Is The Rent Due?

Drama. The wets on Wall Street are praying for rain and thunder such as a “Feds hike” or new lightening in Greece, Cyprus, Spain, or wherever – anything that could trigger investor anxiety and a “flight to safety”, and some pocket-change and “rent” for the market makers, brokers, and salespersons, as investors dump their equities, take profits, and buy their bonds (The Associated Press, May 20, 2013, Despite talk of Fed changing tack, investors have so far refrained from big profit-taking).

If that seems harsh, please see our recent Posts, Frontier Justice, and Risk-On/Risk-Off or The Real Intelligent Investor and The Pensionnaires, all in May, because we too are waiting for the rain – it’s in the air – although we have no idea at all of when it might start, let alone, why it should start.

But, all of our stuff (please see below) is safely cached away, and is “as good as cash” and “better than money” already and that speaks well for the benefits of “home ownership” over short-term leasing, and, when the lease runs out or the rent is overdue, we need to move to the park bench or bespoke trailer-home by the lake (but nowhere near the Hamptons or the better parts of Connecticut).

The Sackof Suzdal by Batu Khan – February 1238 (Wikipedia)

A market retraction, or even blow-out, could happen, of course, because the investment industry is dominated by the large portfolios of the hedge funds, mutual funds, banks and insurance companies that are, in their turn, dominated by computer programs keyed to artificial targets – such as “diversification” and “mean reversion” – luxuries that are, in turn, designed to create volatility because that’s how they work (RT TV, April 24, 2013, The Tweet that rocked Wall Street: $200 billion lost on fake message).

We know what the technology is, of course, but the net result is the same as the Mongol invasions of the 13th century, and tens of thousands of years before that – if the grass is greener over there, we should go there because we don’t know how to grow our own with what we have (a B.Comm, M.B.A., and a law degree that can be used to stop the leaks but not fix the plumbing, so to speak). Does that seem harsh? Well, it’s your money, at least for now.

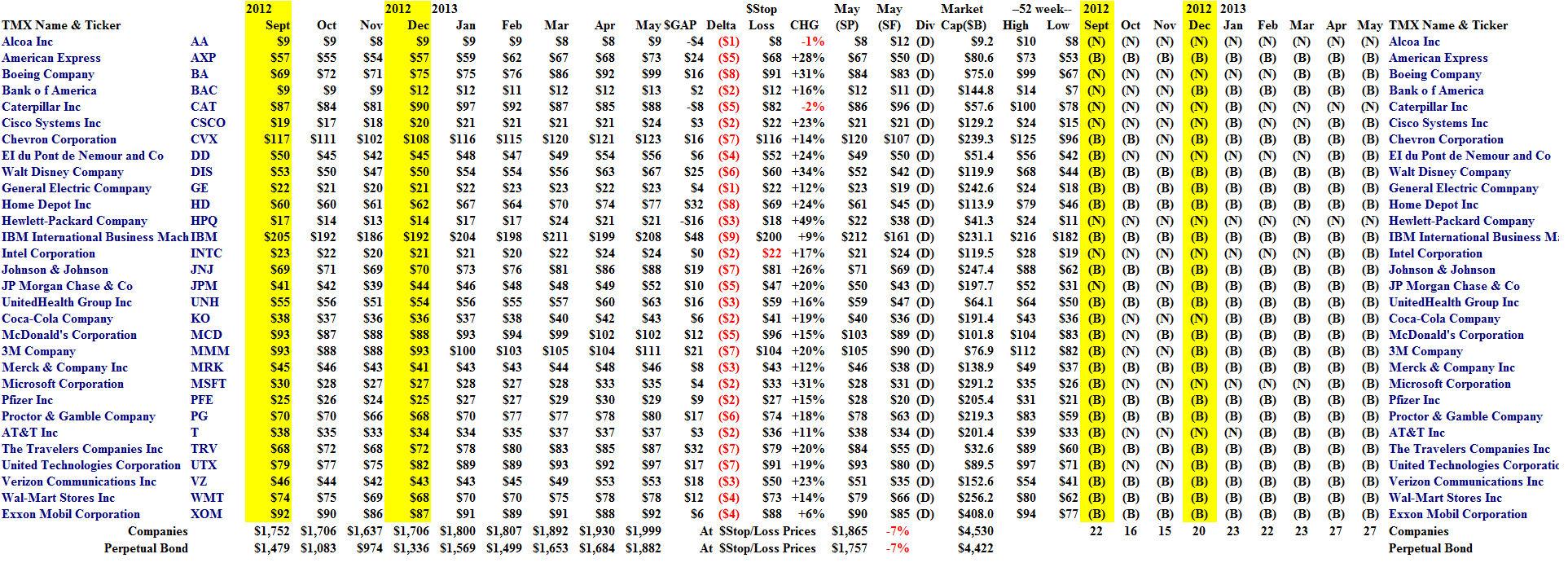

The Perpetual Bond™ in the thirty companies of the Dow Jones Industrial Companies currently has 27 companies in it, all but Alcoa, Caterpillar and Hewlett-Packard (which we’ve discussed in previous Posts; please use the Search box to track anything that we talk about that might not be familiar); and we’ve made 9 buys and 2 sells in the portfolio since December, always in blocks of 1,000 shares for the purpose of this report (please see Exhibit 1 and 2 below).

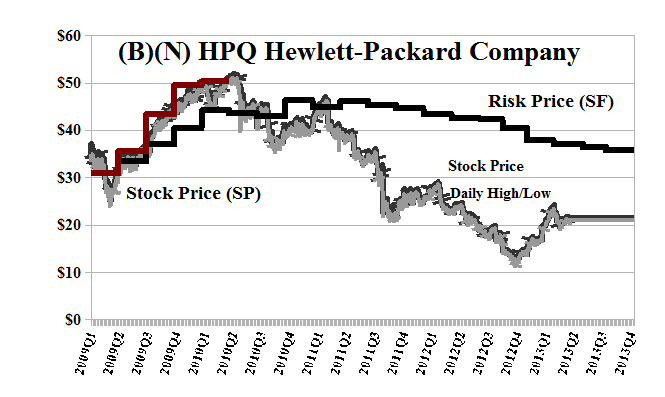

Both Alcoa and Caterpillar are down (-1% and -2%, respectively) but Hewlett-Packard is up +49% and we’ve had to leave those profits for other investors – who are obviously buying it on speculation or “good value” and a possible dividend yield of 2.4% – because we still can’t find a reason to own the stock (please see Exhibit 3 below; and the apparent new labor issues in their manufacturing contractors don’t help – The New York Times, May 20,2013, 3 Foxconn Employees Are Said to Have Committed Suicide).

The portfolio is up +16% in contrast to the Dow itself (which is also a price-weighted index on all thirty companies) which is up +17%, and obviously, we could have done just as well by buying and holding all thirty of companies, absent a “surprise” that we would have no basis to foresee. We’re just “there” but we don’t know where that is, so to speak.

If we do nothing but set our stop/loss prices as indicated in Exhibit 2, and there is a market blow-out, and everything drops, then we could lose minus (-7%) of the current portfolio and the portfolio value would drop from the current $1,882,000 to $1,757,000, all in cash (please see the bottom of Exhibit 2 for the stop/loss analysis and our current stop/loss prices for all the companies based on the demonstrated stock price volatility).

But we don’t have a problem with “collaring” everything that we own, and that can sometimes be done with profit (please see almost any of our (B)(N)-Company Posts) and, in any case, would siphon off no more than 2% of our current profits, which is easily covered by the dividends already received.

On the other hand, if we have the stop/loss, we could also be more selective and just protect those companies that might lose the most, or have a high correlation with the market (high Betas). For example, American Express is currently trading at $73 and has a stop/loss of $68 and a “beta” estimated to be Beta=1, so that the stock price of American Express will tend to do what the market does (although, obviously, it’s done a lot more than the market so far this year).

The July put at $70 costs $0.85 per share today and the cost of that can be offset by the sold or short July call at $78 for $0.85 (also), so that for a cost of $73 to hold the stock and a collar at $0 net ($0.85 less $0.85), we can hold the stock at between $70 and $78 for the next several months and continue to collect our dividends for a current yield of 1.3%.

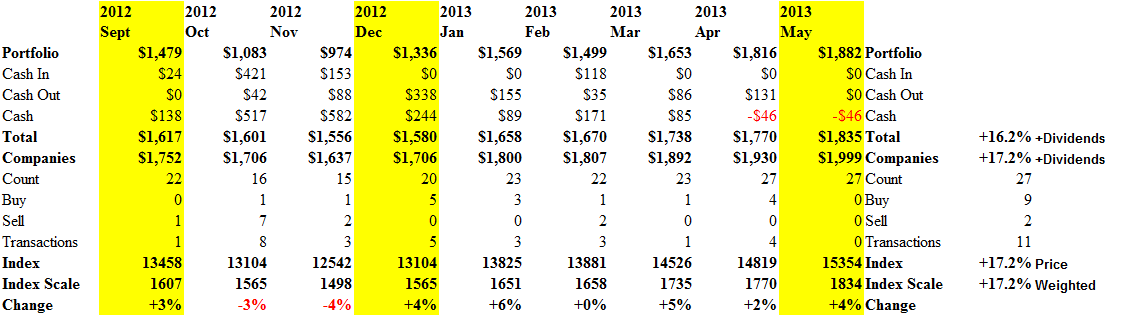

Exhibit 1: The Dow Jones Industrial Companies Perpetual Bond™ – Cash Flow Summary – May 2013

The Perpetual Bond – Cash Flow Summary – May 2013

(Please Click on the Chart to make it larger, and again, if required.)

Exhibit 2: The Dow Jones Industrial Companies Perpetual Bond™ – Portfolio Summary – May 2013

The Perpetual Bond – Portfolio Summary – May 2013

(Please Click on the Chart to make it larger, and again, if required.)

Exhibit 3: (B)(N) HPQ Hewlett-Packard Company – Risk Price Chart

(B)(N) HPQ Hewlett-Packard Company – May 2013

Hewlett-Packard Company is a global provider of products, technologies, software, solutions & services to individual consumers, small- and medium-sized businesses and large enterprises, including customers in the government, health and education sectors.

(Please Click on the Chart to make it larger if required.)

We only buy and hold the stock if the ambient stock prices summarized as the Red Line Stock Price (SP) appear to be at or above the Black Line Risk Price (SF), and for no other reason. But that hasn’t happened since between $30 and $50 in 2009, after which we bailed.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.