The Ackman Identity

Drama. Mr. Cramer (TheStreet, August 12, 2013, Cramer: If Ackman Has You Smelling Blood…) is taking a public bite out of Pershing Square Capital Management LP, a hedge fund without a web site, in which the founder and general partner, Mr. William (Bill) Ackman, has managed to turn an initial stake of about $50 million in 2004 into current assets of about $10 billion by “shorting & snorting”, that is, by aggressively playing the high-stakes game of “shareholder activism” of which his most recent adventures in Herbalife, J.C.Penny, and the Canadian Pacific Railway are good examples (Bloomberg, August 13, 2013, Bill Ackman, Deactivated).

The Hedge Fund Mirage by Simon Lack, 2012

And much of the hedge fund assets are his, or will be. Studies have shown (see, for example, Simon Lack, 2012) that hedge fund managers or general partners tend to end up owning much of their own fund – assuming that they don’t lose the assets first – and, therefore, that diversification in hedge fund assets (which are now widely regarded as an asset type of “alternative investment” by many pension, trust and endowment plans) by buying funds of funds can only tend to slow down investor losses as their invested capital is steadily and linearly drawn down by the managers.

What else should we expect if they refuse to guarantee any part of the investor capital and much of it is illiquid and leveraged by debt, depending on the hedge fund strategy?

Mr. Ackman’s employees also tend to be graduates of elite business schools, but it is said that he likes diversity as well as adversity – new blood, fresh ideas, so to speak – and has also hired at various times a former fly fishing guide who writes life-style books, a former tennis pro, and “a man whom he met in a cab” (he says) (Forbes, June 29, 2012, The Fishing Guide Who Hooked Hedge-Fund Titan Bill Ackman).

Nevertheless, shareholder activism creates excitement, a surprise, and we have had many surprises in the most recent play-books of corporate theatre; for example, Herbalife, J.C.Penny, Canadian Pacific Railway, Tim Hortons, and the Sony Corporation, many of which involve Mr. Ackman in some way; and there are even more in our Posts on Investo-Mania & Behavorial Pension Disorder (Pension Medicine) and The Activist Investor in which we fashioned the Banzai! and Bonsai! (Defence) Bonds of companies deemed more or less vulnerable to shareholder activism because of poor performance or weak management or weak boards and which have failed to maximize shareholder value, it is said.

“Greenmail”

Courtesy: Richard Scarry (1919-1994)

But we like surprises! It’s a benefit to us because it makes markets and loosens the purse strings, bringing fresh money and new enthusiasms.

And we’re always long on stocks and always maintain a protective position (please see almost any of the (B)(N)-Company reports), and if a hedge fund or investor shorts one of our stocks with multiple billions or hundreds of millions of fresh money (typically leveraged with borrowed money on investor assets which they now own in the limited partnership), our puts are worth money whether they’re right (obviously) or wrong (because the surprise increase in volatility will make our puts more valuable); or we’ll just have to take profits on our stop/loss; and if they start buying it, well … enough said. (Please Click on the Links for more information.)

And, of course, we’re collecting dividends on their short position while they’re paying them on stocks they don’t own (OK) and although we like these companies as they are – that’s why we own them – we might have to sell them or take profits and invest in something else.

But that’s our job and, fortunately, there are lots of fish in the sea and a little noise can help us to find them. We can discover The Ackman Legacy from Schedule 13D filings with the Securities and Exchange Commission (SEC) that are required of investors who take large positions in public companies.

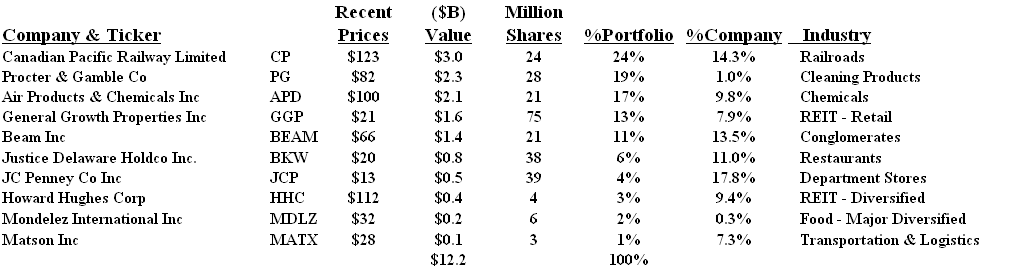

Exhibit 1: The Ackman Legacy circa March through July 2013

The Ackman Identity – Portfolio

(Please Click on the Chart to make it larger if required.)

These are obviously large positions in only ten stocks and, in most cases, a significant ownership interest in the common stock of the company. Mr. Ackman is apparently trimming his holdings in the Canadian Pacific Railway Limited to about $2 billion at the current prices, and he anticipates nearly a year to pull out $1 billion without unduly affecting the stock price; and he’s recently sold his remaining interest in J.C. Penney Company Incorporated, which is currently trading at $13 and down from his purchase price of $20 to $28 three years ago (ibid, TheStreet) but has also sparked the interest of another large investor (Reuters, August 15, 2013, Soros raises JC Penney stake but two big investors exit in Q2); and he’s said to be selling his interest in the major snack and packaged food distributor, Mondelez International Incorporated of Dearfield, Illinois.

Many of these companies have had double-digit gains in the stock price since January (please see Exhibit 3 below, CHG line), and we would expect that Mr. Ackman will make some money under the usual 2/20 formula for hedge fund management fees (that is 2% of the assets under management plus 20% of the capital gains and dividends above the high-water mark before the expenses of running the fund), but it’s unclear that the investors will make any money unless they take it out (ibid, Reuters, August 15) because the assets are still in play.

But, based on what we know (including an abortive short position on Herbalife), it’s unlikely that those gains will match even the +16% that the market has garnished since January; please see Exhibit 2 below, Index line.

Exhibit 2: The Ackman Legacy – Cash Flow as a Perpetual Bond™

The Ackman Legacy – Cash Flow – August 2013

(Please Click on the Chart to make it larger if required.)

Exhibit 3: The Ackman Legacy – Portfolio as a Perpetual Bond™

The Ackman Legacy – Portfolio – August 2013

(Please Click on the Chart to make it larger and again if required.)

The RiskWerk Company is also a hedge fund, but we have none of these problems. The investor capital is always 100% safe and 100% liquid, and we never have an ownership interest in the fund. We just manage the money. Moreover, we are willing to buy and hold any company, in any market, that demonstrates The One Rule – Red line Stock Price (SP) above the Black line Risk Price (SF), and for no other reason – and we don’t need to place large bets on just one or a handful of companies that we don’t own or control.

And we are investors – we want our money to be safe – 100% capital safety – and to obtain a hopeful but not guaranteed return above the rate of inflation; we are not owners, and we never drive from the back-seat, so to speak, or worse, from the back-seat looking backwards using advanced “Weapons of Math Destruction” that are the mainstay of about 80% of hedge fund assets that are not event-driven (such as merger arbitrage, “global macro”, or activist).

The S&P TSX “Depressed” Market as seen by The RiskWerk Company

As an example of The One Rule and portfolio management our way, we have simulated The Ackman Legacy as a Perpetual Bond™ (please see Exhibit 2 and 3 above) and the return – without the Ackman weights – is +22% for the year-to-date through August 16, plus dividends, and the return as managed in the Perpetual Bond™ cannot be less than that for the rest of year, no matter what surprises.

But that return on such a select portfolio is not even 1/3rd of our return on a broad portfolio of more than eighty companies in the “depressed” market of the S&P TSX this year.

And, of course, Mr. Ackman could retire, or get interested in some new venture that he’s probably working on now. We hope so. Please see Exhibit 4 and 5 below.

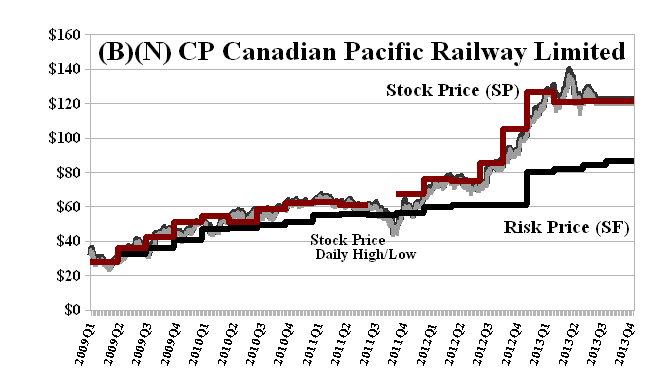

Exhibit 4: CP Canadian Pacific Railway Limited – Risk Price Chart

(B)(N) CP Canadian Pacific Railway Limited – August 2013

It’s possible that Mr. Ackman had something to do with the run-up in the stock price from $60 in 2012 to the current $120 or so, but, after all, it’s not the company that’s buying its own stock, and we don’t see a lot of changes that might be holding the stock price up and well-above the current risk price of $80 (please see Exhibit 3, Risk Price (SF)).

(Please Click on the Chart to make it larger if required.)

Our estimate of the downside due to the demonstrated volatility is minus ($15) (please see Delta in Exhibit 3) and although we could afford the stop/loss at $105, we can also buy the September put at $120 for $2.90 per share and sell an offsetting call at $125 for $1.85 per share, so that for a net cost of holding the stock at $120 to $123 recently, and the cost of the collar at $1.05 per share ($2.90 less $1.85), we could see how this works out for another month, and still collect our dividends of $0.35 per share for a current yield of 1.1% at between $120 and $125 per share. Which prices would surprise, but not hurt us.

Exhibit 5: HLF Herbalife Limited – Risk Price Chart

(B)(N) HLF Herbalife Limited – August 2013

Mr. Ackman and others took a large “short” position in Herbalife Limited, but they seem to have been wrong about the company, and it’s back to trading at $60 and above, and pays a dividend of $0.30 per share per quarter for a current yield of 1.8%.

(Please Click on the Chart to make it larger if required.)

As a result, we made “instant” profits of $20 per share in the first quarter of 2012, and, again, $20 per share early this year on our puts to protect the prices that we had. The current Risk Price (SF) is $58 and our estimate of the demonstrated downside due to ambient volatility is as much as minus ($10) per share. For us, it’s just another play.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.