(B)(N) CTRX Catamaran Corporation

Deal Book. The “market” is festooned with analysts and pundits who have a “better way” to make money in the stock market. Some of that will work some of the time, like a broken clock, but none of it will work all of the time, and it’s anecdotal that if it worked once, or twice, it becomes a “legend” and the same people will continue to do the same things until it’s all gone.

What time is it?

We mention that because we’re constantly surprised by good news from places in which we were not even looking, and the only way to benefit now is to have been there all the time, because the ingenuity of the thousands of companies in the market doing tens of thousands of different things, is simply out of reach for us; not so much because of the “complexity” of doing it, but because there are so many opportunities that it becomes very difficult to choose which opportunity we should pursue now.

Courtesy: Planetary Resouces

For example, should we buy commodities? They’re all available and begging for buyers and surely, they’ll come back in the long term? But that isn’t true because who knows what’s on any passing asteroid?

Courtesy: Catamaran Corporation

And, case in point, we where already there for Catamaran and we were already there for Cigna, which companies have just struck another of the creative and value-creating symbiots that can only emerge from the ground floor, and seldom from the offices of the analysts and pundits on Wall Street who are merely there to applaud the tailings of what’s already been done (The Associated Press, June 11, 2013, Catamaran stock jumps after PBM (Pharmacy Benefit Manager) reaches new agreement to work with health insurer Cigna).

Courtesy: Cigna Corp

For example, with reference to Exhibits 1 and 2 below, we were sold out of our position in Catamaran on a stop/loss earlier this year (please see Exhibit 1 below) because the stock price came under pressure – and, as it turns out, the emerging deal was uncertain, but we weren’t a party to that information – and the stock price dropped below the price of risk for reasons of which we have no idea. All that we knew was that the stock was trading at or above the price of risk, and then it wasn’t, which to us is a sell signal.

But we’ve owned Catamaran since $5 in 2009 and we were sold out at $54 in March and we stayed sold out because it was trading below the price of risk which was $53 at that time, and which has since increased to the current $59 because of new balance sheet information that became available at the end of March, not because of the stock price which did drop shortly thereafter reflecting investor uncertainty in the future earnings growth of the company of which we had no idea. (Please see Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason.)

Moreover, we’re not buying it now and we won’t be buying it again until the stock price exceeds the price of risk regardless of how positive the deal appears to be for the company. We’ll just have to wait and see how this works out because there are lots of companies – hundreds, in fact – that are trading above the price of risk and we understand exactly what that means.

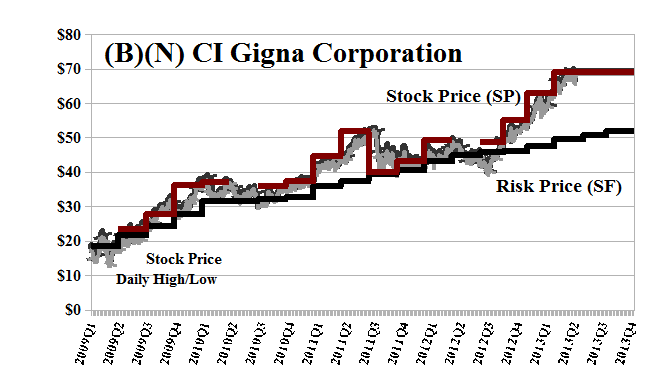

Similarly, we’ve owned Cigna at various times (please see Exhibit 2 below) but most recently since June of 2012 at $48 and we still have it now and for the same reason; Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason.

None of this makes any sense to the analysts and pundits on Wall Street. They don’t know what the price of risk is. They don’t know how to make investments that are “as good as cash” and “better than money” because they don’t know what that means. They don’t know that we invest our money not to have a better chance of losing it, but to have the possibility of a non-negative real rate of return. And that’s all. Anything else is just a gamble.

Exhibit 1: (B)(N) CTRX Catamaran Corporation – Risk Price Chart

(B)(N) CTRX Catamaran Corporation

Catamaran Corp is a provider of pharmacy benefit management services and healthcare IT solutions to the healthcare benefit management industry. The Company’s clients include pharmaceutical supply chain and various others in the same field.

(Please Click on the Chart to make it larger if required.)

From the Company: Catamaran Corporation provides pharmacy benefit management (PBM) services and healthcare information technology (HCIT) solutions to the healthcare benefits management industry in North America. Its PBM services include electronic point-of-sale pharmacy claims management, retail pharmacy network management, mail and specialty pharmacy claims management, Medicare Part D services, benefit design consultation, preferred drug management programs, drug review and analysis, consulting services, data access, and reporting and information analysis. The company offers RxCLAIM, an online transaction processing system to provide online adjudication of third-party prescription drug claims at the point of service, as well as payment and billing support and real-time functionality for updating benefit, price, member, provider, and drug details. It also provides RxBUILDER, a Web-based interface for formulary creation and maintenance; RxPORTAL, which allows customers to interact with the patients formulary and drug history; and RxAUTH, a prior authorization (PA) management solution for automating PA process. In addition, the company offers RxMAX, a rebate management system designed to assist health plans in managing their relationships with pharmaceutical manufacturers; Zynchros, which provides a suite of formulary management tools; and RxTRACK, a data warehouse and analysis system. It serves various organizations in the pharmaceutical supply chain, such as pharmacy benefit managers, managed care organizations, retail pharmacy chains, self-insured employer groups, unions, third party health care plan administrators, and state and federal government entities. The company was formerly known as SXC Health Solutions Corporation and changed its name to Catamaran Corporation in July 2012. Catamaran Corporation was founded in 1993, has 3,300 employees, and is headquartered in Lisle, Illinois.

Exhibit 2: (B)(N) CI Cigna Corporation – Risk Price Chart

(B)(N) CI Cigna Corporation

Cigna Corporation is a health services organization with insurance subsidiaries that are providers of medical, dental, disability, life and accident insurance and related products and services.

(Please Click on the Chart to make it larger if required.)

From the Company: Cigna Corporation is a global health service company dedicated to helping people improve their health, well-being and sense of security. All products and services are provided exclusively by or through operating subsidiaries of Cigna Corporation, including Connecticut General Life Insurance Company, Cigna Health and Life Insurance Company, Life Insurance Company of North America and Cigna Life Insurance Company of New York. Such products and services include an integrated suite of health services, such as medical, dental, behavioral health, pharmacy, vision, supplemental benefits, and other related products including group life, accident and disability insurance. Cigna maintains sales capability in 30 countries and jurisdictions, and has approximately 80 million customer relationships throughout the world and 36,000 employees.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.