(B)(N) The “Undervalued” Equity Markets

The Intelligent Investor

Drama. There hasn’t been any “new thinking” in equity market analysis in sixty years, not since Benjamin Graham and David Dodd codified “ownership thinking” in The Intelligent Investor (1949) and the earlier, Security Analysis (1934).

As a result, we have “Bubble-Mania Angst” and “bears” in the “bull market” trying to make sense of “valuations” that don’t make sense to them and which are irrelevant anyway and we have trigger-happy guys wondering about whether this is the right time for 60/40 or 40/60?

Efficient Frontier (B)(N) Boundary Open

And we haven’t forgotten about the Capital Assets Pricing Model (CAPM) and Modern Portfolio Theory (MPT). What we have there is a “line in the sand” that doesn’t exist in any market that we know of. If it did, we’d all be rich.

Nor have we forgotten about the Black & Scholes Option Pricing Model. Interesting!

So, what’s a girl to do? Well, we need to do some “new thinking” and not so much “worrying“. Try this.

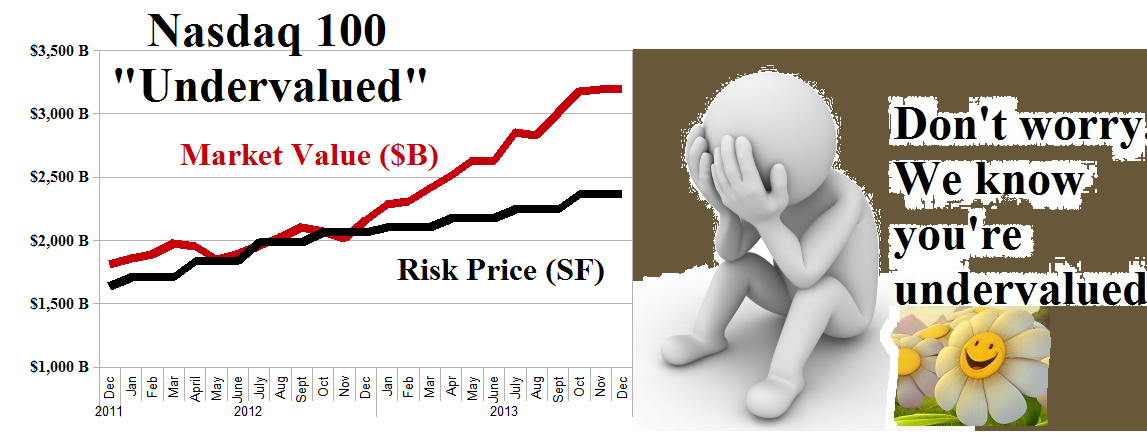

The Nasdaq 100 Undervalued

“A stock is undervalued only if there is an excess of demand over supply”.

“A stock is undervalued only if there is an excess of demand over supply”.

That’s pretty obvious. After all, who is going to buy it from us at this price or a higher price if there’s plenty of it around at a lower price?

And the chart on the right seems to suggest that “undervalued” stocks are likely to get higher prices.

The Nasdaq 100 “Overvalued”

“A stock is overvalued only if there is an excess of supply over demand.”

Are you suggesting then that a stock is overvalued only if there is an excess of supply over demand?

Yes.

But before we get too happy about that, these are “necessary conditions” but not “sufficient”.

For example, there might not be enough money around to buy the undervalued stocks today or investor interests are elsewhere for the time being.

Or, there are companies that are only too happy to print as much stock as we like for whatever reasons we like it.

It’s for those two reasons that from an investor point of view – we want our money to be safe – 100% capital safety – and to obtain a hopeful but not necessarily guaranteed return above the rate of inflation – that there is “a least stock price at which the company is likeable” (Goetze 2006) and that price is the “price of risk“.

Exhibit 1: What the undervalued equity markets have done for us this year in the Perpetual Bond™

Aggregate Market Returns – November 2013

For more information and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.