(B)(N) AMAT Applied Materials Incorporated

Deal Book. Applied Materials of Santa Clara, California, is planning to merge with its smaller rival Tokyo Electron Limited in an all stock deal that will create a new industrial giant in the international business of designing and manufacturing the equipment used to prepare silicon during the early stages of chip fabrication (Reuters, September 24, 2013, Applied Materials, Tokyo Electron deal would create titan).

Gary Dickerson, President and CEO of Applied Materials, and Tetsuro Higashi, Chairman, President and CEO of Tokyo Electron, in Tokyo, Japan for the announcement.

The technology that’s involved is wondrous and sealed in tens of thousands of process patents with, apparently, very little overlap in their capabilities between the two companies.

However, most of their production is taken up by just three companies – Intel Corporation, Taiwan Semiconductor Manufacturing Company, and Samsung Electronics Company – who are competing with each other to manufacture the most highly functional but lowest cost “chips” that enable most of the consumer electronic technology that we’re familiar with including most computers and flat panel display and solar photovoltaic products.

The as-yet unnamed new company (HoldCo) is expected to be incorporated in The Netherlands with headquarters in both Santa Clara, California and Tokyo, and has most recent combined sales of $12 billion (and two money-losing quarters behind each of them in the past year) and their nearest competition is ASML Holding NV (sales $5.8 billion), Lam Research Corporation ($3.6 billion), and KLA-Tencor Corporation ($2.8 billion) for a total of $24 billion per year in the industry.

Mr. Dickerson and Mr. Higashi will continue to serve as CEO and Chairman, respectively, in the new company, and each share of the current Applied Materials (1.203 billion shares) will receive one share in the new company, and each share of Tokyo Electron (180.6 million) will receive 3.25 shares in the new company so that, effectively, the current Applied Materials shareholders will hold 68% of the common stock of the new company.

AMAT How We Got Here

Courtesy: Applied Materials

The deal is uncomplicated and pro forma whether we look at it from the point of view of the market value, the enterprise value, or the price of risk.

Please see Exhibit 1 below.

Based on the current market values, Applied Materials should (fairly) own 68% of the combined company, calculated as 68% = $18042/($18042 + $8669) at ambient stock prices of $15 (Applied Materials) and $48 (Tokyo Electric) before the deal; and based on the enterprise value, 69% = $22840/($22840+$10030) in which we have included $2.5 billion in cash and near cash that is owned by Tokyo Electron.

Exhibit 1: HoldCo – Applied Materials Incorporated + Tokyo Electron Limited

HoldCo

(Please Click on the Chart to make it larger if required.)

The price of risk, however, is more enduring than either of these measures and also gives an estimate of the fair value of the stock price of the combined company.

We cannot say, however, what the issue price will be; only that if it differs from $12.22 per share, a price above that will need to be earned (and it likely will be; please see below), and a price below that is too low, and possibly (and most likely) a bargain, which is unlikely.

The company has plans to support the stock price by buying in about $3 billion of it, and the earnings of the combination are deemed to be accretive because there is little overlap in their two businesses; and, their competitive position is improved by both their size and improved ability to develop the new products that are being demanded by their customers.

Respecting those facts, and that the current stock price of Applied Materials is up almost 3% to $17.50, we would not expect an issue price of less than $15 and that HoldCo will support that price, or higher, by buying in up to 200 million shares of its own equity.

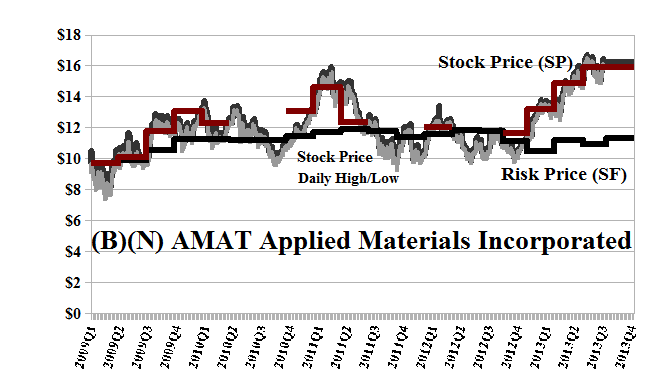

Applied Materials has also been in the Perpetual Bond™ since much lower prices of $11.50 last year (please see Exhibit 2 and 3 below). Our estimate of the downside in the stock price is minus ($2) per share and the stock price is up +50% since December. The company also expects to pay a dividend of $480 million to its shareholders this year for a current yield of 2.5%.

Exhibit 2: (B)(N) AMAT Applied Materials Incorporated – Risk Price Chart

(B)(N) AMAT Applied Materials Incorporated

Applied Materials Incorporated provides manufacturing equipment, services and software to the global semiconductor, flat panel display, solar photovoltaic and related industries.

(Please Click on the Chart to make it larger if required.)

From the Company: Applied Materials Incorporated provides manufacturing equipment, services, and software to the semiconductor, flat panel display, solar photovoltaic (PV), and related industries worldwide. The companys Silicon Systems Group segment develops, manufactures, and sells a range of manufacturing equipment used to fabricate semiconductor chips or integrated circuits. This segment offers systems that perform primary processes used in chip fabrication, including atomic layer deposition, chemical vapor deposition, physical vapor deposition, electrochemical deposition, rapid thermal processing, ion implantation, chemical mechanical planarization, wet cleaning, and wafer metrology and inspection, as well as systems that etch or inspect circuit patterns on masks used in the photolithography process. Its Applied Global Services segment provides products and services designed to improve the performance and productivity, and reduce the environmental impact of the fab operations of semiconductor, liquid crystal displays (LCDs), and solar PV manufacturers. The companys Display segment offers products for manufacturing thin film transistor LCDs for televisions, personal computers (PCs), tablet PCs, smartphones, and other consumer-oriented electronic applications. Its Energy and Environmental Solutions segment provides manufacturing systems to produce products for the generation and conservation of energy, as well as manufacturing solutions for wafer-based crystalline silicon applications. This segment also offers roll-to-roll vacuum Web coating systems for deposition of various films on flexible substrates for functional, aesthetic, or optical properties; and roll-to-roll machine for depositing ultra-thin aluminum films for flexible packaging applications. The company serves manufacturers of semiconductor wafers and chips, flat panel LCDs, solar PV cells and modules, and other electronic devices. Applied Materials, Incorporated was founded in 1967, has 14,500 employees, and is headquartered in Santa Clara, California.

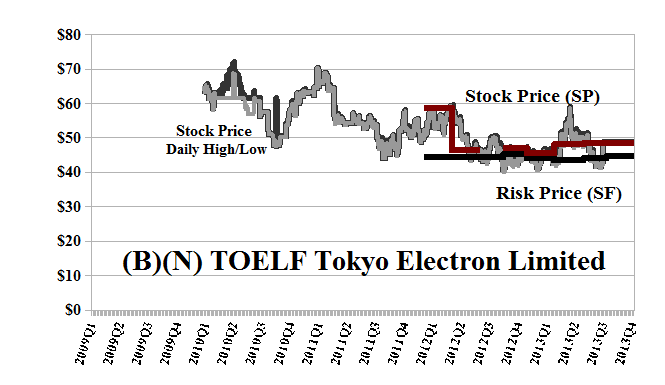

Exhibit 3: (B)(N) TOELF Tokyo Electron Limited (OTC Common Stock) – Risk Price Chart

(B)(N) TOEFL Tokyo Electron Limited

Tokyo Electron Limited, together with its subsidiaries, engages in the manufacture and supply of semiconductor production equipment (SPE) and flat panel display (FPD) production equipment to semiconductor and LCD panel manufacturers.

(Please Click on the Chart to make it larger if required.)

From the Company: Tokyo Electron Limited, together with its subsidiaries, engages in the development, manufacture, and sale of semiconductor production equipment (SPE), flat panel display (FPD), and photovoltaic cell (PV) production equipment to semiconductor and liquid crystal display (LCD) panel manufacturers primarily in the United States, Europe, and Asia. Its semiconductor production equipment includes coaters/developers, plasma etch systems, thermal processing systems, single wafer deposition systems, and cleaning systems that are used in wafer processes, as well as wafer prober systems used in testing processes and other semiconductor production equipment. The companys FPD/PV production equipment product line comprises FPD coaters/developers and plasma etch/ash systems, which are used in the manufacture of displays for personal computers, LCD TVs, and other electronic devices; and plasma CVD systems for thin-film silicon PV cells and end-to-end thin-film silicon PV solutions. It also designs, develops, procures, and distributes electronic components and computer network and semiconductor products centering on integrated circuits (IC), other electronic components, computer networks, and software. In addition, the company provides field support and nonlife insurance services, as well as logistics, leasing, and facility management services. Tokyo Electron was founded in 1963, has 12,000 employees, and is headquartered in Tokyo, Japan.

For more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.