(B)(N) The Easy (EC) Theory of the S&P 500

Big Bertha 42cm M-Gerät Howitzer “Underlying”

Drama. We’ve noted in these Posts that “earnings don’t matter” – and that’s a fact – and also that “fundamentals don’t matter” because virtuous balance sheets and a policy of paying dividends don’t necessarily attract a “good stock price”; “frenzy” matters, but it’s unpredictable, and where there’s “frenzy”, there’s also likely to be some well-heeled hedge funds, or investor “groups”, who are bidding, or talking, the prices up, or down, and are ready to leave when they find a convenient new opportunity.

Fooled again! Protest! Courtesy: Banksy

And, of course, we have to deal with the “weapons of math destruction” – derivatives and securitizations – for which the “underlying” is the least important part.

But we don’t see any evidence that the problem is in the “stock market”, which (in our view) does a spectacular job with admirable efficiency and low costs, and it is one of the few things on the planet, of that scale, day-after-day, that actually works, and drives the “capital” to where it’s wanted

The hallmark of a subsistence economy is the absence of a working “stock market”, and absent the stock market, we need to go to the “castle” for what we want, and there are large parts of the world, and billions of people, that still need to do that, because in those parts of the world, alleged “capitalism” is just a licence to steal.

Are we to be “bystanders”, then, and “collateral damage”, or should we hire “professional managers” with a gift for “gab” and little else, because there is no theory that might help them (and no offence is intended).

But there are three words that move us – safe, liquid, and hopeful – and if we don’t hear those words, we know that it’s not an investment. And that’s the answer – investment professionals need to say those words, and write them into their contracts and the investor can choose to write them out, if they want. That’s professional.

And for the real theory, the one that works – safe, liquid, and hopeful – please see our Posts.

In our New York database, which includes the S&P 500, there are currently 512 companies that are “(EC)-smart” and have a market value of less than $100 billion, pay dividends, and demonstrate a Company E or Company C modality, affirming that they are well-funded and not living hand-to-mouth, month-to-month, for whatever projects they’re undertaking, including the likely payment of dividends; please see Exhibit 1 below (and click on the chart, and again, to make it larger if required).

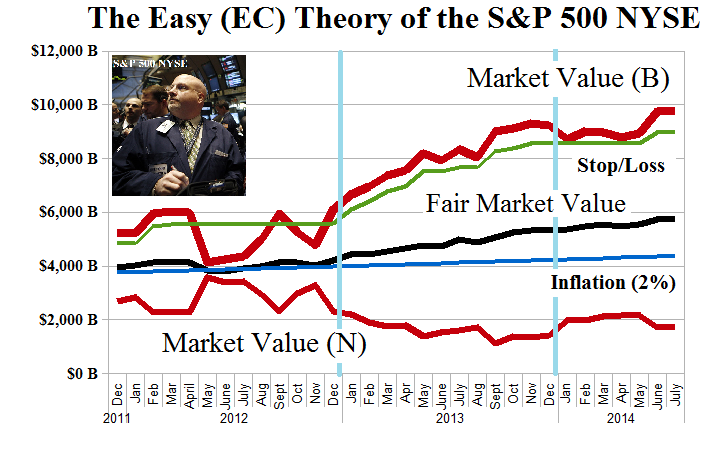

Exhibit 1: The Easy (EC) Theory of the S&P 500 NYSE – Fundamentals – June 2014

The Easy (EC) Theory of the S&P 500 NYSE – Fundamentals – June 2014

Figure 1.1: The Easy (EC) Theory of the S&P 500 NYSE – Risk Price Chart – June 2014

Figure 1.2: The Easy (EC) Theory of the S&P 500 NYSE – Fair Value Chart – June 2014

With reference to Figure 1.1, there are more than 500 companies in this portfolio and each of them has a market capitalization of less than $100 billion; they all pay dividends and they are all “EC-smart”; of course, the other four hundred or so companies that we follow, should not be said to be “EC-dumb” – they merely have a Company A, B, or D-modality, and different challenges.

The current market value is $11.5 trillion which is up +27% and $1.1 trillion last year, and a further $821 billion and +7.7% so far this year; they also paid dividends of $229 billion for a return of earnings of 37% and an aggregate dividend yield of 2%; please see Exhibit 1 above for further details.

We’ve set the stop/loss aggressively, at 96% of the stock prices, reflecting our estimate of the aggregate quarterly volatility of minus (-8%); the “flat”-spots (green line above the Market Value ($B)) just mean that we’ve hit the stop/loss in a number of companies, but not necessarily all of them; we have some cash, and we can buy back those companies which are still trading above the price of risk at a lower price, and the rest are still paying dividends.

However, the portfolio is never worth less than the stop/loss price, and the stop/loss is usually set by company rather than in aggregate, and it never declines because when a company is at the stop/loss, we’re just into cash on it, and the minimum portfolio value, including the cash, is its value at the stop/loss prices (as shown in Figure 1.1 and 1.2).

The “Fair Value” (Figure 1.2) is the average of the (B)-companies at the price of risk and the (N)-companies at the price of risk (not the stock price) and it is based on the precept that the companies that are trading at or above the price of risk are “undervalued” because there is an excess demand for them over supply at the current stock prices; and the (N)-companies are “overvalued” because there is an excess supply of them over demand at the current stock prices.

Noise – The Capital Assets Pricing Model (CAPM), Modern Portfolio Theory (MPT), and the “Risk/Reward Equation”

The Perpetual Bond™ (Figure 1.2) is easier to manage because we know exactly that a company is in the portfolio if and only if is trading at or above the price of risk, and that’s the only the reason that we have for owning it. The equal-weighted by value Perpetual Bond™ in the same market returned +42% last year and is up a further +14% so far this year; moreover, there’s no reason to weight them in any other way than by “equal value” – anything else is just noise or speculation.

The Perpetual Bond™ in this market currently holds 408 of these companies, which is down from 426 in December, and the method has also suggested 164 transactions in the last six months (73 buys and 91 sells, but only 136 transactions in all of last year), not all of which we need to make, respecting available new information and market uncertainty about “stock prices” that set-in in March; please see Figure 1.2 above.

It might seem “daunting” and “unfamiliar” to think about a domain of more than 500 companies that is not an index or an ETF, but the “number” of companies has very little to do with it, and the budget constraint is the primary concern.

To reduce the portfolio size in terms of the number of companies, we picked a random number between 200 and 400, and then counted down and up every tenth company (decimation) to include in the domain of the “(Small) Easy (EC) Theory of the S&P 500 NYSE”; please see Exhibit 2 below and click on it (and again) to make it larger if required.

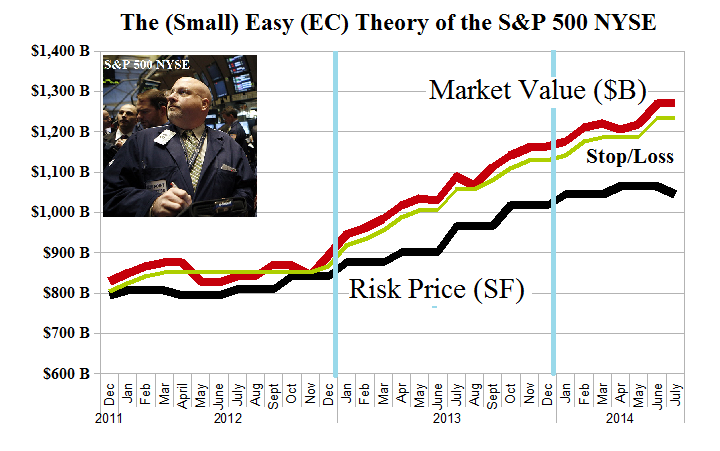

Exhibit 2: The (Small) Easy (EC) Theory of the S&P 500 NYSE – Fundamentals – June 2014

The Easy (EC) Theory of the S&P 500 NYSE – Fundamentals – June 2014

Figure 2.1: The (Small) Easy (EC) Theory of the S&P 500 NYSE – Risk Price Chart – June 2014

Figure 2.2: The (Small) Easy (EC) Theory of the S&P 500 NYSE – Fair Value Chart – June 2014

There are only 52 companies in this domain, but they gained, in aggregate, +26% last year, and also paid dividends of $33 billion for a return of earnings of 41% and a dividend yield of 2.2%; please see Exhibit 2 above and Figure 2.1 on the left.

However, the Perpetual Bond™ in these same companies – “randomly” selected from the “big” Easy (EC) market – returned +41% last year and is up another +16% so far this year; please see Figure 2.2 and click on the links “The (Small) Easy (EC) Theory of the S&P 500 NYSE – Fundamentals, Prices & Portfolio, Portfolio & Cash Flow Summary” for further details.

With smaller portfolios (by number), we’re more likely to be in cash and collecting dividends, but it’s evident that “volatility” has nothing to do with it, and that the “fundamentals” in terms of virtuous balance sheets and “earnings” have nothing to do it; nor is the market to blame.

The Contract

Now that’s Professional.

Moreover, there’s no problem with the contract – 100% capital safety and 100% liquidity and a hopeful but not necessarily guaranteed return above the rate of inflation. Those are the words that move us – safe, liquid, and hopeful.

Anything else is just a gamble or a speculation, and fifty-years of failing to say those words ought to have proved that by now, as most pension funds, endowment funds and retirement plans are facing some serious “deficiencies” and are helped only marginally by the current “bull market”.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}

{kind=link}