Spins & Needles

Drama. Wall Street “thinks” that the Fed is going to slow down the re-purchase of its paper, thereby leaving less cash in investor hands; and possibly raise the T-bill rate a smidgen, thereby giving better yields in really “safe” paper with a high velocity and yields that might be comparable to inflation at 1% (please see our Post, Bubble-mania (Econo-speak), May 2013, for an introduction to Central Banking).

We would “think” that too if our profits were driven by trading profits and transactions fees, and we needed a reason to call our clients and get rid of all that low-yield paper on our shelf, and The Rent Was Due (Reuters, May 30, 2013, Analysis: Dividend stocks lose shine as U.S. bond yields rise).

Moreover, with the S&P 500 up more than +16% since December and +5% in May, the valuations are lofty (ibid, Reuters), they say, and, since its well-known that pigs can’t fly (but please our Post on (B)(N) SFD Smithfield Foods Incorporated, for a different view), they should be expected to descend and meanly revert; best that we help them, they say. Or possibly consider the fact that Earnings Don’t Matter and just a week ago, in Barron’s, May 25, 2013, Defending The Bull:

Of the world’s $209 trillion of financial assets, roughly $45 trillion is invested in government debt, $65 trillion is in loans, and $46 trillion is in corporate debt. With inflation at 2%, investors are poised to lock in real losses on three-quarters of the world’s investible assets. The Fed has suppressed yields and volatility, and investors don’t understand the risks they are taking when buying fixed-income products. Mis-priced capital means that companies that should be going bankrupt are continuing to exist, and some areas of the economy are suffering from over-investment.

The antidote appears to be that “volatility is correctly priced” in equities (ibid, Barron’s) and there are some who believe that we are in the early stages of a multi-year bull market, and that U.S. stocks could climb by as much as +50% in the next two years.

Doing the math, that’s $53 trillion in equities that we have to work with and $20 trillion of that is right here, onshore, in The Wall Street Put, April 2013, of which about half is in investments in equities that are “as good as cash” and “better than money”.

Nevertheless, we know that Wall Street has the clout to succeed with the same failures as in the past, and induce volatility as if it were a late pregnancy, and therefore, we need to update our stop/loss and collars (please see almost any of the (B)(N)-Company Posts), and make sure that they pay for their mistakes, rather than we.

Moreover, it can’t be said that Wall Street begrudges us a non-negative real rate of return; they only know how to do it, notwithstanding investment banking, on large volumes with small returns, and it helps them a lot if the market wants to buy what they have to sell.

We also don’t begrudge investors a non-negative real rate of return; we just know how to do it with excess returns on small volumes, if $10 trillion or so could still be considered small, and we tend to already have what they want to buy.

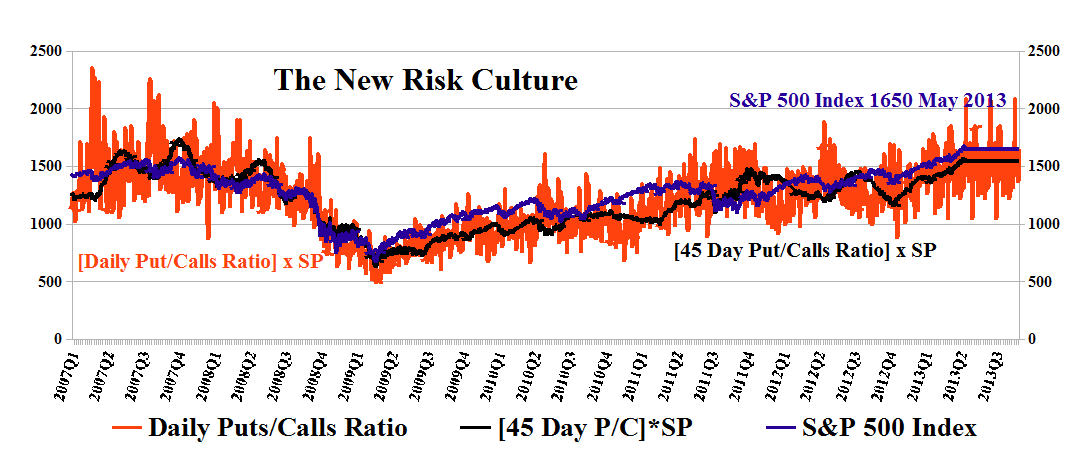

And, as scientists, we also checked our New Risk Culture Chart for anything really new, and, so far, the market is still heavily weighted by calls – which look forward to a positive future – but there are also some new negative put spikes over calls (above the index) introduced in the past week. Please see Exhibit 1 below and Click on the Link for last week and more information about the Chart.

Exhibit 1: The New Risk Culture – The End Is Nigh When It Tilts To High

The New Risk Culture Risk Price – May 30 2013

A thoughtful, well-experienced, Chinese investor said to us last week that he’s reluctant to invest his billions in the Western Markets, particularly the U.S., because they are so hard to understand. Yes.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.