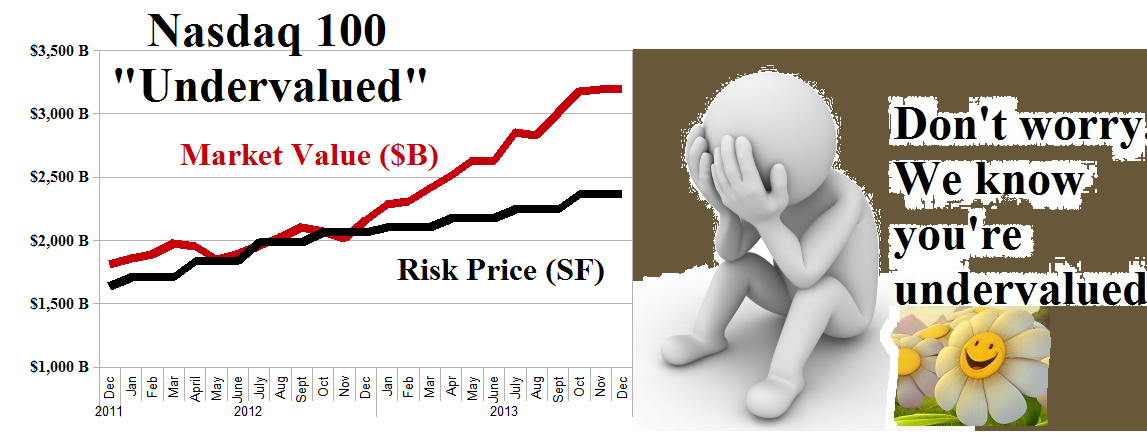

(B)(N) The NASDAQ 100 “Undervalued”

Deal Book. Mr. Icahn has taken a position in Hologic Incorporated of more than 12% and about $750 million in the company currently valued at $6 billion (Reuters, November 21, 2013, Hologic adopts poison pill after Icahn reports stake).

Don’t worry. We can help.

In his view, the company is “undervalued” and the response of the company – which is defensive – is quite at odds with the response of the market which immediately lifted the stock price by a few percent.

Whether that holds or not, will of course depend on what the company and its current shareholders do next (ibid, Reuters).

The company has never paid a dividend and has lost money in four of the last five years amounting to about $3.5 billion despite increasing sales and the year ending in September was gigantic with a loss of $1.2 billion on sales of $2.5 billion.

We think that the company is “undervalued” too but that has nothing to do with the earnings or lack of dividends or other problems that the management will likely be able to deal with. We think that it’s undervalued because it’s trading as a (B), that is the ambient stock price appears to be at or above the “price of risk“. Please see Exhibit 1 below.

Exhibit 1: (B)(N) HOLX Hologic Incorporated – Risk Price Chart

(B)(N) HOLX Hologic Incorporated

Hologic Incorporated is a developer, manufacturer and supplier of medical imaging systems and diagnostic and surgical products focused on the healthcare needs of women.

(Please Click on the Chart to make it larger if required.)

Obviously, with reference to Exhibit 1, the stock has been a “high maintenance” stock and returns have been difficult to get and keep.

We only buy or hold the stock if the ambient stock price summarized as the Stock Price (SP) (Red line and a step function) appears to be at or above the price of risk which we estimate as the Risk Price (SF) which is also a step-function and is calculated from generally available quarterly balance sheets (but has nothing to do with earnings, per se).

And we always protect whatever prices we’re able to get against volatility or “surprise” by using an effective stop/loss or bought put and we’re committed to buying and holding anything that’s trading above the price of risk, depending only our budget; and if we sell a stock, it’s because we’ve been stopped out and the stock is subsequently trading below the price of risk (in which case we might “put” the stock at the higher price if we have a put in effect).

On the other hand, if the stock is still trading above the price of risk, then we have the option of selling the in-the-money put and buying more of the stock at a lower price.

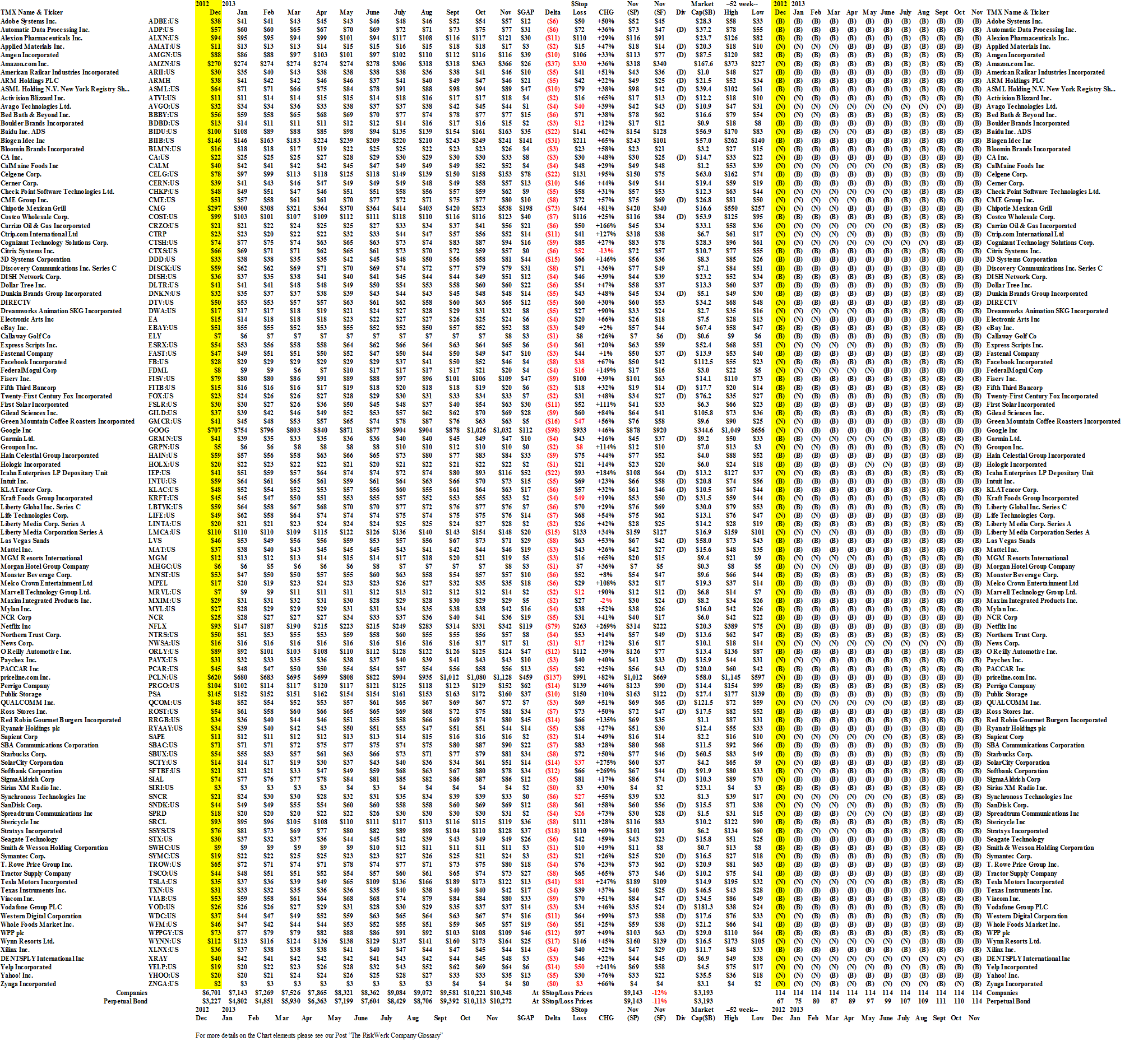

But, there’s a lot more that’s “undervalued” in the NASDAQ 100+ right now despite the fact that “stock prices” are up an average of about 50% this year. Please Click on the link NASDAQ 100 “Undervalued” – Prices & Portfolio – November 2013 for those “undervalued” companies that we’re carrying into 2014.

The Nasdaq 100 Undervalued

And in general, it’s good to be “undervalued”.

Although the NASDAQ 100 Index is up +27% this year, the cash only Perpetual Bond™ is up +60% to date and has 114 companies in it. And the leveraged Perpetual Bond™ which uses the margin account as appropriate is up over +220% and is still active.

The Nasdaq 100 “Overvalued”

Nor is this an “accident”.

The companies that didn’t make the “cut” – and there are about thirty of them that we know of – did this (on the left) for the last two years.

For more information and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}