(B)(N) THI Tim Hortons Incorporated

Deal Book. They’re rolling up to the rim at Timmy’s but it’s the takeout window that they want and not so much the coffee and doughnuts (CBC, June 18, 2013, Tim Hortons being circled by Wall Street hedge funds and Reuters, June 18, 2013, Tim Hortons shares climb as second investor pushes for change).

Courtesy: Tim Hortons Incorporated

Scout Capital Management LLC is a hedge-fund and filed an SEC Schedule 13D on June 6, 2013, declaring 8.4 million shares or 5.5% of the common shares outstanding, and they follow Highfields Capital Management LP which now holds about 6 million shares and a 4% interest.

Drive Thru

Courtesy: Tim Hortons

Undoubtedly, the management and board of Tim Hortons have already discussed ideas such as buying back some of its own shares, or scaling back on the U.S. expansion plans, or possibly spinning off its real estate assets into a trust such as a REIT which other firms such as Loblaw Companies Limited and the Canadian Tire Corporation are actively engaged with at the present time, and why not Shoppers Drug Mart, McDonalds, Sears Canada, Target, the banks and all of their properties, and so on.

Of course, Tim Hortons would have to own or control the REIT in order to avoid yet another activist shareholder suggesting that the REIT should sell the properties in a “hot” market, or charge themselves more rent, or do less maintenance and take down the signage in order to increase “shareholder value” by filling the doughnut holes.

Courtesy: Post Holdings

We’re not impressed at all and if creative solutions are required, as they say, where will they get the time to advise both Tim Hortons and Post Holdings (another of their alleged basket cases) when their own website is in such dire need of creative maintenance?

Obviously, they are “cereal” activists, so to speak, who exploit smaller capitalized companies for personal gain – if less than $10 billion, then just $500 million buys 5% and who doesn’t have $500 million these days? In our view, “greenmail” and noisy shareholder activism is just an updated variant on pump & dump.

But there are other problems, too, and they go to issues of responsible corporate governance and the representation of all the shareholders and stakeholders in the face of noisy activism akin to politicking and vote buying with a questionable display of leadership that amounts to shouting with a proxy and a power-point.

For example, from a technical point of view, trivial measures such as the price to earnings multiple [P/E] and the earnings per share [EPS] are irrelevant to gauging the standard of the stock price performance, or the “shareholder value”, or the efficiency of the firm, and we challenge the business whiz-kids to prove otherwise. Do that and get back to us.

And if they can’t do that, or fix their website, what are they supposed to know about “capital structure, capital expenditures, timing and magnitude of share repurchases, management compensation metrics, and technology” (ibid, CBC) that we should pay for on our time? And they left out ramping up the debt and raiding the employee pension plan. Humph.

And if they really want to improve the efficiency of the business and operating profits, they could take up a clip board, serve coffee, make sandwiches, sweep the floors, greet the customers, and so forth, and work there alongside the 2,500 other employees who probably have a lot of good ideas based on experience.

And where has the Board been all these years, on our payroll, and not noticed these things discovered by the newbies and born-again coffee magnats?

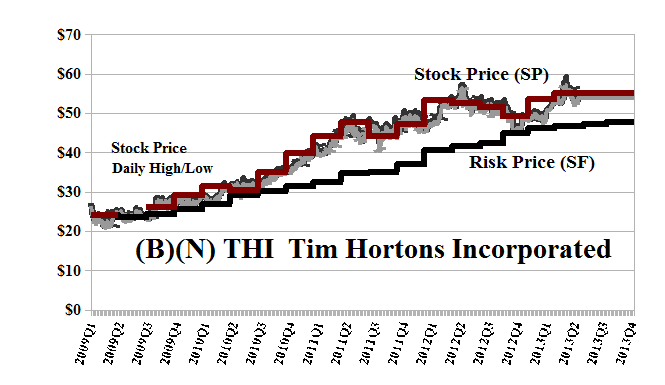

Moreover, we own the stock because we “like” it and we’re not alone because the stock has been trading at or above the price of risk since at least $25 in 2009 and it’s now trading at $50 to $60 on its own efforts and with a dividend yield of 2% on coffee that’s better than at home. Please see Exhibit 1 below and our previous Post.

And what if we and other large shareholders such as FMR LLC which owns almost 9% of the stock, or the Royal Bank of Canada and the TD Asset Management Incorporated which own more than 10% of the stock between them, decide to take our money, interim profits, and go home, how that will affect the stock price?

Exhibit 1: (B)(N) THI Tim Hortons Incorporated – Risk Price Chart

(B)(N) THI Tim Hortons Incorporated – June 18 2013

Tim Hortons Incorporated, of Oakville, Ontario, develops and franchises quick-service restaurants that serve food, including coffee, other hot and cold beverages, baked goods, sandwiches, soups and other foods products to legions of students, senior citizens and retired folks, travelers, baby-sitters, and workers on their way or on their break.

(Please Click on the Chart to make it larger if required.)

From the Company: Tim Hortons Incorporated engages in the development and franchising of quick service restaurants primarily in Canada and the United States. Its restaurants provide premium coffee, espresso-based hot and cold specialty drinks, cappuccinos and espresso shots, fruit smoothies, home-style soups, fresh baked goods, grilled Panini and classic sandwiches, wraps, soups, prepared foods, and other food products. As of December 30, 2012, the company had 4,264 restaurants, including 3,436 in Canada, 804 in the United States, and 24 in the Gulf Cooperation Council. Tim Hortons Incorporated was founded in 1964, has 2,500 employees, and is based in Oakville, Canada.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2006) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.