(B)(N) GOOG Google Incorporated

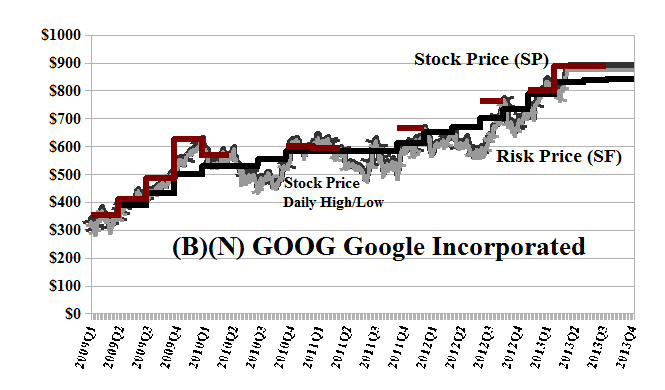

Drama. Google Incorporated has finally made it into the Perpetual Bond™ with substantial “likeability” at the current stock price of $900 (which is already off a little from $910 obtained earlier today) and 1,000 shares cost $900,000; and it’s evident that the “Big” money is driving the price, and stopped feeding on Apple Incorporated, maybe for a long time (FOX Business, May 15, 2013, Next Stop $1,000? Google Soars Above $900, Unveils Music Service). Please see Exhibit 1 and 2 below, and our recent Post, The New Wave Markets, May 2013, for some real insight into what’s going on.

The current Risk Price (SF) is $840 which is substantially below the current stock price of $900 and we were already buying the stock at much lower prices of $800 and a Risk Price (SF) of $730 to $780 a few months ago (Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason).

The company doesn’t pay a dividend and the only way that the big money can make money on it, is by buying and selling it to each other – for example, The Farmer’s Co-Op Pension Plan to the Electrician’s Union, and so forth. Our estimate of the price downside due to the demonstrated volatility is minus ($80) and the stock could be trading anywhere between the current $900 and $820 and $980 and we would not be surprised, although a lot of programmed traders and pensionnaires, would be. Please see our recent Post, The Pensionnaires, May 2013.

The options market is huge and we can protect our current price by buying the July put at $900 for $32 today, and sending out a flyer, selling the July call at $950 for $20, so that for a net cost of holding the stock at $900 and the cost of the “collar” at $12 per share ($32 less $20), we can expect to keep the stock at no less than $900 and no more than $950 for the next three months, and hopefully work the options up and forward as the future unfolds.

Who said that the stock doesn’t pay dividends? A slightly more aggressive play is to sell the July call at $915 which is selling for $33 today, so that we could make $1 per share and possibly not get sold out at $915 before July, but that seems to require a lot maintenance, and runs strongly counter to the current enthusiasm for the stock at $1,000(?), absent some “profit taking” and “back fill” (please see our New Wave post) and the continuing good works of the company.

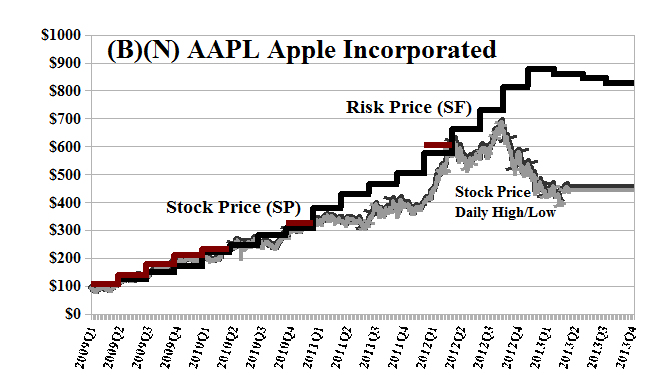

In contrast, Apple Incorporated can’t sell the stock for buying it at a current dividend of $3.05 per share per quarter, or $12 billion per year to the shareholders for a current yield of 2.9%. Please see Exhibit 2 below for the current story on just another iThing.

Exhibit 1: (B)(N) GOOG Google Incorporated – Risk Price Chart

(B)(N) GOOG Google Incorporated – May 2013

Google Incorporated maintains an index of web sites and other content, and makes this information freely available to anyone with an Internet connection.

(Please Click on the Chart to make it larger if required.)

Exhibit 2: (B)(N) AAPL Apple Incorporated – Risk Price Chart

(B)(N) AAPL Apple Incorporated – May 2013

Apple Incorporated designs, manufactures, and markets personal computers, mobile communication devices, and portable digital music and video players and sells a variety of related software, services, peripherals, and networking solutions.

(Please Click on the Chart to make it larger if required.)

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.