(P&I) Demand and Supply

And the only one that matters is … Demand

Essay. The most common and prevailing mistake that economists make and which tends to render their discourse into an engaging babble with an unfortunate undertow, is to equivalence the demand for a good and its supply, whether they are both the same or different, with the “value” or “worth” of the good where the latter are just and only a determinant or factor of its price but seldom determine its price.

As a result, we get the best minds in economics coming out with newsworthy but discouraging statements such as “Canada housing market overvalued by 10 percent” (The Canadian Press, February 4, 2014) when what they mean, and all that they can say, is that “the demand for housing exceeds its supply at the current prices” and, therefore, that it is “undervalued” even at these prices. And the same might be said for the Canadian dollar which at US$0.90 is trading at a discount to its most recent previous value at par; the Canadian dollar is not “undervalued” but it is “overvalued” because the supply of the Canadian dollar at these prices exceeds the demand for it.

And if houses are deemed to be “overvalued” then Canadians could stop buying them at these prices and the prices will come down either because there is an increase in the supply of alternatives at a better price, or the current owners of these houses have a liquidity problem. And similarly for the Canadian dollar; the demand for it needs to be increased which can be done by increasing exports of Canadian products, by decreasing imports, or raising the interest rate. For example, if Americans start buying Canadian houses, we will soon find that both these houses and the Canadian dollar are “undervalued” because the demand for each exceeds the supply at the current prices.

Moreover, it is because we make that distinction and not the “value judgement” based on some fictitious “worth”, and are able to do it with the “price of risk” and the Perpetual Bond™, that our equity portfolios in every market and every segment of every market will always outperform (absent gambling) the “volatility”- and “value”-based models of worth and ownership that pervades the industry.

Mine?

For example, most investors think that because they own a share of a company’s stock that they also own a share of its net worth or shareholders equity and its earnings and property and that these latter will determine its price. But that is not the case.

And the distinction between “demand & supply” versus “value” or “worth” as a determinant of “demand” for stocks, bonds or currency is particularly important right now because investors, globally and in general, can’t decide what price to pay based on what they know (CNBC, February 4, 2014, ‘Hot money’ ride could be getting put on ice).

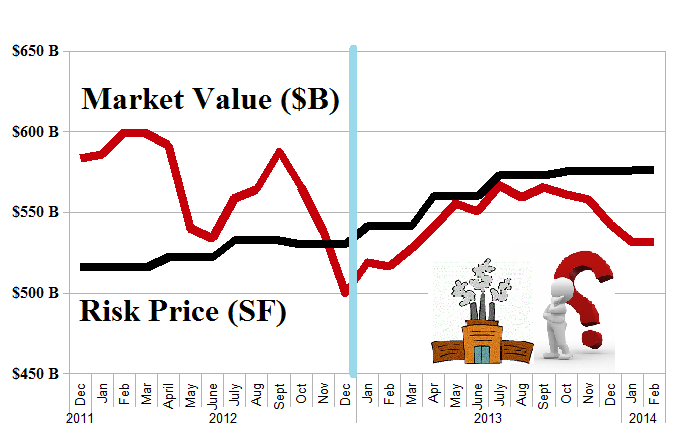

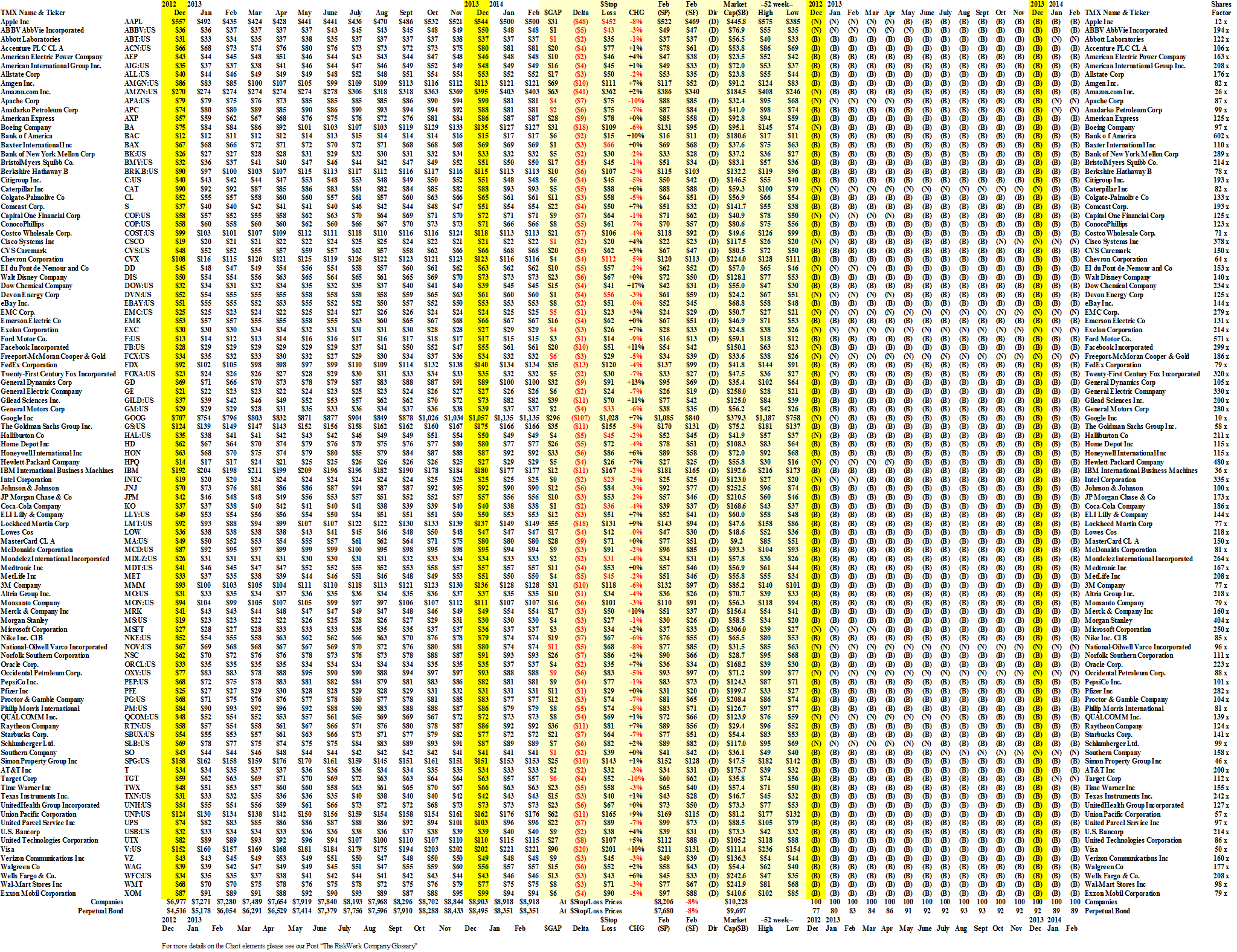

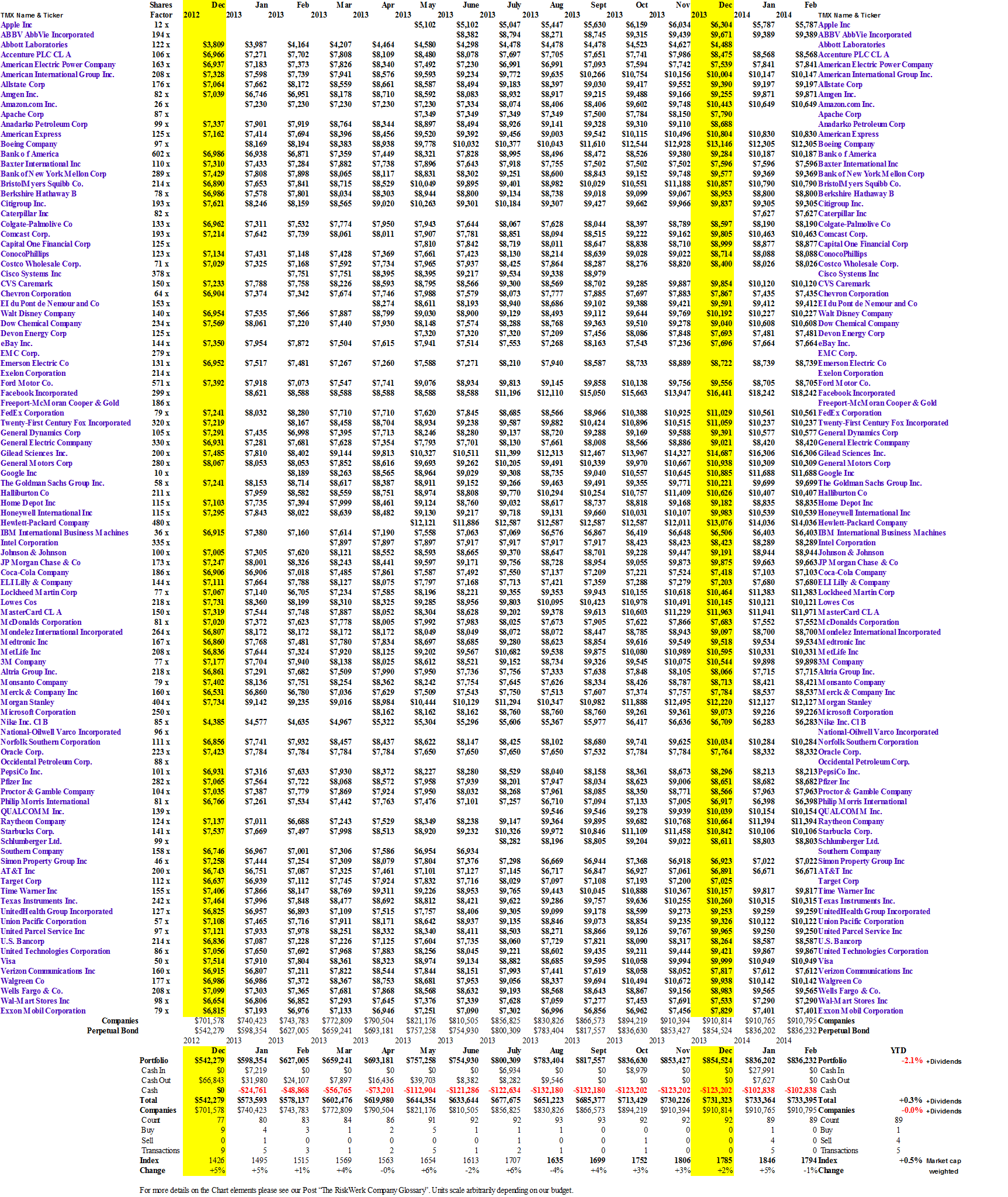

But for us, there is no uncertainty. We’re fully invested in stocks for which the demonstrated demand exceeds the supply and which are, therefore, “undervalued” regardless of the “price” or “worth”, and fully divested of stocks for which the supply exceeds the demand and which are, therefore, “overvalued” (even at these low, low, prices, regardless of the “value”). Please see Exhibit 1 below.

Exhibit 1: The S&P 100 “Undervalued” and “Overvalued” Stocks – February 2014

The S&P 100 Undervalued Stocks – February 2014

The S&P 100 Overvalued Stocks – February 2014

Of the one hundred stocks in the S&P 100, eighty-nine are currently in the Perpetual Bond™ and that portfolio (which is a managed portfolio) returned +35% last year, plus dividends.

The contra-portfolio which consists of all those stocks that failed to trade above the price of risk, did a lot less; it was up as much as +10% but lost $12 billion last month and the eleven stocks in it are still “overvalued” and will remain so until they begin to trade at or above the price of risk.

For more details, please click on the links “(B)(N) NYSE S&P 100 – Prices & Portfolio – February 2014” and “S&P 100 – Portfolio & Cash Flow Summary“.

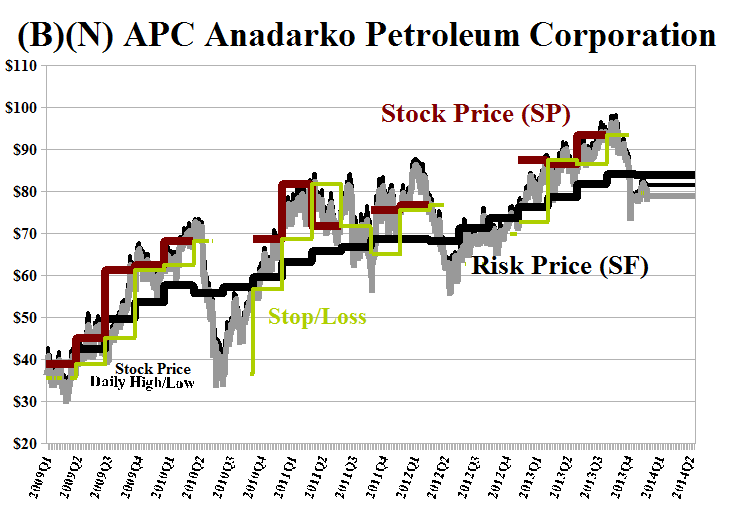

(B)(N) APC Anadarko Petroleum Corporation

As an example, Anadarko Petroleum Corporation is a $40 billion company that earned $1.7 billion and paid $362 million in dividends last year and has been in the Perpetual Bond™ since $74 in December 2012, but was drummed out at $88 in December and is now trading at $80 and is below the price of risk, Risk Price (SP), which is $84 and rising.

Undoubtedly, Anadarko is “worth” more than $40 billion and $80 per share and, in fact, it’s “worth” $84 per share, the price of risk on a “cash as money” basis.

But that information is useless to us until somebody, and then anybody who wants to own it, is willing to pay that price.

For more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}