(B)(N) Shopping In America

Deal Book. The US retail shopping place has become a strange place for shoppers and investors alike because of the high-profile and aggressive exits and entries of certain investors (Reuters, August 27, 2013, Ackman turns back on J.C. Penney, sells entire stake in retailer) and also because there is a lot of uncertainty regarding the future of traditional “bricks & mortar” retail that, at the store level, affects the employment of millions of administrative and sales staff, and the underlying manufacturers, their employees and suppliers, wholesalers, and transport industries, who, after all, are also their customers and can’t buy much if they’re unemployed.

Moreover, the “Made on Wall Street” brand continues to harass investors as they raise seemingly profound complaints about retail models, such as Herbalife, or the “business model” that somehow fails to maximize shareholder value, or attack the life-blood of these firms in support of their transient short positions (The Wall Street Journal, February 4, 2013, Creditors Allege Penney Violated Debt Terms).

Shopping In America

Our defence is to create a portfolio of stocks that contains them all and is, therefore, profoundly generic and a natural hedge.

That is, if we’re not shopping at one of them, then we’re likely to be shopping at another, and the news of the day can never catch us unaware because we’re already there (or not).

Shopping American in Mumbai

Along with the traditional “bricks & mortar” retailers, we’ve included their New World competition, Amazon (notwithstanding the retailers’ own online shopping sites) and Wal-Mart, and the “dollar stores“, with a view that if Americans are not shopping European & Prada or The Gatsby Collection (which we’ve excluded), electronics or appliances, drugs & cosmetics (Walgreens), groceries, automobiles, vacations, houses or cottages (or things to fix them at the Home Depot or Lowes), or for investments, or locally, they’re shopping here and need to come back at least once a month, possibly weekly, for entertainment and the household necessities that they use or wear every day, regardless of the stock markets.

“Shopping” American-style is a worldwide activity, and it never stops. It’s 24/7, every hour and every day of the week, but it might stop here (in America) if we can’t find more creative ways to invest in the retail stores that doesn’t involve pillaging them for their properties and pension plans.

There are sixteen companies in the portfolio “(B)(N) Shopping In America” which we’ve run as a Perpetual Bond™ which has returned +50% this year, plus dividends of another 1.6% on average, with no trouble at all.

There are sixteen companies in the portfolio “(B)(N) Shopping In America” which we’ve run as a Perpetual Bond™ which has returned +50% this year, plus dividends of another 1.6% on average, with no trouble at all.

Please see Exhibit 2 and 3 below.

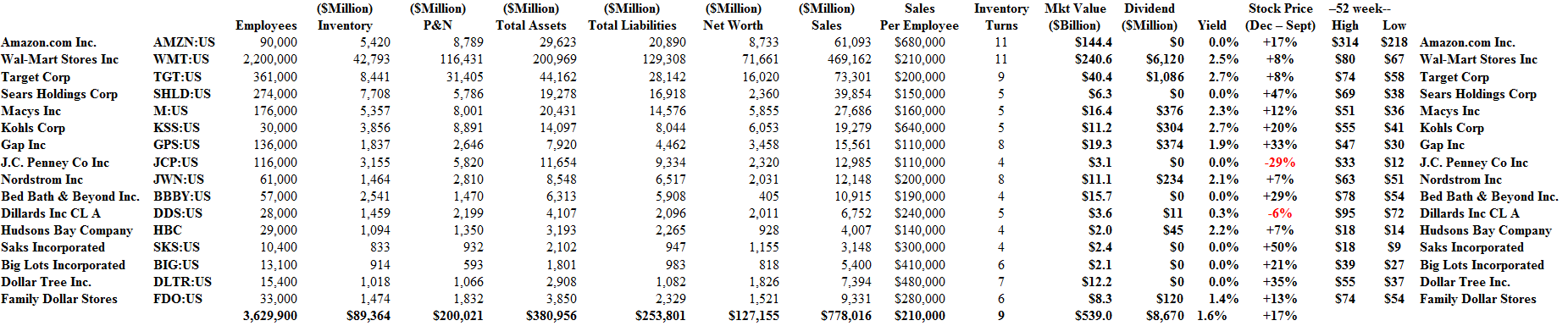

The reason that the portfolio is no trouble at all is not that we have any insight into the retail business from a consumer, operational or financial point of view. Based on the fundamentals (please see Exhibit 1 below), no combination of size, presentation, business model, debt leverage or gearing to equity, sales per employee, or inventory turn, or dividend policy, can be used to explain their stock prices.

Our rule is based on the price of risk. We only buy and hold a stock if the ambient stock price, summarized as the Stock Price (SP), appears to be at or above the price of risk, summarized as the Risk Price (SF), and for no other reason. Please see almost any of the (B)(N)-Company Posts for examples and also Exhibit 4 below on the Target Corporation.

From that point of view, retail investing, which includes all investors except the investment banks, broker/dealers and market-makers, is not different or harder than retail shopping and involves the same thought process and information that is peculiar to millions of shoppers.

Above (B) / Below (N)

Quite simply, stocks that are priced below their price of risk demonstrate an excess of supply over demand, and stocks that are priced above their price of risk demonstrate an excess of demand over supply.

That result is a theorem (Goetze 2006) provable in both mathematics and economics, that the price of risk resolves a Nash Equilibrium that obtains between “risk seeking” investors and “risk averse” investors and results in portfolios of stocks, labelled (B), that tend not to lose in value, and portfolios of stocks, (N), that tend not to gain in value.

And that distinction can be observed in practice because “an investment” is “the purchase of risk” – we want to keep our money safe and obtain a hopeful, but not necessarily guaranteed, return above the rate of inflation – and carries the same burden of our thought process, information, abilities, budget, and sense of risk aversion, that we might bring to anything else that we want to buy or need if there are many choices available to us.

For example, a stock certificate is only actionable as a contract and doesn’t entitle us to the company’s property, earnings, or even the payment of dividends, and it’s only worth more to us if someone is willing to buy it from us at a higher price than we paid for it (notwithstanding that if we own or control enough of the stock, we might own the company or be able to influence its management).

Exhibit 1: Retail Fundamentals

Retail Fundamentals

(Please Click on the Chart to make it larger and again if required.)

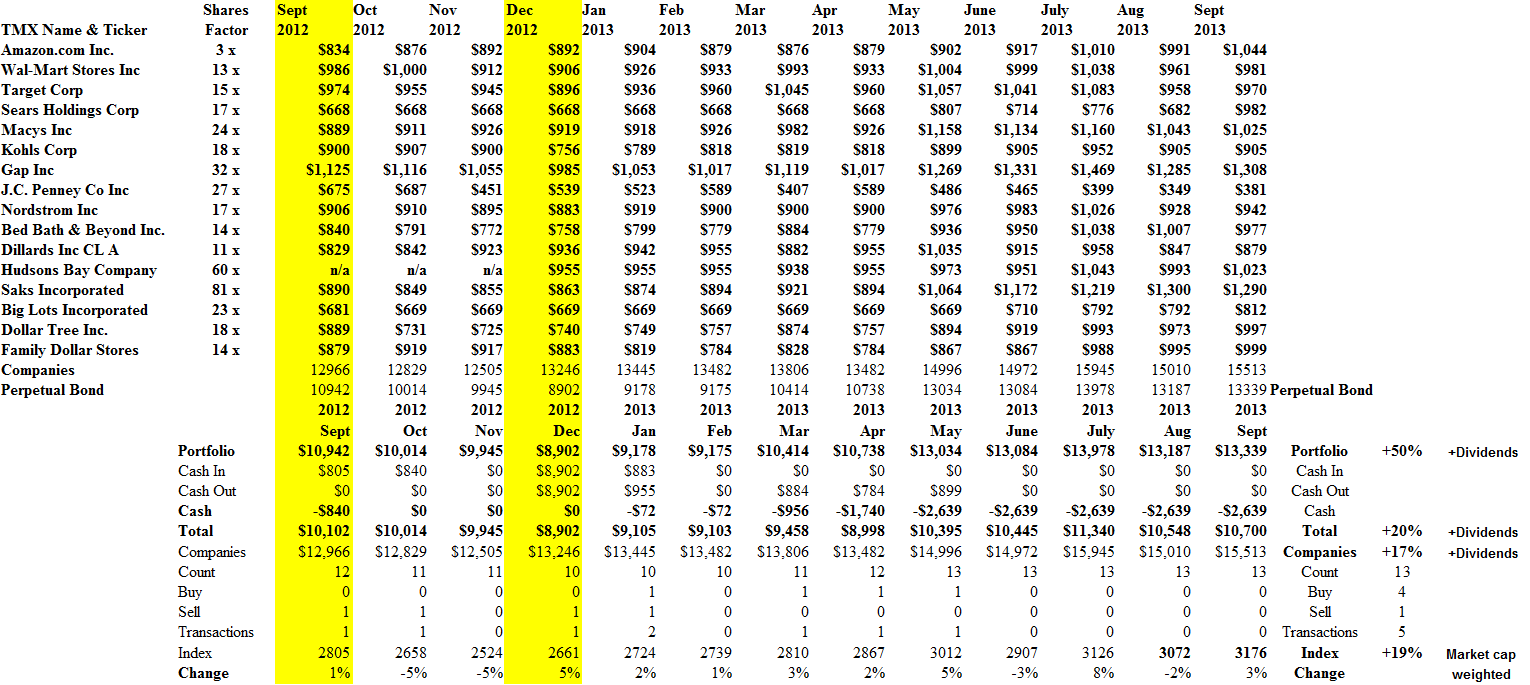

Exhibit 2: (B)(N) Retail – Prices & Portfolio – September 2013

(B)(N) Retail – Portfolio Prices – September 2013

(Please Click on the Chart to make it larger and again if required.)

Exhibit 2 above shows the ambient stock prices of the companies in the portfolio domain since September last year and the (B)(N) status of each of the companies at those prices, and prices near to them, allowing for the demonstrated volatility of stock prices.

In general, we are indifferent to the purchase prices but use stop/loss selling and sometimes a bought put to protect the prices and gains that we have.

Because the number of companies is small (only sixteen) and there are large differences in their prices, we spent more or less the same amount of money on each stock (in December and early January) by varying the number of shares purchased using the “Shares Factor” which is calculated from their average stock prices in the nine months preceding September 2012.

Please see Exhibit 3 below and for additional information on the chart elements and selling discipline, our recent Posts on Earnings Don’t Matter (the Dow companies) and Earnings Don’t Matter – NASDAQ 100.

We also note that how much money we invest depends only on our budget and the example scales from 000’s to millions without a problem since the entire market capitalization of these companies is currently about $540 billion, and if they are a (B), we are holding or buying them now with the same intensity as we did last December, and for the same reasons even though the average stock price of these companies is up +17% since December.

Exhibit 3: (B)(N) Retail – Portfolio & Cash Flow – September 2013

(B)(N) Retail – Portfolio & Cash Flow – September 2013

(Please Click on the Chart to make it larger and again if required.)

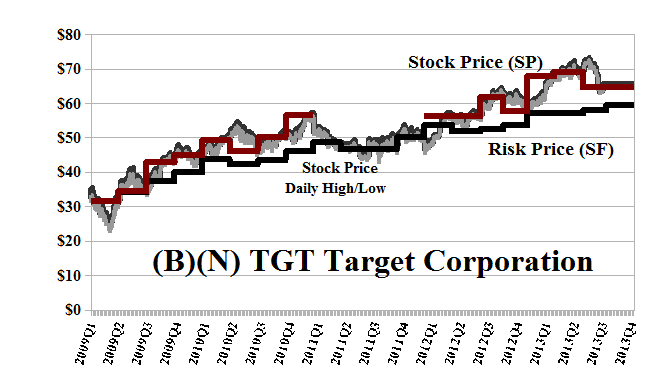

As an example, Target Corporation became eligible for inclusion in the Perpetual Bond™ at $56 in 2011 and is still in the Perpetual Bond™ at its current price of $64 which is above the Risk Price (SF) of $58 (Red line Stock Price (SP) above the Black line Risk Price (SF) in Exhibit 4 below).

Drops in the ambient stock price are saved by stop/loss selling or a bought put against our long position. If the stock is sold, then we’re prepared to buy it back at a lower price if the stock price still appears to be trading above the price of risk, or if we have the put and are still determined to keep the stock, we can sell the in-the-money put and re-visit our price protection, with the possibility that if we hold the stock, then we can also sell an opportunistic call against it.

Our estimate of the current downside in the stock price due to the demonstrated volatility is minus ($4) per share so that we would not be surprised by any price between the current $64 and $60 (which is still above the price of risk) and $68.

Since the market is full of “surprises”, the selling discipline is important and necessary to protect the stock prices that we have. For example, the November put at $63 costs $0.90 per share today, and, if we choose, we can partially offset the cost of that by selling the November call at $68 for $0.50 per share so that for a net cost of holding the stock at the current $64 and the cost of the collar, $0.40 per share ($0.90 less $0.50), we are assured to no less than $63 and no more than $68 for the next two months, and can roll the collar forward and up (or rely on the stop/loss at a higher price) as more information becomes available.

The company expects to pay dividends of $1.1 billion to its shareholders this year for a current yield of 2.7% and the stock price is up +8% since December.

Exhibit 4: (B)(N) TGT Target Corporation – Risk Price Chart

(B)(N) TGT Target Corporation – September 2013

Target Corporation was incorporated in Minnesota in 1902. It operates as three segments: U.S. Retail, U.S. Credit Card and Canadian.

(Please Click on the Chart to make it larger if required.)

From the Company: Target Corporation operates general merchandise stores in the United States. The company offers household essentials, including pharmacy, beauty, personal care, baby care, cleaning, and paper products; hardlines comprising music, movies, books, computer software, sporting goods, and toys, as well as electronics that consist of video game hardware and software; apparel and accessories, such as apparel for women, men, boys, girls, toddlers, infants, and newborns, as well as intimate apparel, jewelry, accessories, and shoes. It also provides food and pet supplies, including dry grocery, dairy, frozen food, beverages, candy, snacks, deli, bakery, meat, produce, and pet supplies; and home furnishings and décor, such as furniture, lighting, kitchenware, small appliances, home décor, bed and bath, home improvement, automotive, and seasonal merchandise comprising patio furniture and holiday décor. In addition, it offers in-store amenities. As of September 6, 2013, it had 1,856 stores, including 1,788 stores in the United States and 68 stores in Canada. The company distributes its merchandise through a network of distribution centers, as well as third parties and direct shipping from vendors. Further, it provides general merchandise through its Website, Target.com; and branded proprietary Target Debit Card. Target Corporation was founded in 1902, has 360,000 employees, and is headquartered in Minneapolis, Minnesota.

For more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.