(B)(N) SNE Sony Corporation ADS

Deal Book. Piracy in the music industry has a familiar meaning, but it now has a new name that is emerging in mergers, acquisitions, and spin-offs by greenmail (Reuters, May 15, 2013, U.S. hedge fund calls for Sony Entertainment spin-off and our recent Post, O’the Slings And Arrows Of Outrageous Fortunes, March 2013). The fabled hedge fund manager, Mr. Loeb of Third Point LLC, has taken a proprietary interest in the business of the Sony Corporation, and says that the company has a “hidden gem” in Sony Entertainment; and we are immediately minded of Edgar Bronfman Jr, scion of the Seagram’s fortunes, who also watched a lot of television, and directed the fortunes of Vivendi Universal Entertainment from hero to zero in just two years, which is itself amazing and the stuff of tragic comedy symptomatic of the times with the AOL Time Warner debacle occurring at about the same time (please see our recent Post, (B)(N) AOL AOL Incorporated, May 2013).

For the instant replay, Mr. Loeb’s stake in Sony “The Company” is currently about 6% of the stock which is worth $1.1 billion at the current price of $20 and up significantly since $10 in December, so what the “stake” cost is not known – it could be as low as $500 million on the open market in December, but Mr. Loeb has also said that his group can raise another $1.97 billion, which is nearly two weeks of revenue for the entertainment giant and nearly 2% of the current liabilities of $137 billion (which is pricey and costing the company about $9 billion per year).

While other companies are trying hard to buy “content” (such as BCE and Astral Media, please see our Post, (B)(N) BCE BCE Incorporated, October 2012), Mr. Loeb has suggested that Sony should “dis-integrate” Sony Entertainment and exciting products such as Beyonce, Adele, and Spider-Man, and reduce its ownership from a full 100% to 80% for the sum of, who knows what, two weeks of revenue and a good laugh, nothing that Sony can’t do for itself with a little bit of paperwork – if it wanted to and wanted to “insulate” and “in-centify” the management from the current woes of Sony “The Company”; but one doesn’t see a lot of future in selling the jewelry to add (maybe) $10 per share (ibid, Reuters) – and maybe for a short time because the market is fickle – to the shareholder value of “The Company” that produces consumer electronics in tough competition with Panasonic of “The Breakfast Collection”, Samsung, and a raft of niche competitors with a song and a chip.

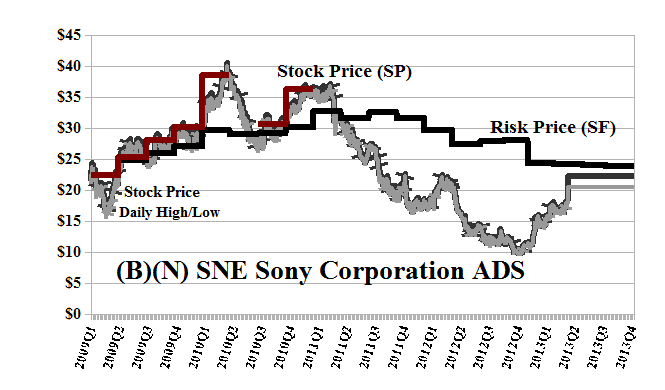

We can’t play at the present time because the company is trading below the Risk Price (SF) of $24 and we last held it at $40 to $35 two years ago (Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason). Sony is not paying dividends at the present time.

Exhibit 1: (B)(N) SNE Sony Corporation ADS – Risk Price Chart

(B)(N) SNE Sony Corporation ADS

Sony Corporation and its subsidiaries are engaged in the development, design, manufacture, and sale of various kinds of electronic equipment, instruments, and devices for consumer and industrial markets.

(Please Click on the Chart to make it larger if required.)

From the Company: Sony Corporation designs, develops, manufactures, and sells electronic equipment, instruments, and devices for consumer, professional, and industrial markets worldwide. It offers consumer products and devices, such as televisions; Blu-ray disc players/recorders, home theaters, home audio systems, and DVD-video players; compact digital, home-use video, and interchangeable single-lens cameras; and personal computers and memory-based portable audio devices. The company also develops, produces, markets, and distributes PlayStation3, PlayStation Vita, PlayStation Portable, and PlayStation 2 games hardware and related software. In addition, it provides professional devices and solutions, such as broadcast- and professional-use products, and other B2B business solutions; CMOS image sensors, CCDs, system LSIs, and other semiconductors; batteries, audio/video/data recording media, storage media, optical pickups, and optical disk drives; and materials and components for electronic devices, such as anisotropic conductive films. Further, the company engages in the acquisition, production, and distribution of television programs, motion pictures, and animated films; operation of television networks and studio facilities; creation and distribution of digital content; development of new entertainment products, services, and technologies; and music publishing business. Furthermore, it provides various financial services, including insurance, savings products, and loans; engages in the research, development, design, production, marketing, sale, distribution, and servicing of mobile phones, accessories, services, and applications, as well as original equipment manufacture of mobile phones; manufactures Blu-ray, DVD, and CD disks; and provides Internet and medical-related Internet services. The company was formerly known as Tokyo Tsushin Kogyo Kabushiki Kaisha and changed its name to Sony Corporation in 1958. Sony Corporation was founded in 1946 and is headquartered in Tokyo, Japan.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.