The Lonely Hunters (Hedge Funds)

Drama. “Hedge funds” have been around since the beginning of the insurance industry as an investment activity that began with Lloyd’s of London in the 17th century. The modern application of “hedge funds”, as a technology to manage the asset and liability mix (the ALM), is used by insurance companies who must control for the value and liquidity of their assets and liabilities in order to contractually pay claims as they might be expected to come due.

However, today’s “Hedge Funds”, despite their name, are nothing like that, and would be recognized by 17th century investors as a bare-backed “trading venture” and long-necked “speculation” by a visionary that has nothing to do with the prudent investment of money in order to assure the payment of claims as they might be expected.

That’s left to the investors, which include most of our insurance companies and pension plans, who are hoping to win the lottery and a windfall that might solve all their problems, but end up searching for a landfall (and government guarantees and bail-outs) because there is no assurance of the bare minimum – capital safety and liquidity – in the pursuit of the visionary – and if there were, it would be in the guarantee of which there is inexcusably none (please see our recent Post, The Pensionnaires, May 2013).

As Mr. Buffett has said “We won’t know what shorts they’re wearing until the tide goes out.” And the tide’s gone out (Reuters, May 16, 2013, More top hedge funds dumping Apple).

It’s not really important to us, who did what and when, and for how much (and that is explained in the article, ibid Reuters, and these data are available in the quarterly 13-F regulatory reports of the U.S. Securities and Exchange Commission (SEC) and are required from the thousands of alleged “hedge funds” that are available to investors) but they’re unlikely to stop doing what they’re doing as long as they’re cashing in now and then and drawing management fees. And we also need aggressive investors and shareholders in the market.

But we, who are risk averse investors in these same markets – pastoral, if you like – should look at the companies that they’re “investing” in, not because we need a vision, but because it’s very “big” money that’s being tossed about, and we have more than a fair chance to get a better outcome for ourselves – which is our job – while they pommel each other, so to speak, and waste or re-allocate our pension and endowment funds amongst themselves.

For example, in the last quarter, the hedge fund Passport Capital bought 2.2 million shares of Yahoo! Incorporated (of which there are 1.1 billion outstanding), but Tiger Global Management sold 14 million shares worth about $350 million and the stock is currently trading at $27 up from $20 last year, and $15 for the three years prior (please see Exhibit 1 below and our earlier Post, (B)(N) YHOO Yahoo! Incorporated, November 2012).

Exhibit 1: (B)(N) YHOO Yahoo! Incorporated – Risk Price Chart

(B)(N) YHOO Yahoo! Incorporated – May 2013

Despite all of that vision, we did just as well or better and did not begin buying the stock until the ambient stock prices appeared to be at or above the price of risk (Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason).

(Please Click on the Chart to make it larger if required.)

And now, we are not selling it but holding it with a stop/loss in place or a “collar” to protect our price and profit against “surprises” (such as bad news or some hedge fund bailing out to solve its own liquidity problem).

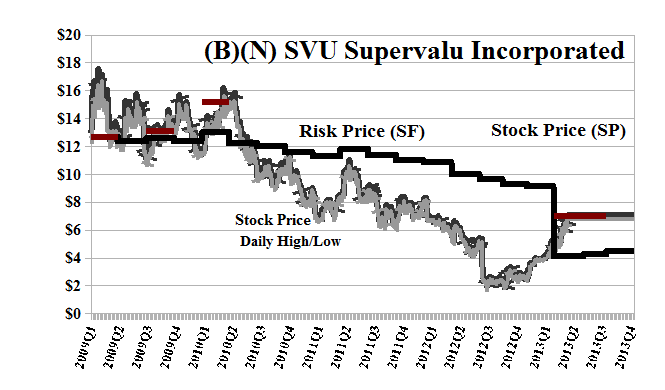

As another example, consider Supervalu Incorporated and the plight of its 35,000 employees and their pension plan (please see our previous Post, (B)(N) SVU Supervalu Incorporated, December 2012). This is not the same company that we looked at in December; after months of petitioning, the hedge fund, Cerberus Capital Management, failed to acquire the company but bought some of its assets for $3.3 billion. Please Exhibit 2 below.

Exhibit 2: (B)(N) SVU Supervalu Incorporated – Risk Price Chart

(B)(N) SVU Supervalu Incorporated – May 2013

We missed the long slide from $16 to $2 and neglected to pick it up at $2 late last year for the usual reasons. Who knows the future? All we can really know, with reasonable certainty, is now.

(Please Click on the Chart to make it larger if required.)

After the Cerberus deal, the hedge funds, Jana Partners and Omega Advisors, jumped in to buy 14 million shares and 6.9 million shares, respectively, so that they hold almost 10% of the stock between them; on the other hand, the hedge fund Coatue Management lost heart, pulled the trigger, and “dumped” its 10 million shares at $5 to $6 per share, and likely for a good profit, but no future.

The Risk Price (SF) has dropped considerably from $9 to $4 and the current liabilities from $2.7 billion to $1.2 billion; and the inventory from $2.4 billion to $900 million; and the stores from $6 billion to $1.7 billion (net) but the total liabilities have increased from $12 billion to $12.5 billion and the shareholders equity has plunged from near zero to minus ($1.4 billion) (which is not necessarily “bad”; please see our recent Post and Dominos Pizza in The New Wave Markets, May 2013). We could buy it because the stock price is above the Risk Price (SF), but we don’t know if it will stay there, particularly if the company is still in play. The company doesn’t pay dividends and who knows who will short it next, try to take it over, or change the management.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.