Momentum (Econo-speak)

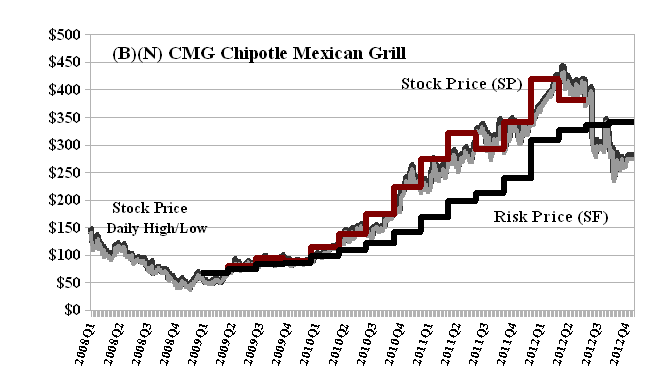

The economist, Buttonwood (nom de plume), is wondering why the obvious phenomenon of “momentum” – the tendency of fast rising stocks to keep going up – is not “arbitraged” away (Buttonwood, The Economist, December 12, 2012, Market failure). The market abounds with exciting examples but we have selected the rather tasty and wholesome CMG Chipotle Mexican Grill which also shows the equally intriguing reverse phenomenon that might be called a “hard stop or panic on the brakes” and one has to wonder how quickly “exuberance” and “enchantment” becomes “despair” and that is also fair game for “arbitrage” if we are prepared for it.

Exhibit 1: (B)(N) CMG Chipotle Mexican Grill – Risk Price

Chipotle Mexican Grill Incorporated (Denver, Colorado) develops and operates fast-casual, fresh Mexican food restaurants throughout the United States and two restaurants in Toronto, Canada, two in London, England and one ShopHouse Southeast Asian Kitchen.

(Please Click on the Chart to make it larger if required.)

Buttonwood, citing very recent research, attributes the phenomena (both up and down) to an “expanding disequilibrium” that is fired by investor greed (gambling) and fuelled by easy credit and then further promoted (or fanned) by herding among portfolio managers who are rewarded for performing (buying and selling) and are substantially immunized against the results of their performance (they did the best that they or anyone could have done, didn’t they).

In contrast, we would say that the phenomena (both up and down) is the result of sensible investor risk aversion (not gambling) and demonstrates a Nash Equilibrium already fully expressed. Moreover, these effects are observable, measurable and actionable.

That’s quite a difference. In the Buttonwood view, we are always spinning out of control, both up and down. Whereas in our view, we are always in control and responding appropriately to the demonstration of investor risk aversion. Please our Post, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012.

More Food For Thought

Buttonwood (and their agents) is defeated by a reliance on the “differential” view of “economic activity” which may be described (from the point of view of mathematics) as a solution (or “toy solution”) in search of a problem absent a foundation in economics or a domain that describes, at a minimum, the properties of economic activity for which a differential solution might apply. Please see, for example, our Posts, Stock Prices Are The New Pink, June 2012, and The Price of Money, November 2012. Other economists have had similar concerns:

“Nearly two decades of drawing downward-sloping liquidity preference curves in textbooks and on classroom blackboards should not blind us to the basic implausibility of the behavior they describe.” – James Tobin, Liquidity Preference as Behaviour Towards Risk, Review of Economic Studies, 1958.

“In a world involving no transaction friction and no uncertainty, there would be no reason for a spread between the yield on any two assets, and hence there would be no difference in the yield on money and on securities. In such a world securities themselves would circulate as money and be acceptable in transactions.” – Paul A, Samuelson, Foundations of Economic Analysis, Cambridge, Harvard University Press, 1947.

“In order to carry out a market transaction it is necessary to discover who it is that one wishes to deal with, to inform people that one wishes to deal and on what terms, to conduct negotiations leading to a bargain, to draw up the contract, to undertake the inspection needed to make sure that the terms of the contract are being observed, and so on. These operations are often extremely costly, sufficiently costly at any rate to prevent many transactions that would be carried out in a world in which the pricing system worked without cost.” – Ronald H. Coase, The Problem of Social Cost, Journal of Law and Economics, 1960.

“A world without transaction costs has very peculiar properties … the world of zero transaction costs turns out to be as strange as the physical world without friction. Monopolies would be compensated to act like competitors and insurance companies would not exist.” – Ronald H. Coase, The Firm, The Market, and The Law, U of Chicago, 1990.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

Share this: