(B)(N) Bloomin’ Brands & Red Robin

Deal Book. The Street likes growth and good food for growth – in every which way – has been hot, hot, very hot, this year in the restaurant stocks and groceries as Americans seek the sybaritic and step out (The Street, June 17, 2013, Cramer’s Mad Money Recap).

Courtesy: Red Robin Gourmet Burgers Incorporated

We like growth, too, but we know what happens when the “growth” stops. In cancer, it’s called a cure, but in stock prices, it’s called momentum and when the momentum stops, a lot of investors will need to empty their pockets and won’t eat there again, no matter how good the food.

So, if we’re going to ride the growth curve – and we will, even as “risk averse” investors – then we (speaking for ourselves) need to know what we’re eating and where we are, and when it comes to companies, and their stock prices and our money, the only compass is the price of risk, which, like Pepto-Bismol®, is the momentum and volatility killer. Cheque! Please!

Courtesy: Bloomin’ Brands Incorporated

Bloomin’ Brands has a market value of $3 billion, 93,000 employees, total assets of $3 billion, and a lot of debt, also about $3 billion ($2.7 billion); in other words, there isn’t anything on the balance sheet for the shareholders equity ($300 million) and the company has never paid us a dividend, either.

The company re-blossomed in an IPO in August 2012 that only sold about 14 million shares at $11 to raise $150 million, new money which stuck around and didn’t disappear into the maws of the owners, Catterton Partners and Bain Capital, who bought the original assets for $3.2 billion in 2006 and seem to have been working the “debt market” with which the company is now saddled, and there’s a lot that’s riding on sales, gross profits, and earnings, and Catterton Partners and Bain Capital still own more than 50% of the shares.

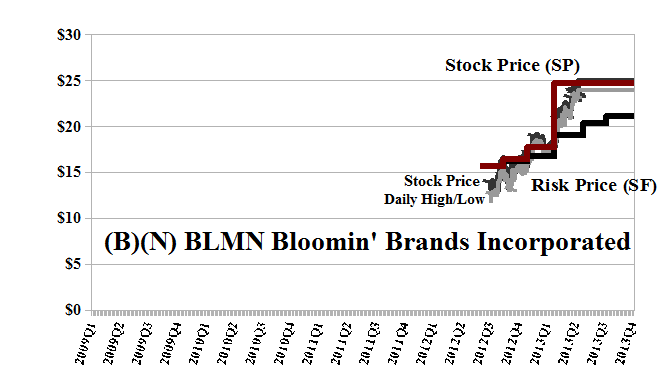

It became eligible for the Perpetual Bond™ at $16 almost right away and we’ve kept it through the current $25 (please see Exhibit 1; Red Line Stock Price (SP) above the Black Line Risk Price (SF) and for no other reason).

The downside in the stock price due to ambient volatility is minus ($2.50) and even though there is an options market, we can afford to just keep it at the stop/loss of $22, and rising with the stock price, if it does; or if we’re sold out at $22 or more, we might buy it back at lower prices if it is still trading above the Risk Price (SF).

Exhibit 1: (B)(N) BLMN Bloomin’ Brands Incorporated – Risk Price Chart

B)(N) BLMN Bloomin’ Brands Incorporated

Bloomin’ Brands Incorporated is a casual dining restaurant company with a portfolio of differentiated restaurant concepts.

(Please Click on the Chart to make it larger if required.)

From the Company: Bloomin’ Brands Incorporated owns and operates casual, upscale casual, and fine dining restaurants primarily in the United States. The company operates restaurants under various concepts, including Outback Steakhouse, a casual dining steakhouse; Carrabbas Italian Grill, an Italian casual dining restaurant; Bonefish Grill, a casual seafood restaurant; Flemings Prime Steakhouse and Wine Bar, an upscale, contemporary prime steakhouse; and Roys, an upscale dining restaurant. As of December 11, 2012, it owned and operated approximately 1,400 restaurants in 48 states and 20 countries and territories. The company, formerly known as Kangaroo Holdings Incorporated was incorporated in 2006, has 93,000 employees, and is based in Tampa, Florida.

Red Robin Gourmet Burgers is much smaller than Bloomin’ Brands and has a market value of about $800 million at the current $56 per share; it has also never paid a dividend, but has sales of about $1 billion a year and has shown a profit every year of between $10 million and $30 million since 2009.

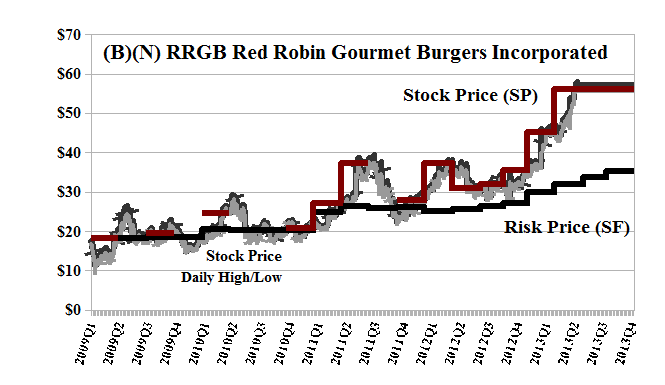

It’s trading at $56 which is substantially above the current Risk Price (SF) of $35 and rising (please see Exhibit 2 below) and it became eligible for the Perpetual Bond™ at much lower prices of $25 to $35 more than a year ago and we’re prepared to hold it now with only the stop/loss in force which is $56 less our estimate of the downside in the stock price due to ambient volatility of minus ($7.50) per share.

We can scratch our heads and wonder, Why is Bloomin’ Brands priced at $25 and up more than +50% since last year; or, Why is Red Robin priced at $56 and up more than +50% since last year?

We can scratch our heads and wonder, Why is Bloomin’ Brands priced at $25 and up more than +50% since last year; or, Why is Red Robin priced at $56 and up more than +50% since last year?

There is no sensible answer for that except that there are enough investors who are willing to buy the stocks at those prices and others who are not yet willing to sell them for less. And as long as that is true, the stock price will continue to rise.

For more information, please see our Posts, Stock Prices Are The New Pink and Bystanders & Collateral Damage.

Exhibit 2: (B)(N) RRGB Red Robin Gourmet Burgers Incorporated – Risk Price Chart

(B)(N) RRGB Red Robin Gourmet Burgers Incorporated

Red Robin Gourmet Burgers Incorporated, together with its subsidiaries, is a casual dining restaurant chain focused on serving an imaginative selection of high quality gourmet burgers in a family-friendly atmosphere.

(Please Click on the Chart to make it larger if required.)

From the Company: Red Robin Gourmet Burgers Incorporated, together with its subsidiaries, develops, operates, and franchises casual-dining restaurants across the United States and Canada. Its restaurants offer gourmet burgers, as well as various salads, soups, appetizers, entrees, desserts, and signature Mad Mixology alcoholic and non-alcoholic specialty beverages. As of the June 11, 2013, the company operated 474 Red Robin locations, including 336 company-owned Red Robin restaurants, 5 Red Robin’s Burger Works locations, and 133 franchised Red Robin restaurants. Red Robin Gourmet Burgers, Incorporated was founded in 1969, has 22,000 employees, and is headquartered in Greenwood Village, Colorado.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2006) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.