(P&I) What’s A Girl To Do?

60/40 or 40/60?

Are we too late?

Drama. “History” is a fraud if used as a guide to future investment returns in “managed money” and the “numbers” 5-year or 10-year performance and so forth, are pretty much anything that they want to tell us (Morningstar, November 19, 2013, Fool’s Gold and May 15, 2013, Extreme Outcomes).

We’ve had to confront that issue – and do “history” again – because pension fund managers are once again in their 60/40- or 40/60-modality. Shall we have 60% equities and 40% bonds or the reverse, as has been the case, and how much of our capital should we allocate to “alternatives“?

In any case, they’re late, again, and the uptake in this current “bull market” that began in 2009 ballooned to +30% this year and how long can that last?

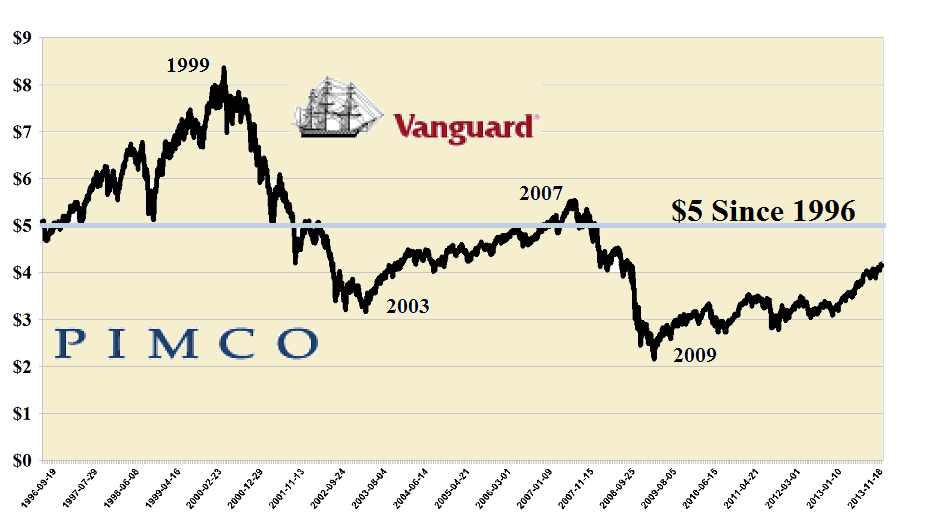

Nevertheless, the flagship bond fund and largest mutual fund in the world, PTTRX PIMCO Total Return Institutional, which manages $250 billion in assets, all in “bonds” of various sorts, has lost money this year and after redemptions has lost ground to the managed equity total return fund, VTSMX Vanguard Total Stock Market Index Investor, which now has over $280 billion to manage.

It will surprise the hirsute “risk/reward” acolytes that both funds have tripled investor capital (about 3×) since inception in 1996 but that PTTRX has outperformed VTSMX by about 20% during all of that time. But we’re not that much further ahead because what used to cost $1 in 1996 now costs $1.50 (US Bureau of Labor Statistics). Please see Exhibit 1 below.

Exhibit 1: Vanguard VTSMX in units of PIMCO PTTRX since 1996

The chart shows that $5 PIMCO invested in VTSMX in 1996 is now $4 PIMCO in 2013 and although both funds tripled our money (which the chart doesn’t show), what was $1 in 1996 is now $3 in cash that buys only $2 in the goods and services that we could have bought in 1996 and still need.

The real return is then about +4% per year but “investors” are unlikely to stay the course. For one reason or another, liquidity being one of them, anxiety another, most investors tend to get on board late (buying closer to the top) and jump ship late (selling closer to the bottom) and we wonder whether VTSMX will once again be $5 PIMCO in the near future and whether that too will be a “top” (ibid, Morningstar).

If bond holders are now making the 60/40-decision, then they’re going to be selling 33% of their bond positions (60% to 40%) and increasing their equity positions by 50% (40% to 60%). But the “bond market” is about twice as large as the “equity market” (about $40 trillion in bonds to $26 trillion in equities) which means that about $15 trillion is going to be looking for things to buy from us because we are never out of the equities market and never in the bond market. Please see Exhibit 2 below.

Exhibit 2: The US Equity Markets – November 2013

Aggregate Market Returns – November 2013

The Nasdaq 100 “Overvalued”

Moreover, everything that we have trades in (B) and is, therefore, “undervalued” but only available at “high prices” so we should expect that a lot of that bond money is going to be buying “bargains” in the “Trading Zone” (N) either directly or through participation in an index fund of some sort.

Oops!

But, the story isn’t over. Eventually, investors will begin to wonder why they are holding these stocks with [P/E] multiples in the stratosphere created with their own money and decide to sell and buy bonds. OK.

For more information and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.