(B)(N) JCP J.C. Penney Company Incorporated

Deal Book. Since the hasty departure of J.C. Penny’s most recent CEO of less than eighteen months, Mr. Ron Johnson, nobody wants to run it. According to Mr. George Bradt, the Managing Director of the Executive Consulting firm, PrimeGenesis, and an expert in CEO transitions: “Don’t take the job. Actually don’t even take the interview. The less a new CEO candidate has to do with anyone involved with this organization, the better.” – Business Insider, April 10, 2013, Why CEOs should even consider J.C. Penney.

Well, we figured it out. Five minutes with their on-line catalogue convinced us that they have only one problem – too many of the same goods of differing quality and different prices. It’s confusing and pointless. We say: “Sell only good. If you want it good, go to J.C. Penney.”

The hedge fund manager, Mr. Bill Ackman and Perishing Square Capital Management, is J.C. Penney’s largest shareholder at the present time, and they’re apparently sitting on a paper loss of about $500 million which will be difficult to recover, absent a compelling new vision, since sales are down 30% from last year and the company is running at a loss. However, Mr. Ackman says (or insists) that the retailing business can be very lucrative if done right – “If you get a retailer fixed, and you can replicate it, it’s about the best way to make money.” – Reuters, April 5, 2013, Hedge fund manager Ackman says mistakes made in J.C. Penney turnaround.

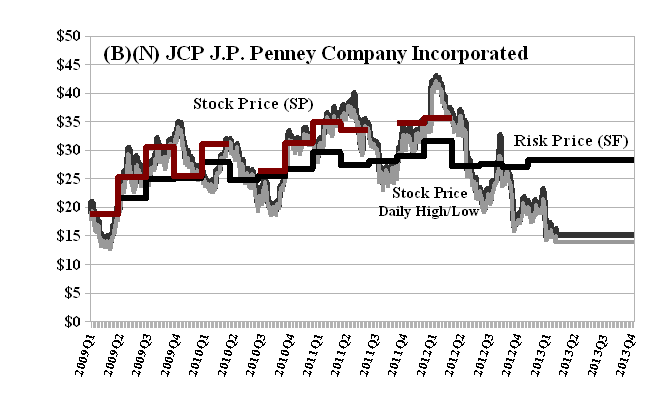

In our view, a better way to make money is not to lose it. We’ve had various opportunities to buy and hold the stock of J.C. Penney (please see Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF)) but sold the last of our holdings at $35 in May of last year, executing the long put that we use to protect our price in situations like this (please see other Deal Books or almost any of the (B)(N)-Company Posts), and have not been tempted to own it since. On the other hand, a defensible acquisition price for the whole company is the Risk Price (SF) which is currently $24 and places a value of $5.2 billion on the company, in contrast to the current market value of $3 billion and stock price of $14.

For that price, we would obtain $2.3 billion of inventories and $5.3 billion of fixed assets (net plant and equipment, net of an accumulated depreciation expense of $2.9 billion), and total liabilities of $6.6 billion, which, undoubtedly, the creditors will be glad to have us take over and continue to service. That would be much more proactive than just buying the “good” socks that Mr. Ackman purchased with his own money at J.C. Penney to show his “good” faith in the company and its management and more than 100,000 employees. – ibid, Reuters.

Exhibit 1: (B)(N) JCP J.C. Penney Company Limited – Risk Price Chart

J. C. Penney Company Incorporated, of Plano, Texas, is a holding company, selling merchandise and services to consumers through its department stores and Direct channels. It offers products including family apparel and footwear, accessories, and fine and fashion jewelry.

(Please Click on the Chart to make it larger if required.)

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation.

Stock prices that are less than the price of risk are “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”. On the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information. Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more details.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.