(B)(N) Black Gold In The Canadian Oil Patch

Drama. The Canadian oil patch has been in the doldrums this year, as have most of the resource-based or commodities industries such as gold, silver, copper, uranium, iron ore, forestry, or potash. The industry consists of about forty-three companies that are directly engaged in exploration, development or production, and the pipelines, and will pay about $11 billion in dividends this year and employ more than 500,000 Canadians.

The Canadian Oil Patch – Statistics

Courtesy: Canadian Association of Petroleum Producers

It’s said, however, that the industry is already 80% owned by foreign interests – and has been for decades – and by world money standards it’s small even though it is one of the top ten producers of energy, natural gas and conventional crude oil, notwithstanding the reserves which are among the largest in the world. Please see the statistics.

Nevertheless, the entire industry has a current market value of only $370 billion which is less than one Exxon Mobil ($380 billion) which will also pay about $11 billion in dividends this year. And similarly, Apple Incorporated, the maker of i-things for everybody, has a market value of $440 billion and will also pay $11 billion in dividends this year.

However, market value has little to do with capitalization which is the debt and shareholders equity – real money on the balance sheet – and the “market value” of the companies is of little use to them if they can’t access it by, for example, rights offerings, warrants, or secondary offerings in the capital markets without further depressing the price.

The market value might as well be zero if nobody wants to buy the stock from us, but usually perks up if somebody wants to buy all of the stock.

But there seems to be not much interest in buying more nor much interest in investing more in the industry which is looking for new investment (not “market value”) of about $650 billion over the next ten years (Energy Minister, Mr. Oliver, quoted in Reuters, October 7, 2012).

And we cannot make an investment case on the basis of a compelling or exclusive “national interest” (The Street, October 3, 2013, Jim Cramer: What About Oil From Canada?) because nationalist and mercantile policies are the death-knell of modern world economies and what’s expected of them.

New Canadian Money

So, where’s the new money going to come from? Should we print it?

The answer is “yes, it will be printed” because, obviously, there’s a lot more money in circulation now than there was ten years ago.

On the other hand, the answer is “no, because even though it will be printed, it should be printed only as it’s earned” which is to say that the new money that’s being printed should have at least as much “purchasing power” as the old money that it replaces even though “prices” might be higher and we need more of it.

Canadian Wheat & the CPR

Well, unlike the Canadian public pension plans which have about $1 trillion among them – and still think that they need more for the future and have no money to spare for us, their shareholders, to lighten our burden now – and which will be receiving meagre returns this year on far-flung investment strategies without much distinction, the all-Canadian Perpetual Bond™ in the S&P TSX is up +96% this year, plus dividends, which is +20% more than what we had in early August in the S&P TSX “Hangdog” Market.

S&P TSX “Hangdog” Market

And we need to deal with that now and not some time in the far-flung future in which our money will, undoubtedly, not be worth anything.

The portfolio currently has 109 companies in it – and over two hundred that are not – including 10 of the oils, and it would seem to be merely prudent to think about taking some of those profits off the table and to re-allocate them to oil & gas companies.

But we can’t buy them just because they’re “cheap”. They need to demonstrate that they are alive and for that they need to be a (B) of which there are currently ten but more might emerge if we demonstrate an interest in the sector with our money for their new projects.

And although we can reasonably expect double-digit returns next year, regardless of the market, it likely won’t be in the same crop of companies that we harvest.

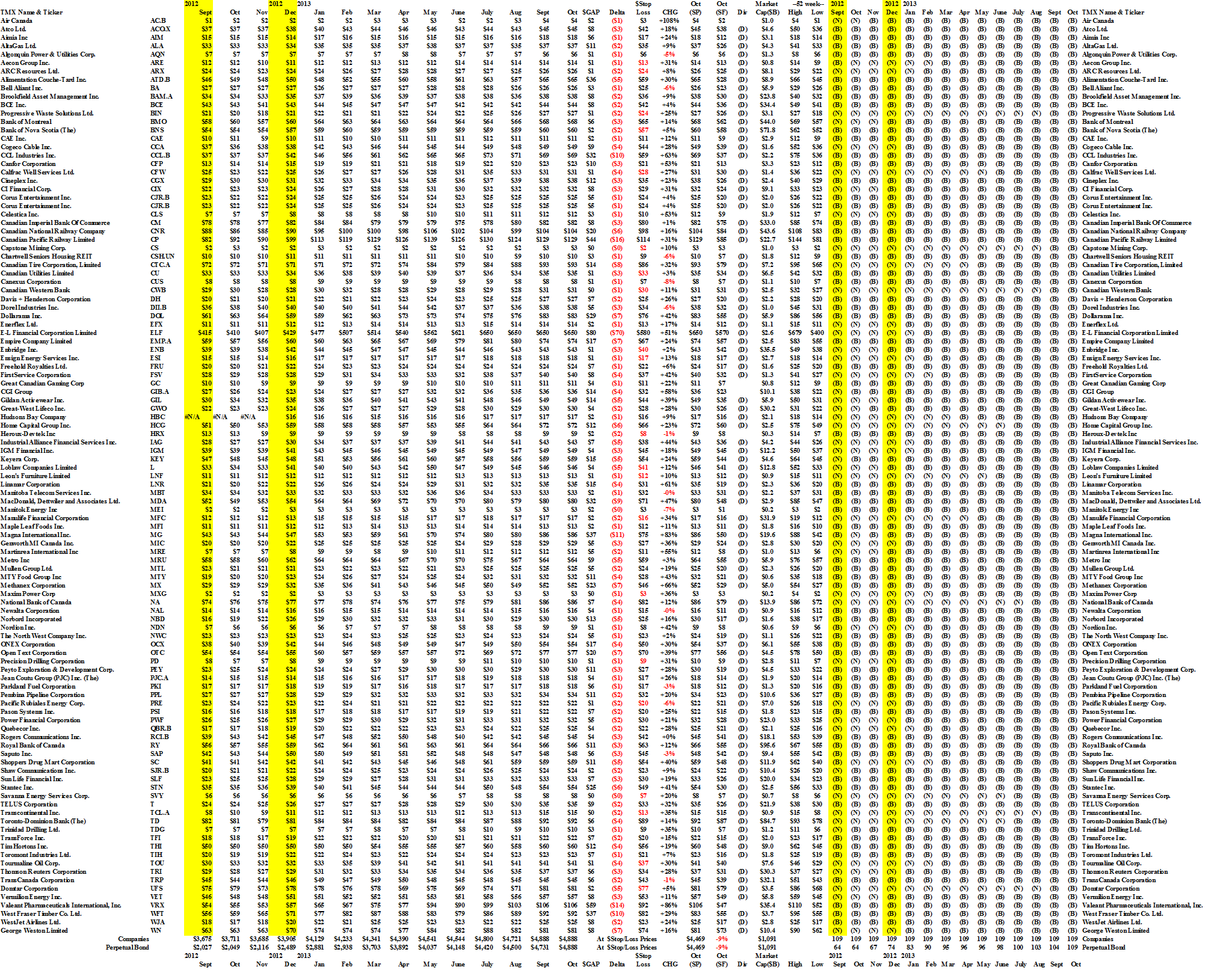

Exhibit 1: (B)(N) S&P TSX “Hangdog” Market – Cash Flow Summary – October 2013

S&P TSX “Hangdog” Market – Cash Flow – October 2013

(Please Click on the Chart to make it larger and Portfolio twice for the details.)

At the present time, Canada seems to be exporting all of its conventional oil production (about 1.3 million barrels a day) and about half of its heavy oil and synthetic oil production (about 900,000 barrels a day) and importing about 800,000 barrels a day of conventional oil and using about 900,000 barrels a day of the heavy oils and synthetics for its own consumption, an equation that will surely change as conventional oil production diminishes. (Please see the statistics.)

Our usual rule applied to the oils – we only buy and hold a stock if it’s trading as a (B), that is, the ambient stock price appears to be above the price of risk – created a portfolio of eight to ten of the oils, which hasn’t changed much since December, with a return of +40% so far this year. Please see Exhibit 2 below.

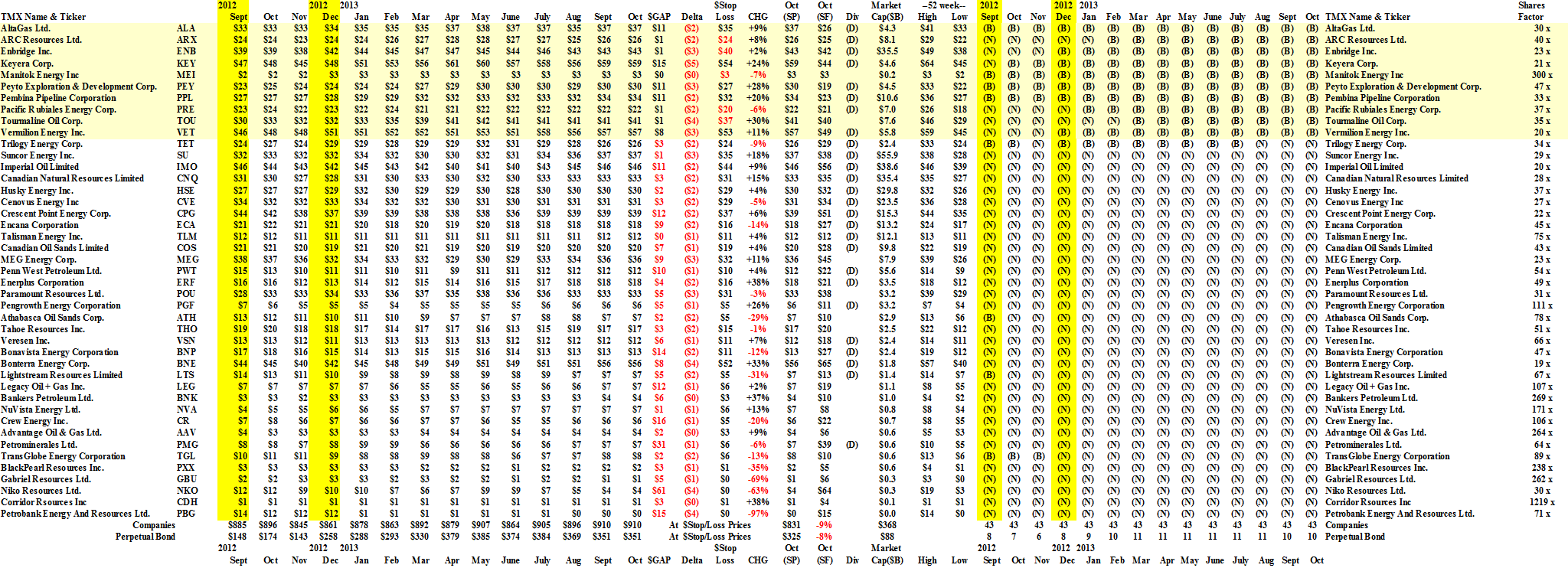

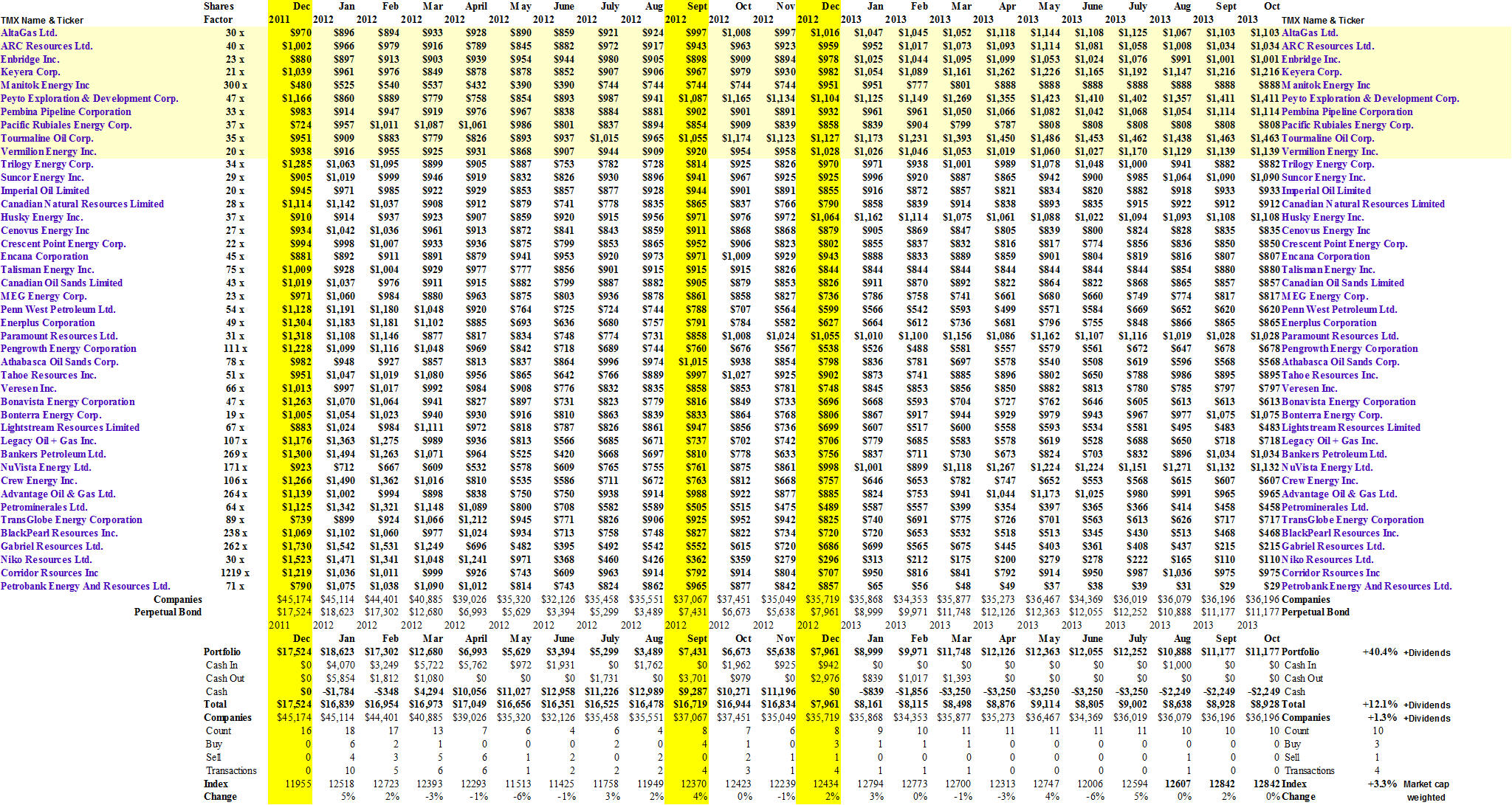

Exhibit 2: (B)(N) Black Gold in The Canadian Oil Patch – Cash Flow Summary – October 2013

Black Gold in the Canadian Oil Patch – Cash Flow Summary – October 2013

(Please Click on the Chart to make it larger if required.)

Because the portfolio was small (only eight companies in December) and the stock price differences were large, we bought the companies on the basis of a more or less equal amount of money into each, based on the average prices in the nine months preceding December.

For more details, please click on the links for Prices and Portfolio.

Clearly, if we keep on doing this – and there’s no reason that we shouldn’t – we’ll need to buy a toll road, too, just to cart away our money and avoid the traffic.

+96% – Toll Road – +40%

For more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}

{kind=link}