(B)(N) MG Magna International Incorporated

Drama. The S&P TSX Composite Index closed at 12,500 last week, which is the same level as January of this year, and January of last year, and it’s up from 12,300 on May 10, 2006, seven years ago, in contrast to the Dow Jones Industrial Companies and the S&P 500 which are both up +50% in those seven years, and the increase in those markets is worth about five times the entire Canadian market of about $2 trillion.

A well-regarded Canadian investment adviser attributes last week’s tiny (but apparently surprising) increase to a renewal of investor “risk appetite” feeding on the recent U.S. experience (Reuters, May 10, 2013, Magna and Bombardier drive TSX higher); and a Canadian bank economist predicts that the Canadian dollar will lose about 10% of its value in comparison to the U.S. dollar, this year (The Canadian Press, May 9, 2013, TD Bank forecasts loonie could sink to 90 cents US by 2014).

We don’t know the future and our investments don’t depend on forecasting the future, but we can put this together and we might think that since 70% of Canadian exports are to U.S. and (could be) becoming cheaper to buy, and that most large capitalization Canadian stocks are also listed in New York, that the Canadian market is cheap now and going to become more expensive in Canadian dollars in the upcoming months, and that Canadian bond investments at low yields are about to tank, all of which will be good news for the stock market and the stock market index which will rise as least as much as the dollar falls, and be boosted even further by a hopeful rise in Canadian exports of goods and services.

Magna International Incorporated trades as MG.TO in Toronto and MGA in New York; MGA closed at US$64.71 on Friday and MG.TO closed at CDN$65.46 merely reflecting a currency exchange difference that will always be arbitraged away because we cannot expect to buy the stock “cheaply” in Toronto and sell it at a higher real price in New York, or vice versa.

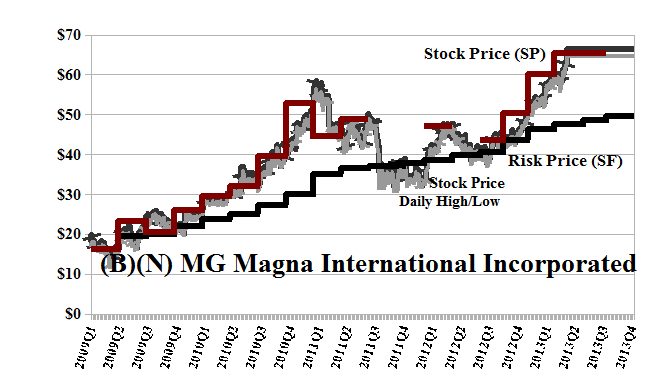

The current Risk Price (SF) is $50 and Magna became eligible for the Perpetual Bond™ at much lower prices of $45 to $50 last year (please see Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason).

However, our estimate of the downside risk due to the demonstrated price volatility is minus ($9) so that it could be trading between $56 and $74 and off the current price of $65 without surprise. The quarterly dividend is $0.32 per share for a total payout of $298 million this year and a current yield of 2%.

If the Canadian dollar loses its value against the U.S. dollar then the stock price will increase for that reason alone, quite apart from the boost to the company’s export business to the U.S., Europe, and China. The August put at $64 is available for $2.20 today and we can sell the call at $68 against our long position for $1.50, so that we can hold the stock between $64 and $68 for the next three months for the cost of the “collar” at $0.70 ($2.20 less $1.50) which we might revise if the Canadian dollar unfolds, so to speak.

Exhibit 1: (B)(N) MG Magna International Incorporated – Risk Price Chart

(B)(N) MG Magna International Incorporated

Magna International Incorporated designs, develops, and manufactures advanced automotive systems, assembles modules & components, and engineers & assembles complete vehicles for sale to original equipment manufacturers of cars & light trucks.

(Please Click on the Chart to make it larger if required.)

From the Company: Magna International Incorporated designs, develops, manufactures, and engineers automotive systems and components to original equipment manufacturers primarily in North America, Europe, and internationally. Its products include automotive interior systems, including sidewall and trim, cargo management, cockpit, and overhead systems; seating systems, such as complete seating systems, seat structures and mechanisms, and foam and trip products; and closure systems comprising door modules, power closure systems, window systems, latching systems, driver controls, electronic features, lighting systems, sealing systems, engineered glass, and handle assemblies. The company also offers body and chassis systems, which include body and chassis systems, engineering and tooling, and renewable energy structures; vision systems that comprise interior and exterior mirrors, actuators, and electronic vision systems; and electronic systems, such as driver assistance and safety systems, engine electronics and sensors, body systems and human-machine interfaces, intelligent power systems, hybrid and electric vehicle components/systems, and industrial products. In addition, it provides exterior systems, including front and rear fascia systems, class A composite panels, structural components, sealing systems, modular systems, under hood and underbody components, exterior trims, and sheet molding compound materials. Further the company offers powertrain systems, such as driveline and fluid pressure systems, and metal-forming solutions; and engineering services and system integration. Additionally, it provides roof systems comprising retractable hard and soft tops, and sliding folding and modular roofs, as well as vehicle engineering and assembly, and contract manufacturing services. Magna International Incorporated was founded in 1957 and now has 120,000 employees, and is headquartered in Aurora, Ontario, Canada.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.