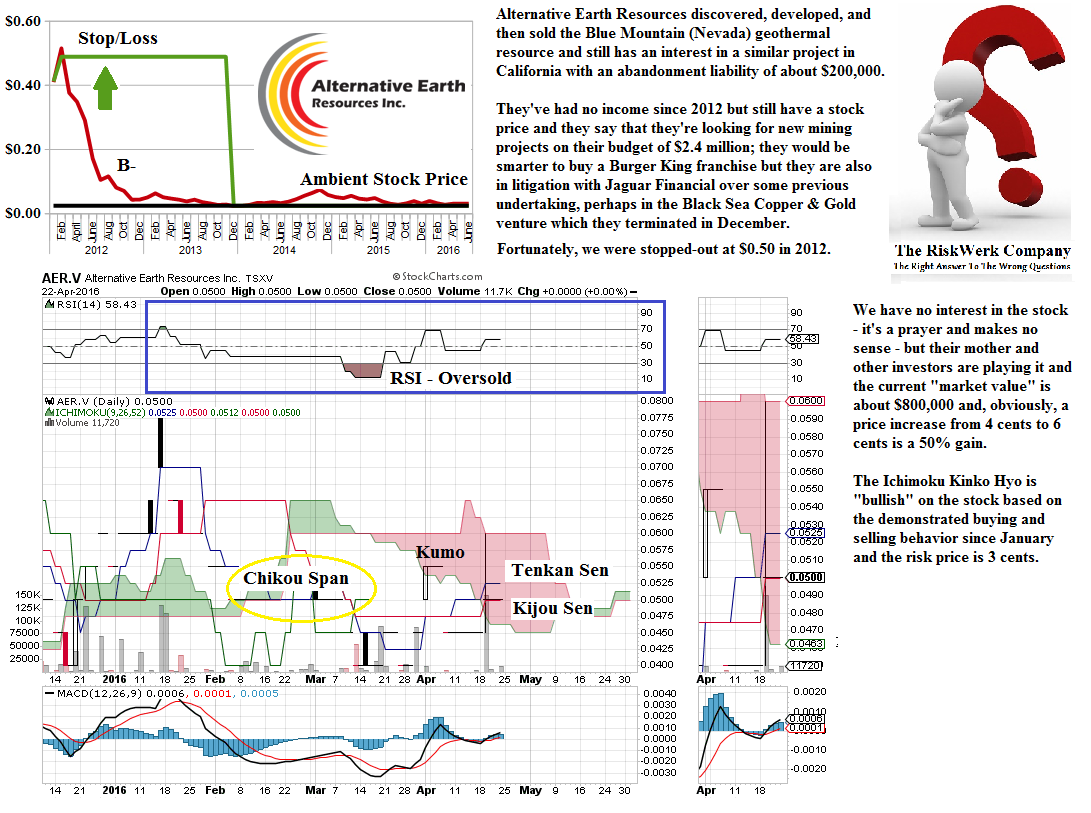

Figure 1.2 NGLPF (AER.V) Alternative Earth Resources Incorporated (B+) |

Figure 1.3 OPTT Ocean Power Technologies Incorporated (B+) |

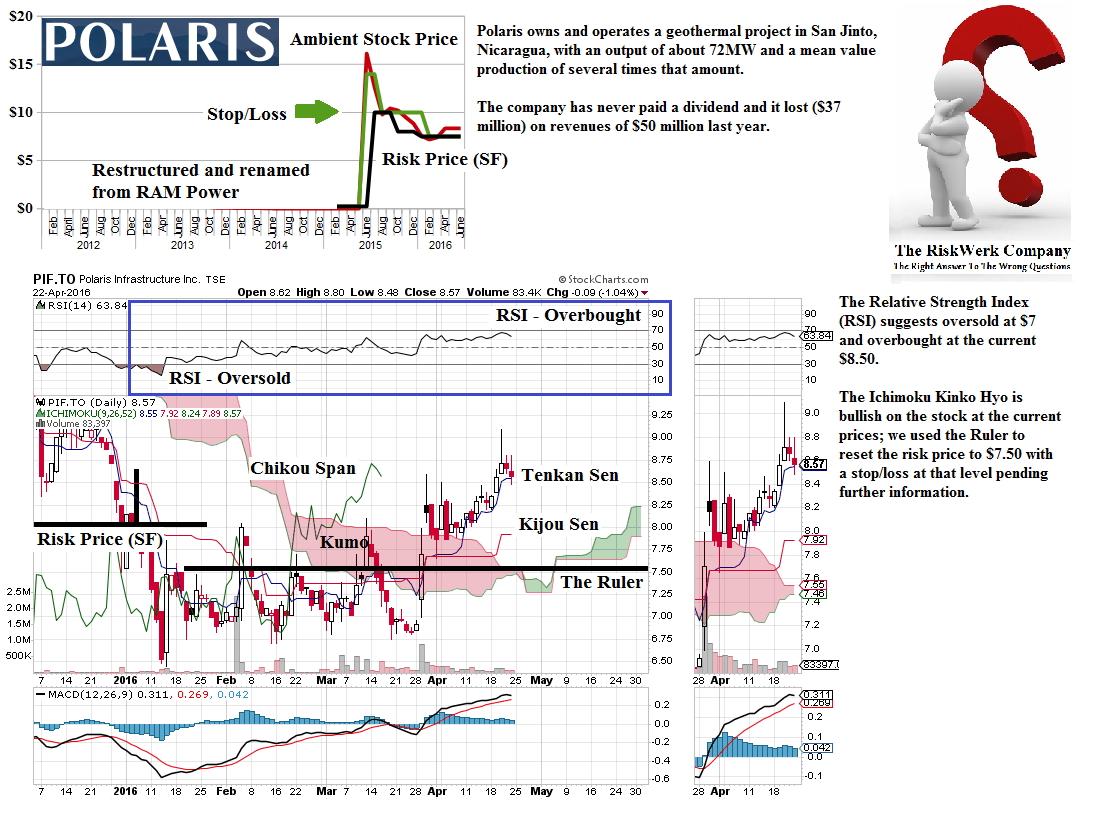

Figure 1.4 PIF.TO Polaris Infrastructure Incorporated (B+) |

Figure 1.5 RUN Sunrun Incorporated (B+) |

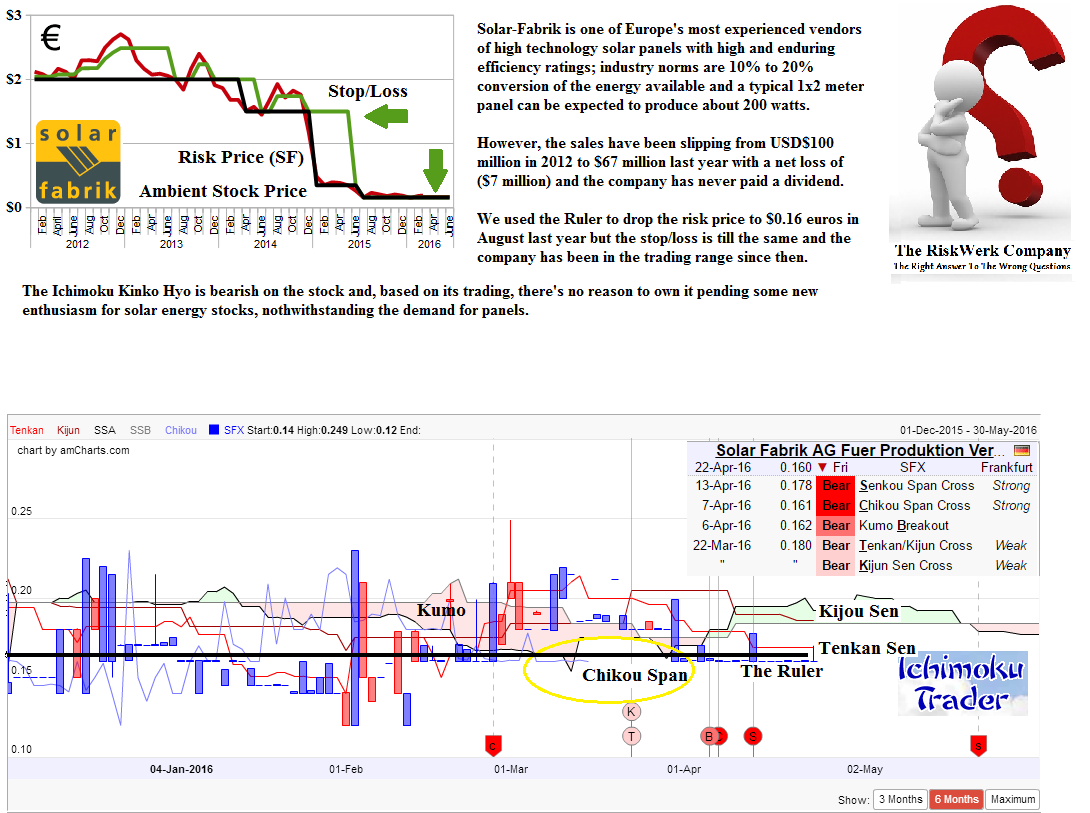

Figure 1.6 SFX.MU Solar Fabrik AG (B+) |

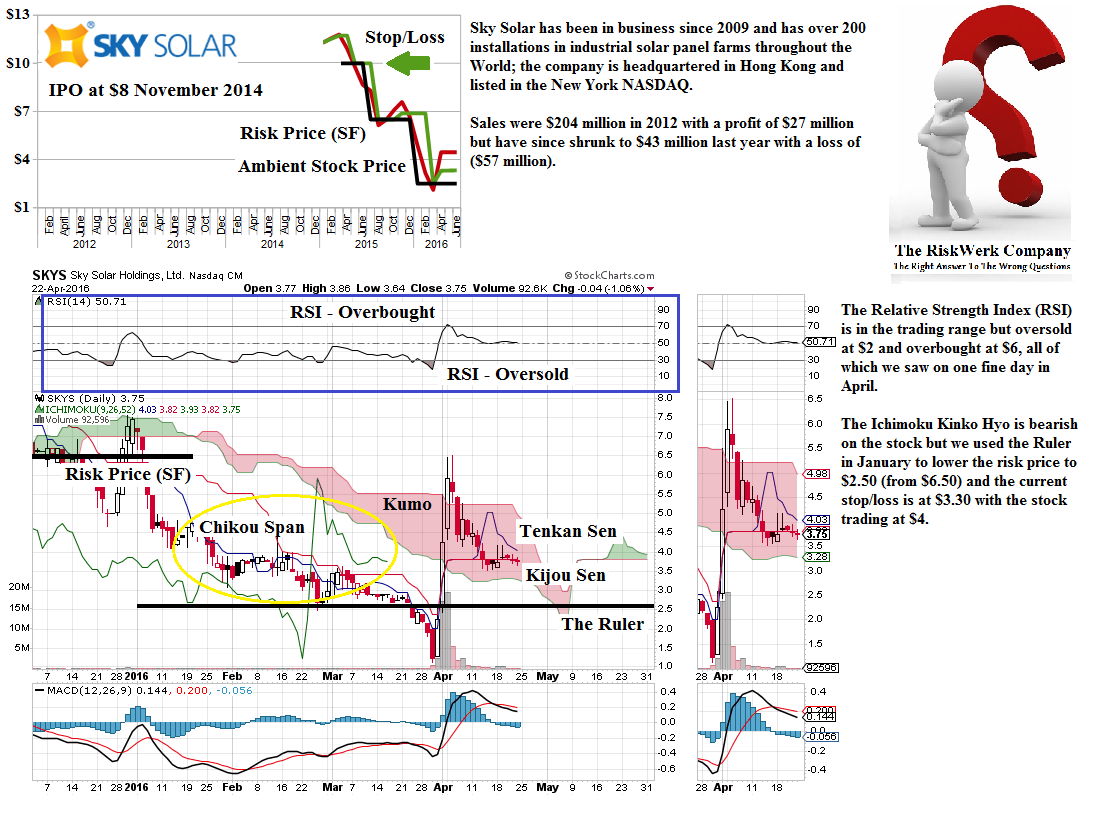

Figure 1.7 SKYS Sky Solar Holdings Limited ADR (B+) |

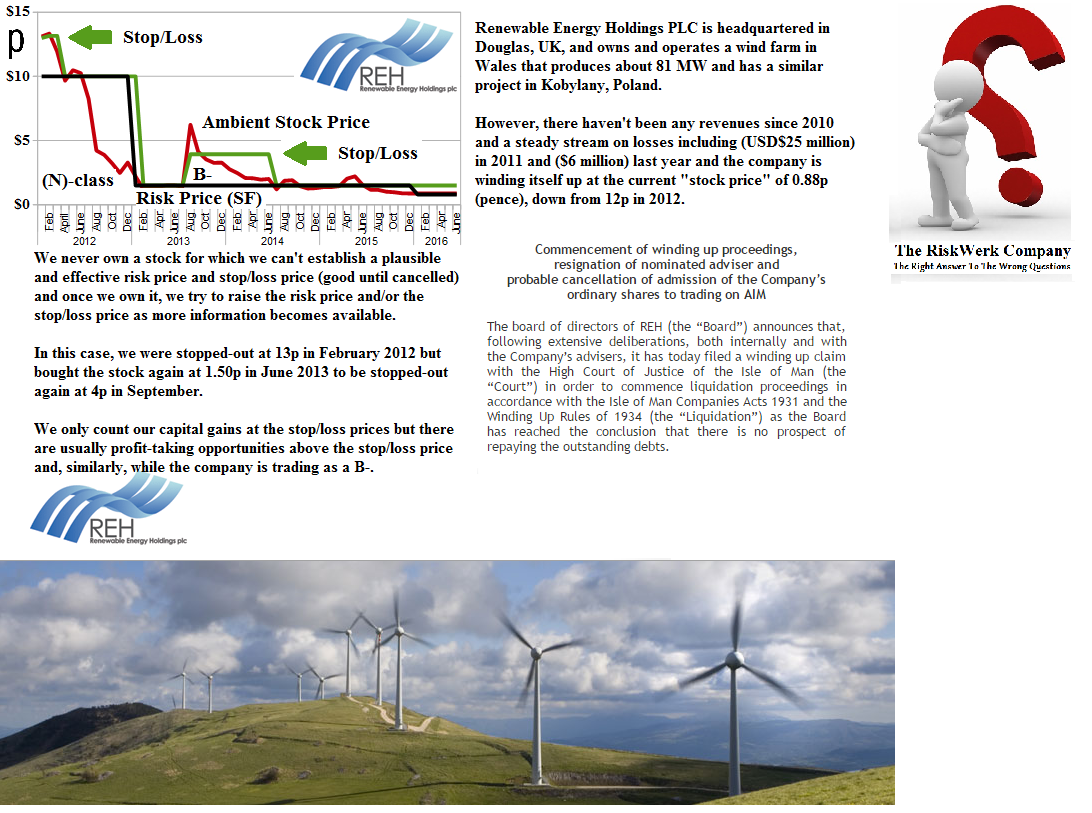

Figure 1.8 REH.L Renewable Energy Holdings PLC (B-) |

Figure 1.9 ASTI Ascent Solar Technologies Incorporated (N) |

Figure 1.10 DSTI DayStar Technologies Incorporated (N) |

Figure 1.11 Intelligent Energy Holdings PLC (N) |

Figure 1.12 SWVK.DE SolarWorld AG (N) |

Exhibit 2: More Power on Main Street – The (B)-class Portfolio

For more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.