The New Wave Markets

Drama. An investment is just and only the purchase of risk, and the risk is that we might not get our money back and a hopeful return above the rate of inflation, which, if we don’t, is just another way of losing our money because we can buy less later with our money than we can buy now.

All of that can be re-stated as “an investment is just and only the purchase of risk and the risk is that we might not obtain a non-negative real rate of return”; and, when stated that way, the definition of an “investment” and “risk” is equally evocative in cases of inflation, which is the norm and our “money” as cash in our pocket can be expected to buy less in the future than it can buy now, and deflation in which our “money” as cash in our pocket can be expected to buy more in the future because the demand for goods and services has waned, or, in some cases, the supply of goods and services has waxed and the market is flooded with goods and services for which there are not enough buyers.

That simple paradigm keeps us fully invested in the “equities” market, at all times, because we can show – prove in mathematical and economics terms – that the “cash” in our pocket can never be as “good” as an investment that is both “as good as cash” and “better than money” when we buy it (the investment) at a “price” that we can calculate as the “price of risk”. For more on these concepts, please see our recent Post, Bystanders & Collateral Damage, which provides more information and references.

Large investors, such as mutual funds, endowment and trust funds, and pension funds, address the exact same problem of a return on “cash” as “money” when it is invested, by strategically shifting their investments between their portfolio of equities, and their portfolio of bonds which are priced according to the demonstrated inflation now and their expectation of a different rate of inflation in the future. Such as, typically, 60% bonds/40% equities expecting “lower inflation” than now, or 40% bonds/60% equities expecting “higher inflation” than now.

For example, if the rate of inflation is high, now, then bonds can only be sold at a serious discount, and we can buy $100 a year from now, for $95 now, reflecting a known 5% rate of inflation and the anticipation that it will not go any, or much, higher; if it does, then the price of their bonds will go down, and if they have an unanticipated liquidity problem, then they might have to sell them at a lower price than what they paid for them.

On the other hand, if inflation is not high now, but expected to be high or higher later, then we shouldn’t be buying bonds at all because the price of the bonds that we own will go down if inflation is, in fact, higher later.

And, on the other hand (again), if inflation is “high” now, why should we expect it to be even “higher” later; what does “high” mean, anyway, when a burgeoning economy can be growing at rates of 6% or more, and it feels good to own companies?

The “bond paradigm”, then, is the easiest of all the investment paradigms because there is only one variable – inflation – although it is commonly made much more complicated by buying and selling bonds in foreign currencies so that now we need to consider two or more rates of inflation, and the relations between them (which increase exponentially), and the rate of exchange between the currencies, which is subject to the demand and supply of goods and services, and many surprises such as wars, civil unrest, and natural disasters in strange locales. Notwithstanding all of that, nobody knows how to forecast inflation anyway.

“Big” money doesn’t have much choice. The bond market is at least ten times as big as the equities market, and “big” money can only buy so much of a stock without “stating its intentions” and possibly making a bid for all of it. “Big” money, then, needs to buy whole barrels of stock – dozens, if not hundreds of companies – and the barrel could very well have a weak RIM (Research in Motion) or a bad Apple, that they didn’t expect because the companies are bought and sold by the “bag” according to the needs of the Capital Assets Pricing Model (CAPM), which has nothing to do with “investment risk” as we defined it, but only adherence to some vague standard of “volatility” and “co-volatility” to reduce “volatility”. What?

Our approach to such large portfolios is, of course, quite different, and it’s different because we know the price of risk for all the equities in them, with at least the same certainty that a bond holder might know the price of risk for a bond, and why it is what it is. Please see below for more information and additional references.

Which brings us to the real goat of the day and the partisans of The New Wave Markets – small investors with $10’s of thousands or possibly some millions, to “madly” invest (The Street, May 13, 2013, Cramer’s ‘Mad Money’ Recap: A Surreal Market). As we noted above, for every $1 invested in the equity markets, there’s at least $10 invested in the bond markets, and when the latter start to move from 60/40 to 40/60, tired of the real sub-zero yields, then, “This is not just a pipe”, anymore, and we’d better believe it. Or be smoked by volatility.

Exhibit 1: The Real Sub-zero Imaginary

Yields of the “Big” Money Post-2008 – Volatility Risk Chart

René Magritte (1898-1967)

Mr. Cramer is now “astounded” that the markets appear to be so “unpredictable” and confound the received wisdom of the ages.

He has noted, specifically, that the stock prices of Whole Foods Market, Walt Disney, and Domino’s Pizza, all ran up before their earnings reports – good or bad – but then kept on running and, so, “profit takers” didn’t, instead of “profit takers” do, which is, apparently, the usual thing to do – just take the money and run – because who knows where it came from?

The next challenge to “real analysis” is that the stocks Williams-Sonoma and Restoration Hardware, “gapped higher” but, then, didn’t retreat to fill in the gap, before “gaping still higher” and higher again, with no deference to “consolidating” the gap.

And finally, the companies 3M, Caterpillar, and Emerson Electric, all shared “gloomy outlooks” and “dismal earnings” but the stock prices sought the light, and surged upwards. How can this be?

Well, it’s easy. All of these companies that didn’t do what Mr. Cramer expected, are in the Perpetual Bond™; and the one company (Caterpillar) that did do what Mr. Cramer expected, just took a little longer to do it, and it is an (N) and is not in the Perpetual Bond™. Caterpillar ran up to $95 and just below the Risk Price (SF) of $95, but then retreated to $87 where it is today. Please see our Post, The Dow (B)-Nots, April 2013, for more details, and for the others, our Posts, The Risk Adjusted Dow, March 2013 for 3M, (B)(N) DIS Walt Disney Company, April 2013, and Whole Foods Market and Emerson Electric, The Wall Street Put, April 2013.

That leaves only Dominos Pizza, Williams-Sonoma, and Restoration Hardware Holdings Incorporated (which is new to the database) below, and these charts are transparent to us and we know exactly what they mean and what to do:

Exhibit 2: (B)(N) DPZ Dominos Pizza Incorporated – Risk Price Chart

(B)(N) DPZ Dominos Pizza Incorporated

Domino’s Pizza Incorporated through its subsidiaries is engaged in retail sales of food through Domino’s Pizza stores; sales of equipment and supplies to Domino’s Pizza stores and receipt of royalties from domestic and international Domino’s Pizza franchisees. Its head office is in Ann Arbor, Michigan.

(Please Click on the Chart to make it larger if required.)

Dominos is a kind of financial phantasmagoria because its net worth is grossly negative (minus $1.3 billion) and several times below its total assets ($500 million); it pays a total dividend of $45 million per year for a current yield of about 1.5% on gross revenues of $1.7 billion.

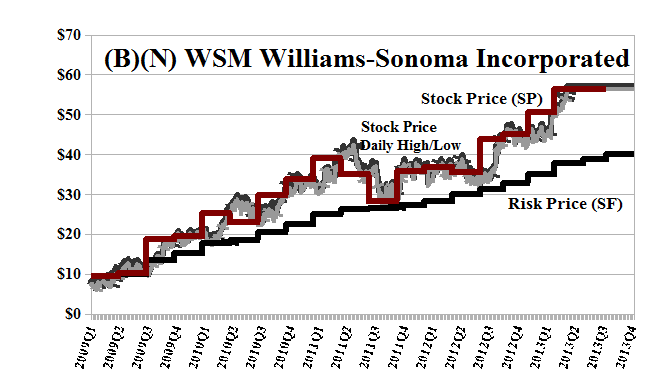

Exhibit 3: (B)(N) WSM Williams-Sonoma Incorporated – Risk Price Chart

(B)(N) WSM Williams-Sonoma Incorporated

Williams-Sonoma Incorporated is a multi-channel specialty retailer of home furnishings in the United States and Canada, based in San Francisco, California.

(Please Click on the Chart to make it larger if required.)

Exhibit 4: (B)(N) RH Restoration Hardware Holdings Incorporated – Risk Price Chart

(B)(N) RH Restoration Hardware Holdings Incorporated

Restoration Hardware Holdings Incorporated operates as a luxury brands in the home furnishings marketplace offering furniture, lighting, textiles, bathware, decor, outdoor and garden, as well as baby & child products from Corte Madera, California.

(Please Click on the Chart to make it larger if required.)

It came out as an IPO at $24 in November last year.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.