The Activist Investor

Deal Book. Whenever one of our stocks is in the news, we think about “protecting the price” (and there are lots of examples in these Posts). Like baiting the bear or kicking the sleeping dog, we don’t know what’s going to happen because we’re just bystanders. The noisy activist investor might have a point; maybe there is some value that can be “unlocked”, they say, by a change of the sleeping or sleepy board and management; or maybe the company is worth more if sold in pieces; or maybe it can be tidied up and “flipped” by a hedge fund or venture capitalist to some other firm that can do more with it, or even re-floated in an IPO.

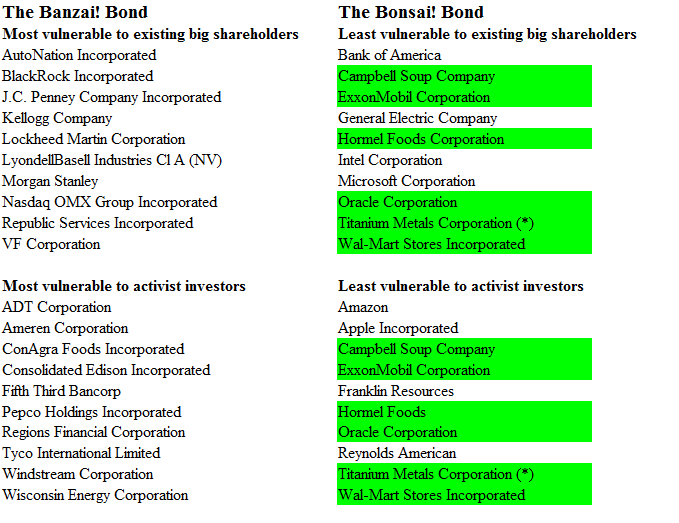

The research firm and M&A consultant, Rotary Gallop, wanted to know what the “tipping point” is for getting control or ownership of a firm. That is, which firms, by name, are unusually vulnerable to “activist takeovers” for whom money is replaced by moxie & proxy, so to speak, and they might end up controlling or owning the firm for next to nothing down; or, which firms are unusually vulnerable to takeover by an “insider block” which is a significant holding but still short – perhaps, far short – of an outright majority; and which firms are resistant to both (Rotary Gallop S&P 500 Control and Vulnerability Reports – The New York Times, April 10, 2013, Report Identifies Companies Vulnerable to Activist Takeovers).

So, we created two portfolios that expose the “activist” situation from our point of view; we’re investors – third parties – and we want our money to be safe – 100% capital safety – and to obtain a hopeful return above the rate of inflation, absent a lot of drama, nips, and scratches that make us look as if we’re just observers and not really “playing the game”. The Banzai! (May You Live Ten Thousand Years) Bond is a Perpetual Bond™ that tracks the recent price performance of twenty companies in the S&P 500 NYSE that are vulnerable (according to Rotary Gallop) to shareholder activism or an insider takeover; and the Bonsai! (Sleeping Bear) Bond of companies that aren’t, and are unlikely to be the object of a takeover because of their size or a controlling block that is unlikely to be moved by a relatively penniless activist.

The Banzai! Bond of companies deemed most vulnerable to a takeover offer has returned (a magnificent) +20% since the end of December, plus dividends, when managed as a Perpetual Bond™, but it has also returned +14% when bought in total and we did nothing else but quietly collect our dividends and the return is comparable to and exceeds the market return during the last several months. In contrast, the Bonsai! Bond of less vulnerable companies has also returned +18% when managed as a Perpetual Bond™ but a negative (-2%), which is about minus (-13%) below the market, when just bought and held – Sleeping Bears, indeed. Please see the Exhibits below.

Exhibit 1: The Activist Investor & Company Vulnerability

Undoubtedly, there is an issue of corporate governance because the shares of the activist investor will be more equal than ours, and a noisy 5 or 10 percent-er might end up owning the company or controlling its future direction, wisely or not, and we are disarmed (and there are several recent examples in these Posts) but not necessarily disrobed; that is, we might not lose our shirts in these imaginative deals and could benefit instead.

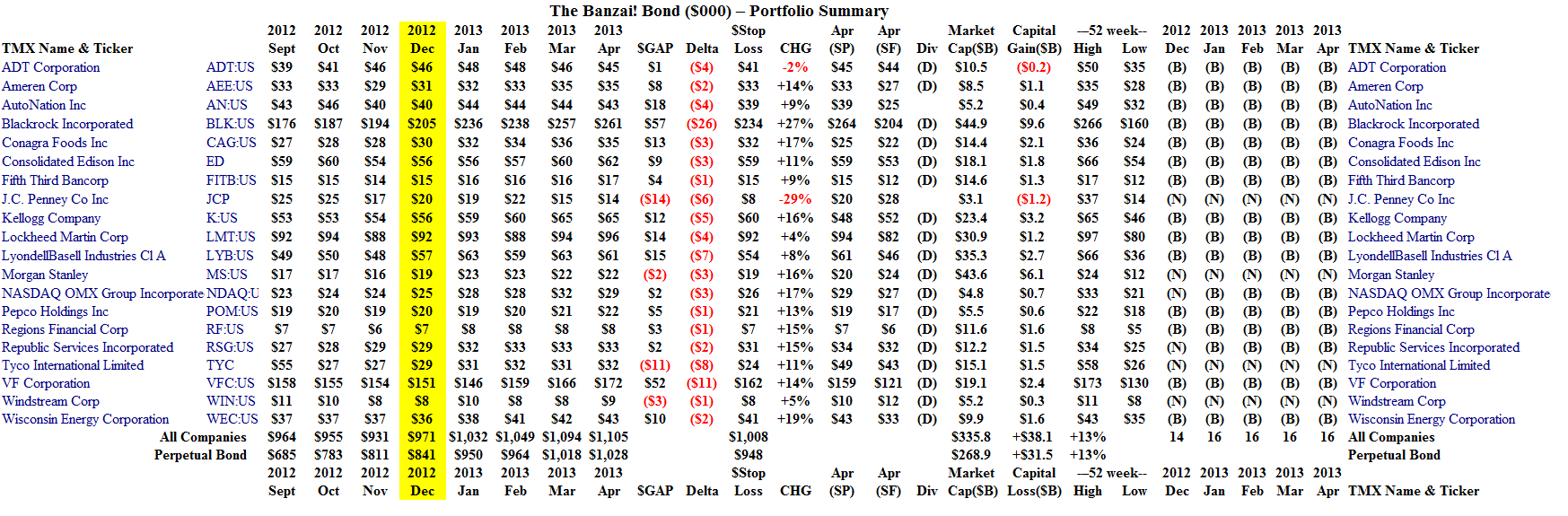

For the Banzai! Bond, we bought two more companies in January (the Nasdaq OMX Group Incorporated and Republic Services Incorporated; please see Exhibit 3 below and note the (N)- to (B)-transition in January) and the Bond currently holds sixteen of the twenty companies.

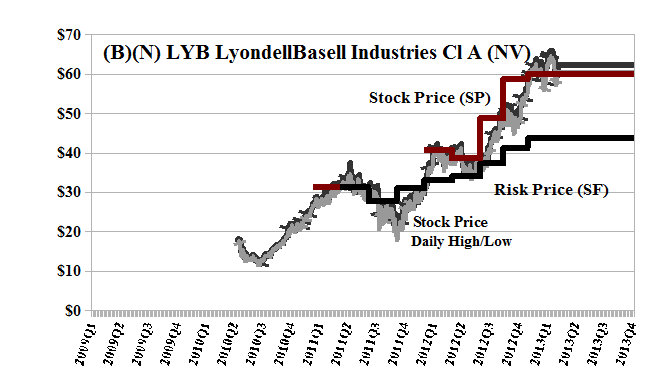

We also note (please see the bottom of Exhibit 3) that both the Banzai! Bond (of sixteen companies) and the All Companies portfolio returned +13% when weighted by the capitalization of the companies. Of these twenty companies, only the J.C. Penney Company is getting “activist investor” attention at the present time (please see our recent Post, (B)(N) JCP J.C. Penney Company Incorporated, April 2013) but the bouyancy of these companies as a group seems to indicate that investors “like” most of these companies and that a takeover offer would be just a bonus. For example, LyondellBasell Industries Cl A (NV) is a Dutch company, listed in New York, that makes chemicals in Rotterdam, and it’s trading well above its Risk Price (SF) of $45 which would be a plausible “acquisition price” should it falter, but a simple “collar” on its current price would make it worth $65 to us regardless of the outcome. In addition, the stock is up +50% since this time last year, and it pays a quarterly dividend of $0.40 per share, or $920 million per year, to its more or less complacent shareholders for a current yield of 2.6%. Please see Exhibit 4 below.

Exhibit 2: The Banzai! Bond – Cash Flow Summary

(Please Click on the Chart to make it larger if required.)

Exhibit 3: The Banzai! Bond – Portfolio Summary

(Please Click on the Chart to make it larger, and again, if required.)

Exhibit 4: (B)(N) LYB LyondellBasell Industries Cl A (NV) – Risk Price Chart

LyondellBasell Industries NV is a plastics, chemical, and refining company. The company produces polypropylene and polypropylene compounds, propylene oxide, polyethylene, ethylene and propylene. It also provides technology licenses.

(Please Click on the Chart to make it larger if required.)

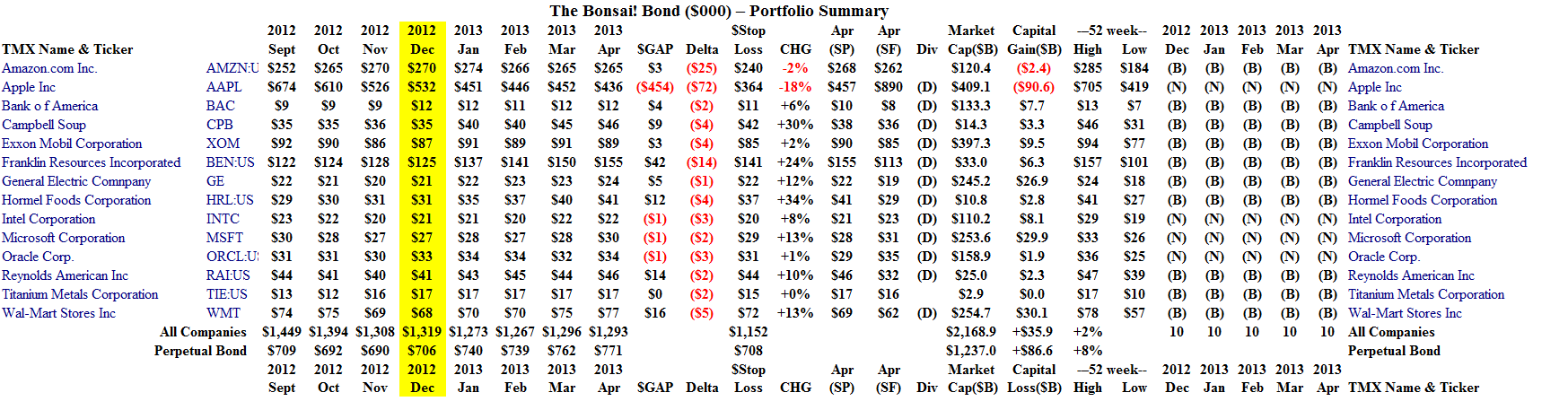

Turning now to the invincibles in the Bonsai! Bond, the Titanium Metals Corporation was taken out in November by the Precision Castparts Corporation of Oregon for a cash payment of $16.50 per share or $2.9 billion, 45% of which went to a small group of companies controlled by the Dallas billionaire, Mr. Harold Simmons (Marketwire, November 19, 2012, Titanium Metals Corp (TIE) Investor Lawsuit to Halt Acquisition by Precision Castparts Announced by Shareholders Foundation); only months before the offer, the stock was trading at $10 and down from $20 in 2011. In effect, that it was closely held made it more vulnerable rather than less vulnerable to a takeover, and the takeover worked against those investors who bought and held the stock at $20 and favoured those investors who had held the stock for a long time or bought it more recently at $10. That could also be true for others of the smaller companies, such as the Campbell Soup Company, Hormel Foods or Reynolds American, for example (and please see our Post on the plight of the H.J. Heinz Company, (B)(N) HNZ H.J. Heinz Company, February 2013) but unlikely in the case of the largest companies such as Amazon, Apple, Bank of America, Exxon, and so forth, with a market value that is well in excess of $100 billion; only the government could take those over and then only if they are too big to fail. Pity that we should be neither able to influence the board and management with our votes nor have a shot at a takeover premium.

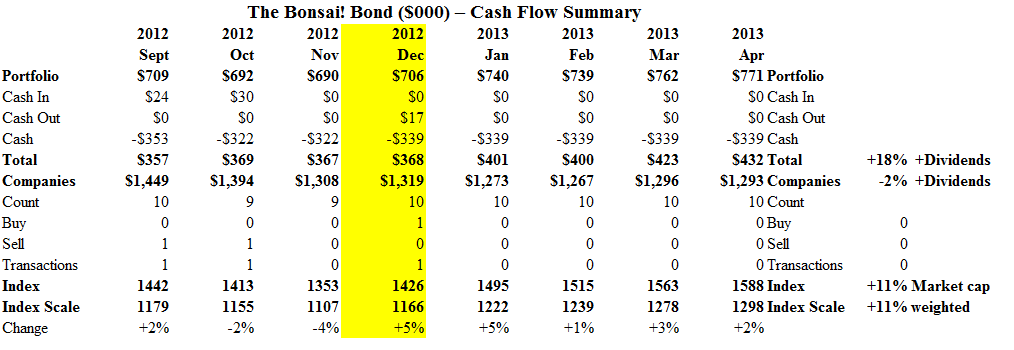

Exhibit 5: The Bonsai! Bond – Cash Flow Summary

(Please Click on the Chart to make it larger if required.)

Exhibit 6: The Bonsai! Bond – Portfolio Summary

(Please Click on the Chart to make it larger, and again, if required.)

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.