(B)(N) TSLA Tesla Motors Incorporated

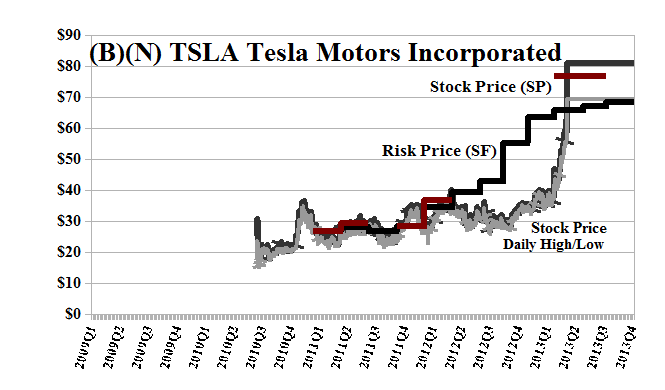

Drama. Jim (Cramer) doesn’t know how to “value” this company, Tesla Motors Incorporated (The Street, May 9, 2013, Three Short Ideas Just Aren’t Playing Out). What is the stock price, anyway? Is it $30 to $35 which it has been for a year, or is it $80, which it was yesterday on volumes of 25 million shares, on both Thursday and Friday, although typical daily volumes are still in the range of one million shares for a company that has never paid a dividend and has just 115 million shares outstanding (please see Exhibit 1 below).

And it gets worse because all bets are on the inventory which is currently $238 million of electric cars ready for sale or in production; and the plant & equipment to produce them, which is valued at $600 million, so that the combined total of $838 million is about five times the net worth, and less than the total liabilities of the company which produces a car that retails for between $60,000 and $85,000 and tanks up (or juices up) beside the Toyota Prius Plug-In at $30,000 and cash back with a 0% APR financing plan.

But even more shocking is that a lot of people who have never heard of Tesla Motors, own this stock in their mutual funds and retirement plans, and don’t even know it; and a lot of people, or just a lot of money, must have bought it yesterday at $70 to $80 because 25 million shares changed hands, or the price would have vanished and never lifted off from $35 in March.

At the end of March, global investment companies such as Capital Research Global Investors, Morgan Stanley, The Vanguard Group, Allianz Asset Management AG, Artisan Partners Limited Partnership, Marsico Capital Management LLC , Wells Fargo & Company, Baillie Gifford & Company, Invesco Limited, and FMR LLC, owned anywhere from 2 million to 6 million shares valued at between $70 million and $215 million on their books, for a total of $1.7 billion and 50 million shares.

And mutual funds such as the Fidelity OTC Portfolio, Fidelity Blue Chip Growth Fund, Fidelity Contrafund Incorporated, Fidelity Growth Company Fund, Fidelity Mid-Cap Stock Fund, Growth Fund of America Incorporated, Smallcap World Fund, College Retirement Equities Fund, Artisan Mid-Cap Fund, and the Invesco Mid-Cap Growth Fund, each owned between 1 million and 5.4 million shares valued at between $40 million and $200 million, for a total of $900 million and 25 million shares.

That totals to $2.6 billion of investment in a company that was valued at no more than $3 billion, in total, in March, and is “valued” at $8.8 billion today. The aforementioned companies have 75 million shares between them, of 115 million outstanding, and they can’t sell them at any price unless they can find some new buyers (The Wall Street Journal, April 22, 2013, U.S. Seizes $21 Million From Electric Car Maker Fisker).

On the other hand, if people like the company that much, then Tesla has yet another golden opportunity and should think about selling some of their shelf stock out of treasury – why not 50 million shares to feed this market (if, in fact, there is one); “short sellers” or people who just don’t like the car, and borrowed the stock to sell it short at $35 or $30, of course, won’t be buying the car even if they can get some of their money back before they have to replace the stock at $65 or more. That’s the price of not knowing the price of risk (please below).

It’s become eligible for the Perpetual Bond™ at $80 over the Risk Price (SF) of $69 and rising to $70 (please see Exhibit 1 below). We don’t care what it’s “worth” as long as somebody thinks that it’s “worth” more than what we paid for it and we can sell it a higher price. However, our estimate of the downside due to price volatility is minus ($15) so that we would not be surprised by any price between the current $80 and $65 or $95. Since we can’t buy any useful price protection, we’re not buying it at all, and we’re going to leave all that money on the table for those in the know. We’ll probably get it later.

Exhibit 1: (B)(N) TSLA Tesla Motors Incorporated – Risk Price Chart

(B)(N) TSLA Tesla Motors Incorporated

Tesla Motor Incorporated designs, develops, manufactures and sells high-performance fully electric vehicles and advanced electric vehicle power train components.

(Please Click on the Chart to make it larger if required.)

From the Company: Tesla Motors Incorporated designs, develops, manufactures, and sells electric vehicles and electric vehicle power train components. The company also provides services for the development of electric power train systems and components, and sells electric power train components to other automotive manufacturers. It markets and sells its vehicles through Tesla stores, as well as over the Internet. As of March 31, 2013, the company operated a network of 32 stores in North America, Europe, and Asia. Tesla Motors Incorporated was founded in 2003 and is headquartered in Palo Alto, California. Tesla Motors is growing and now has about 3,000 employees in contrast to the Toyota Motor Corporation which has already grown-up and has at least 300,000 employees, world-wide.

Which is another concern that we have; the market values the Toyota Motor Corporation at $200 billion and so, each employee at less than $700,000 ($200 billion/300,000 = $667,000) in contrast to each employee of the Tesla Motor Corporation at more than four times as much ($8.8 billion/3000 = $3 million), and suggests $20 per share, rather than $80, when the buzz wears off, or less should the car fizzle like a Fisker.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.