(B)(N) The Canadian “Hot” Money Stocks

Canada With 3rd World “Growth”

Drama. Canada doesn’t think of itself as a “3rd world” nation or emerging economy but the reality of it is quite different and “bracing”. For example, last year, the top sixty Canadian companies in the S&P TSX earned $52 billion and paid 75% of it, $40 billion, in dividends and most of that, perhaps as much as 80% of it, is going to be paid, and most likely “exported”, to the foreign owners of Canadian stocks. Please see Exhibit 1 below.

That in itself is not a cause for grief or alarm. No country that is not in the “3rd world” and destined to stay there, is an island onto itself and every industrialized country needs to trade in order to remain industrialized. To reverse that “fact” and symptom of de-industrialization and “underemployment” in Canada, however, Canadians need to own more of their own industries and resources, and export more of their industrial, service and resource products and less of their capital. In other words, we need to buy it back but not be unfriendly to foreign investment interests (CNBC, February 4, 2014, ‘Hot money’ ride could be getting put on ice).

And the solution, as in all investments, is “liquidity”. Please see below.

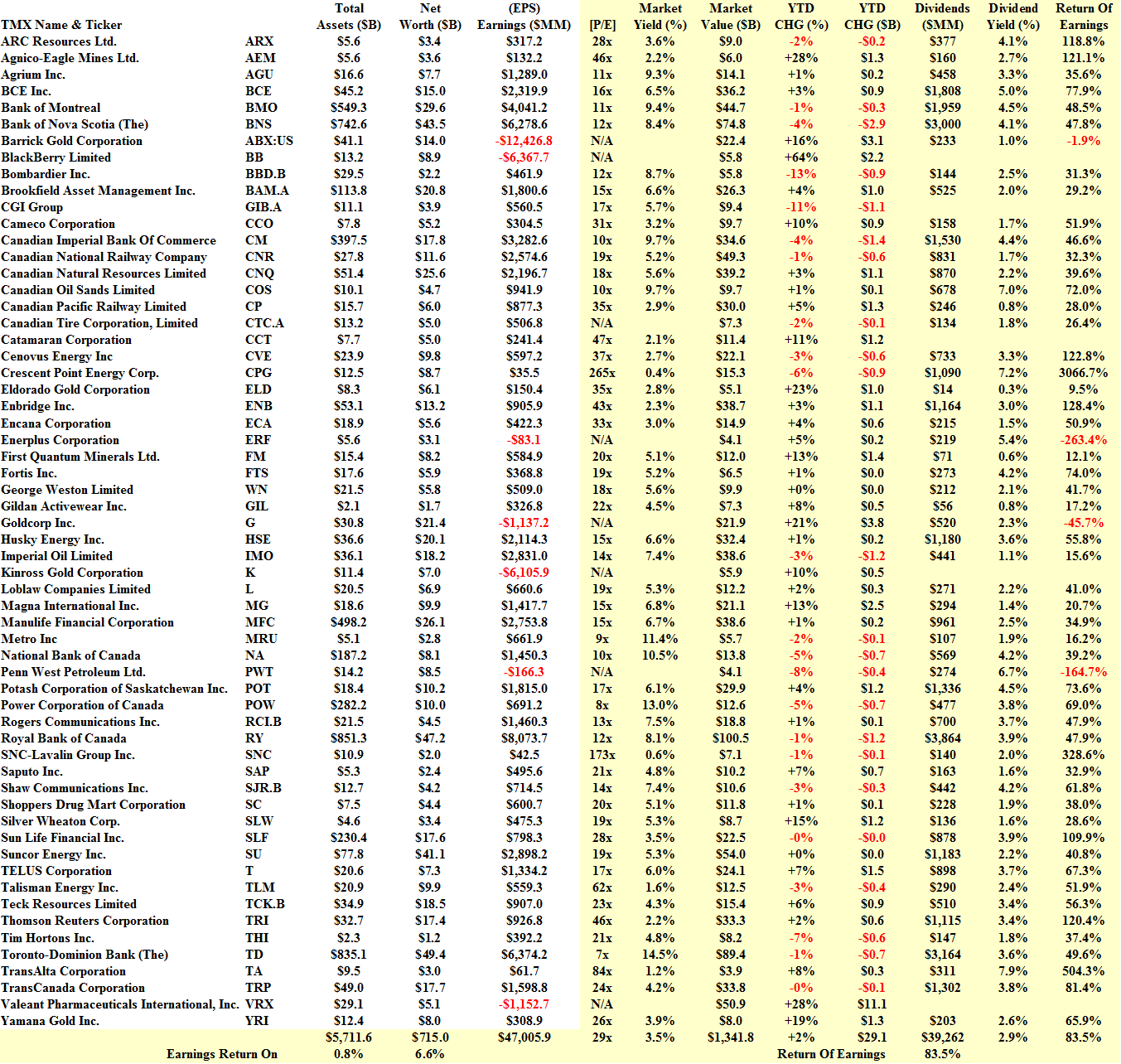

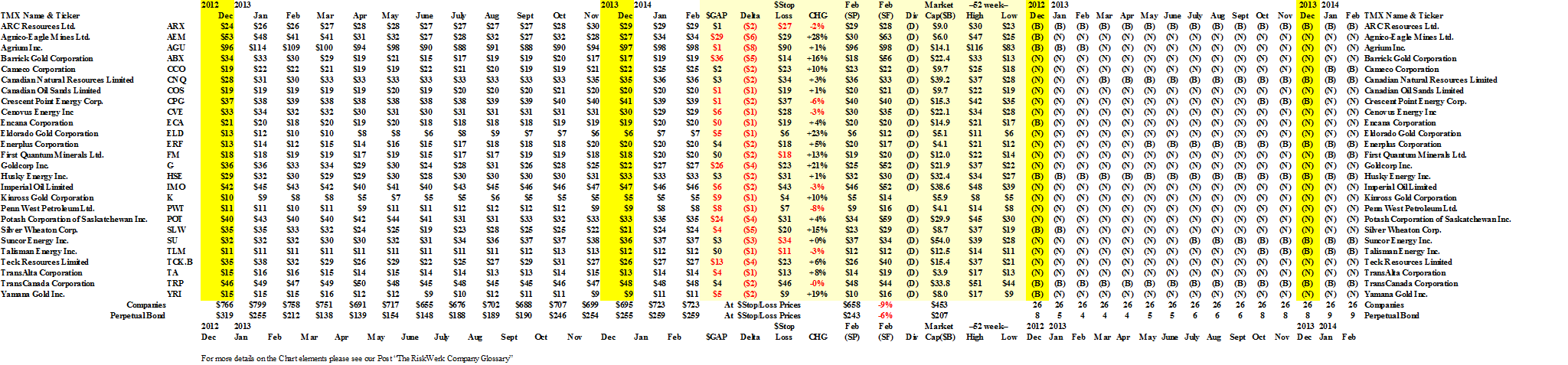

Exhibit 1: The Canadian “Hot” Money Stocks – Fundamentals – February 2014

The Canadian “Hot” Money Stocks – Fundamentals – February 2014

The Overvalued Undervalued Canadian “Hot” Money Stocks

The table shows that in aggregate these companies returned 6.6% on the shareholders equity and less than 1% on the total assets.

Moreover, the debt burden is extraordinary at $5 trillion ($5.7 trillion less $715 billion) and 7× the shareholders equity for which we also paid $40 billion last year in shareholder dividends.

But it is laughable to think that the shareholders actually own these companies when the entire market value is $1.3 trillion and the debt is $5 trillion and 4× as much. The debt and bondholders are happy to keep their money in these companies but the shareholders aren’t.

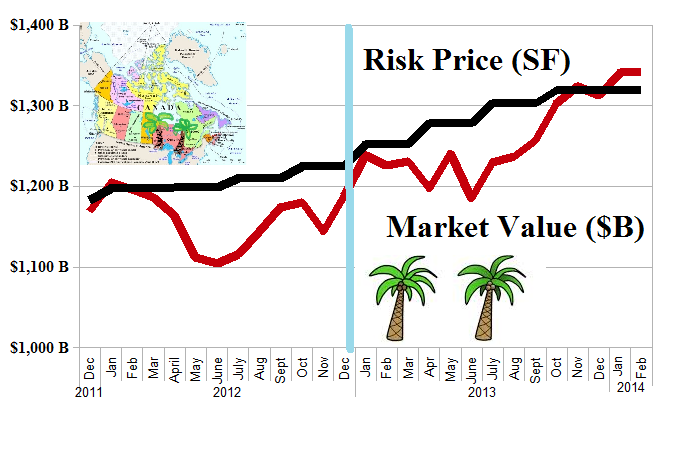

Moreover, with reference to the chart above which shows the market value and the value of the same companies at the “price of risk” (Risk Price (SF)), these companies have been “overvalued” for the last three years and it is only since December that in aggregate, the market value has exceeded the “price of risk” which is the least amount of money that we should be willing to pay for these companies as investments – we want our money to be safe – 100% capital safety – and to obtain a hopeful but not necessarily guaranteed return above the rate of inflation.

The debt-holders and bondholders are obviously satisfied that they’re doing that and that there is no need to change the equation absent a need for “liquidity” or the emergence of higher rates of interest. The shareholders, on the other hand, are not that happy or certain.

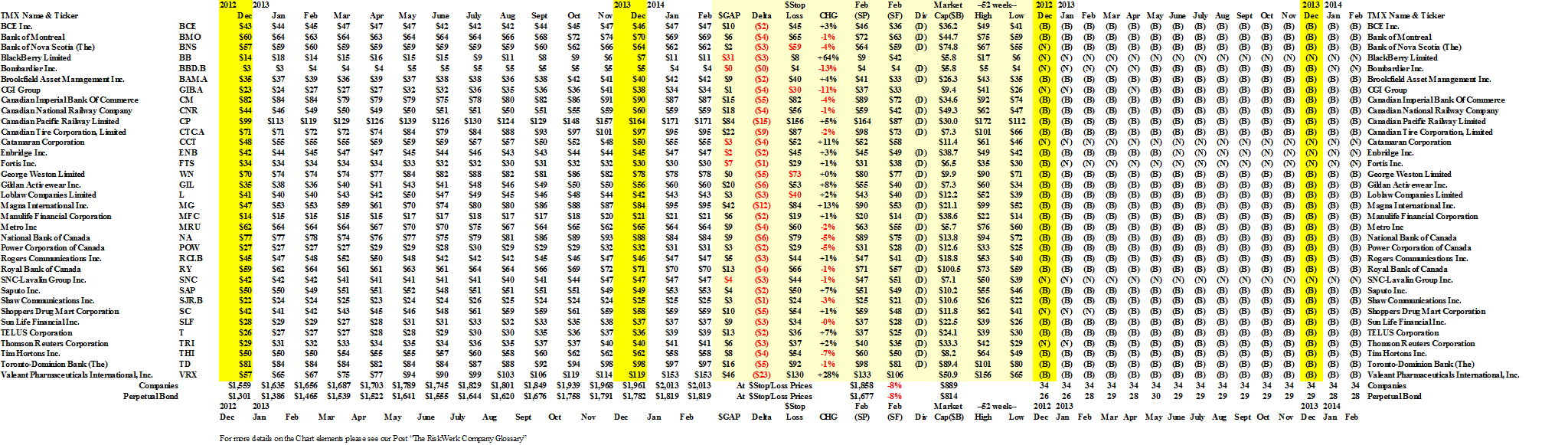

However, the market for Canadian stocks segments naturally into a market for the non-resource or industrial stocks which includes the banks, insurance companies, industrials and assorted consumer-oriented companies, and the resource stocks within which we have included the pipelines. Please see the tables in Exhibit 2 below.

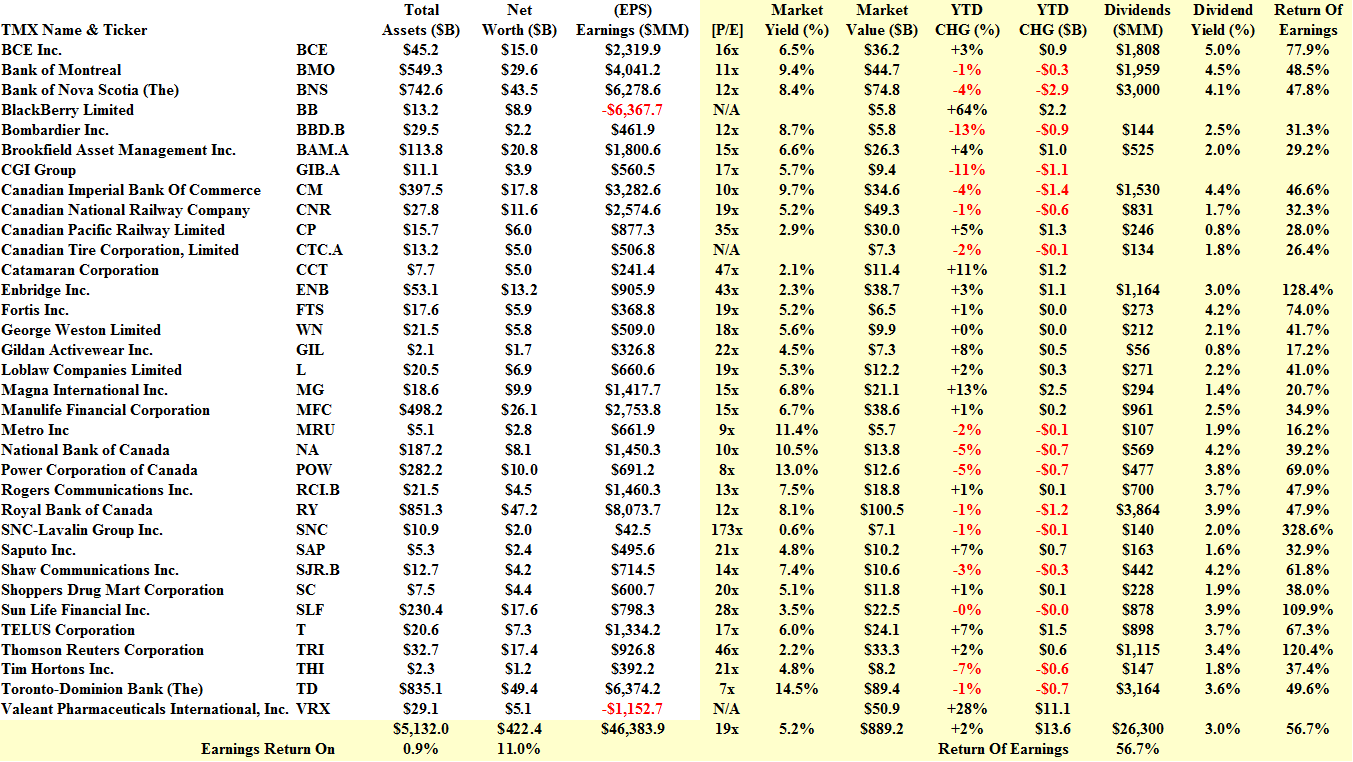

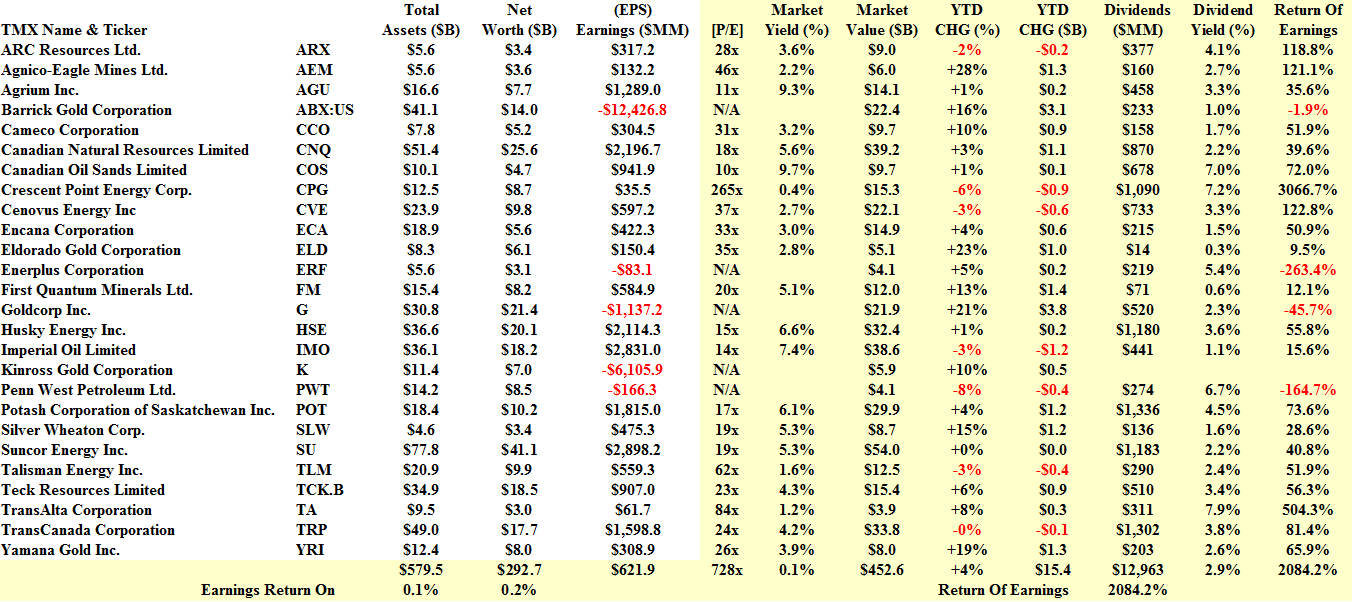

Exhibit 2: Industrial and Resource Canadian “Hot” Money Stocks – Fundamentals – February 2014

The Industrial Canadian “Hot” Money Stocks – Fundamentals – February 2014

The Resource Canadian “Hot” Money Stocks – Fundamentals – February 2014

Resource and Non-Resource Canadian “Hot” Money Stocks

From these two tables, we see that most of the debt, $4.6 trillion, is held by the industrials ($5.1 trillion less $422 billion) and from the chart on the left, that these companies have been “undervalued” and trading at or above the price of risk at “high” prices for the last several years and are undervalued now despite a stock market gain of +2% and $13.6 billion since December.

On the other hand, the resource companies match the debt with shareholders equity ($579 billion less $292 billion) and these companies are still “overvalued” and there is no certainty in investor regard for them although they are up +4% and $15 billion since December. We just don’t know if they’re going stay “up” and our estimate of the downside in the aggregate market value due to the demonstrated volatility is minus (9%) absent surprise. And they paid 20× their earnings as dividends.

However, because they are “overvalued” and there is an excess of supply over demand, large blocks of these stocks cannot be traded without affecting the price. The ambitious seller of a large block, most likely for “liquidity” reasons, can expect to receive a lower bid, below the market price; and the buyer of a large block can expect to get it at the market price, or somewhat lower, or somewhat higher depending on the negotiated asking price; and if the price is not right, we can expect that they will walk away because there are lots of other opportunities in this sector.

Illiquid But They Will Hatch.

They’re Canadian Aren’t They.

In other words, these stocks are “illiquid” and behave like long-dated “bonds” (which also have an indeterminate return even if held to maturity) in contrast to the stocks that are trading at or above the price of risk, and we can expect to buy them at par from a grateful seller. They are, therefore, good investments for patient money, money for which liquidity is not a problem and for which a long investment horizon is satisfactory.

For example, the current entire market value of the resource companies, including the pipelines, is $450 billion and patient money can buy a substantial or controlling interest in all of them for less than $200 billion and there are lots of patient, long-horizon investors in the Canadian pension plans who don’t need to chase our money in Brazil, Argentina, Turkey and elsewhere in the years to come (CBC, January 31, 2014, Head of CPP fund investing ‘where the puck is going to be’).

Here’s the puck.

Courtesy: Winnipeg Jets

They can chase it right here, repatriate the dividends, and do some good for Canadians, now. The puck is in the net, don’t you know?

For more information on what’s hot and what’s not in the Canadian Resource and Industrial “Hot” Money Stocks, please click on the links and again to make them larger if required.

And for more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}