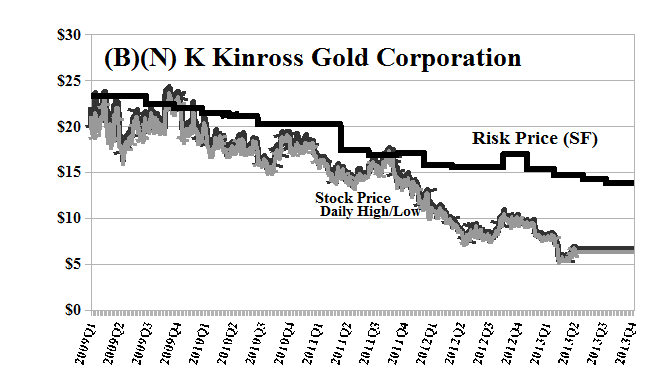

(B)(N) K Kinross Gold Corporation

Drama. Kinross Gold Corporation has left the valley and $1 billion behind in a 2-year old dispute with the Ecuadorean government over who owns what, and how it’s to be taxed, and how it’s to be developed (The Wall Street Journal, June 11, 2013, Kinross to Exit Ecuador as Gold-Mine Talks Fail).

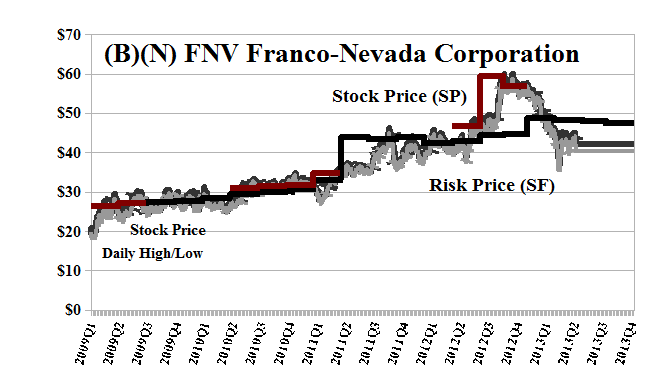

None of the Canadian golds are doing well and the last two that were in the Perpetual Bond™ in March (Yamana Gold and Franco-Nevada Gold) have exited as their stock prices plunged by more than 10% in the last two months (please see Exhibits 1 through 3 below). Moreover, the SPDR Gold Trust (GLD) with a market value of $45 billion has also plunged by more than (10%) since the end of March to the current 133 from 152 (index).

The Fruta del Norte deposit (“FDN”) is located within a 95,000 hectare land package in south-eastern Ecuador known as the Condor project. Kinross acquired 100% of the Condor project on September 30, 2008 through the acquisition of Aurelian Resources Inc

It is said that insiders are buying the gold stocks – but what else can they do? If somebody doesn’t buy them then the prices might go even lower (The Globe & Mail, April 30, 2013, Junior mining stocks see record insider buying).

They could be right – probably, are right, eventually – because it’s also said that there is already a shortage of supply to meet the demand for gold and silver bullion bars and artifacts, for the same reason that the price of gasoline is so high at the pumps. We’re not refining enough.

The Condor River, Ecuador

Even copper is down about (10%) since March but Ecuador has signed a $2 billion investment contract with the Chinese-owned mining company, Ecuacorriente SA, for the open-pit Mirador copper project on the Pacific coast that expects to start production at the end of 2015.

Kinross currently has a market value of $7 billion which is less than a third of what it was in 2009 (please see Exhibit 1 below). The company valiantly continues to pay a dividend of $0.08 per share semi-annually for a payment of $180 million per year to its shareholders and a current yield of more than 2.5%.

With reference to the Charts below, a company is only in the Perpetual Bond™ if the ambient stock prices summarized at the Red Line Stock Price (SP) are above the Black Line Risk Price (SF), and for no other reason. For examples of “price protection” using either a stop/loss based on the demonstrated stock price volatility, or a “collar”, please see almost any of our (B)(N)-Company posts.

Exhibit 1: (B)(N) K Kinross Gold Corporation – Risk Price Chart

(B)(N) K Kinross Gold Corporation

Kinross Gold Corporation is a gold mining company. The Company’s mines and projects are in Brazil, Canada, Chile, Ecuador, Ghana, Mauritania, Russia and the United States.

(Please Click on the Chart to make it larger if required.)

Exhibit 2: (B)(N) YRI Yamana Gold Incorporated – Risk Price Chart

(B)(N) YRI Yamana Gold Incorporated – June 2013

Yamana Gold Incorporated is a Canadian-based gold producer with significant gold production, gold development stage properties, exploration properties, and land positions in Brazil, Argentina, Chile, Mexico and Colombia.

(Please Click on the Chart to make it larger if required.)

Exhibit 3: (B)(N) FNV Franco-Nevada Corporation – Risk Price Chart

(B)(N) FNV Franco-Nevada Corporation – June 2013

Franco-Nevada Corporation is a gold-focused royalty and stream company with additional interests in platinum group metals, oil & gas and other resource assets.

(Please Click on the Chart to make it larger if required.)

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.