(B)(N) NXY The Nexen Best Thing

Deal Book. There’s a perception that CNOOC, the China National Offshore Oil Corporation, “paid too much” to acquire Nexen Incorporated early this year (Reuters, October 6 2013, Special Report: The education of China’s oil company).

Nexen Building in Calgary, Alberta

We don’t think that’s true because making the deal was difficult (and ground-breaking) and required a significant premium at that time to win the support of the Nexen shareholders, and in the long term these assets can reasonably be expected to provide significant production benefits to CNOOC and will contribute significantly to the further development of heavy oil development and production in China which is said to have the world’s largest reserves of oil-sands and shale-oil that are waiting for capital and technological advances for further development.

But what is “significant”? What is the “numeraire”, in other words?

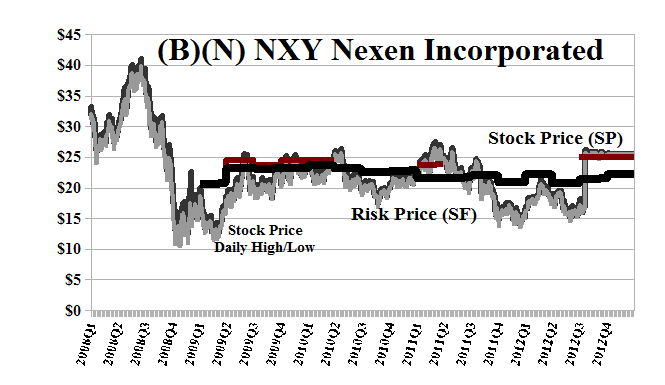

The “context” is significant because at that time the deal was described as a “no brainer” for Nexen shareholders because they would be receiving a 60% premium at $27.50 per share over the ambient stock prices of $20 or significantly less and uncertain in the year previous. Please see Exhibit 1 below.

On the other hand, the deal was also politically charged in more than one way and the words “lipstick on a pig” were used to describe the process (but not the deal) (Maclean’s, November 1, 2012, If Ottawa says no to China on Nexen deal there’ll be a price to pay: experts).

Nevertheless, it’s worthwhile to sharpen our pencil and to look at the deal in money terms that monetize “the demonstrated societal norm of risk aversion and bargaining practice”, notwithstanding the extraordinary and special (individual) projections of “deal making”.

The Nexen Deal

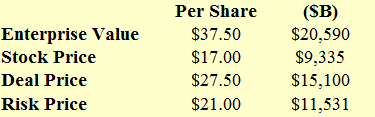

The “enterprise value” is commonly cited and it is the total debt ($11.3 billion) plus the market value ($9.3 billion) in this case, and works out to $37.50 per share which is a significant premium to both the stock price ($17) and the deal price ($27.50).

It’s also significantly above the price of risk ($21) and suggests that somebody should be significantly “happy”. In fact, much too happy and suggests “rip-off” (oversold) or that the buyer knows something that nobody else knows but has overplayed their hand.

Buyer OK Happy Seller OK Happy

In hindsight, and not in the heat of deal-making, analysts now concede that the “risk price” is the “correct price” in view of the actual difficulties of producing, selling, and transporting “heavy oil” (ibid, Reuters).

But that price (the risk price) is further freighted with the extraordinary burden of the political and policy content of that time which even now is not fully worked out and has such consequences as “further deals are not on the table” at the present time.

The Nash Diagram on the right suggests that the seller demands a higher price but might accept a lower, but not too low; and that the buyer will accept a higher price but not too high and, of course, prefers a lower price but would not be interested if the price were too low (suggesting “shoddy goods”).

All of this is quite ordinary and we do it every day whenever we’re shopping for almost any consumer product. And so it is with the “price of risk” because an investment is just and only the purchase of risk.

Exhibit 1: (B)(N) NXY Nexen Incorporated – Risk Price Chart – September 2012

(B)(N) NXY Nexen Incorporated

Nexen Incorporated is an independent energy company worldwide. The company’s Conventional Oil and Gas segment explores for, develops, and produces crude oil and natural gas from conventional sources and operates in the United Kingdom, Canada and the United States, as well as offshore West Africa, Colombia, and Yemen. Nexen’s Oil Sands segment develops and produces synthetic crude oil from the Athabasca oil sands in northern Alberta and its Shale Gas segment explores for and produces unconventional gas from shale formations in northeastern British Columbia. Nexen Incorporated was founded in 1971, has 3,000 employees, and is headquartered in Calgary, Canada.

(Please Click on the Chart to make it larger if required.)

For more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.