The S&P TSX “Hangdog” Market

Drama. We’ve hastened to update our recent Post on this subject (please see May 3, less than three weeks ago) because it is said that the U.S. investors might decide that the U.S. markets are too hot to the point of “glowing” or “radiating”, and so seek the cooler, becalmed, waters to the North for more bargains and lower-priced equities to buy (Reuters, May 21, 2013, TSX hits 1-1/2 month high on broad rally, positive data).

According to the article, investors are “starting to recognize “value” in the TSX” and “a number of names are blowing higher” (or less precociously, like “leaves” or “fans”, we guess) and “you can make money (they say) in Canada if you avoid the commodities” (ibid, Reuters).

Another reason to focus on the Canadian market is this: What if Mr. Bernanke doesn’t raise the Fed Rate by 25 basis points tomorrow? And the market doesn’t drop the hot stocks and race to quality and buy U.S. Government Bonds (notwithstanding the current debt burden of $17 trillion and rising, which is only a problem in election in years, in any case)?

If that happens, and there’s nothing to buy or sell tomorrow, How will they pay their rent? Please see our recent Post, Is The Rent Due?, May 2013, and for more information on investing in foreign markets, Frontier Justice, May 2013. Best that they find or discover some “value” in Canada, and take their clients with them.

Compelling arguments, indeed, and so we’ve set up the kiosk in Canada, and we’re giving them that “come hither” look and free ice cream, because their money is as good as ours, and could be better if the CDN$ sinks to just US$0.90, as some economists are suggesting (The National Post, May 13,2013, Loonie overvalued by as much as 10%, warns BMO chief economist) ; in that case, even our commodities will look better, and stock prices and dividend yields will look too cheap against the US$ for that reason alone. And, thereafter, they would have no place to go but up, one would think? Please see our Post, The Real Intelligent Investor, May 2013, for a counter-argument.

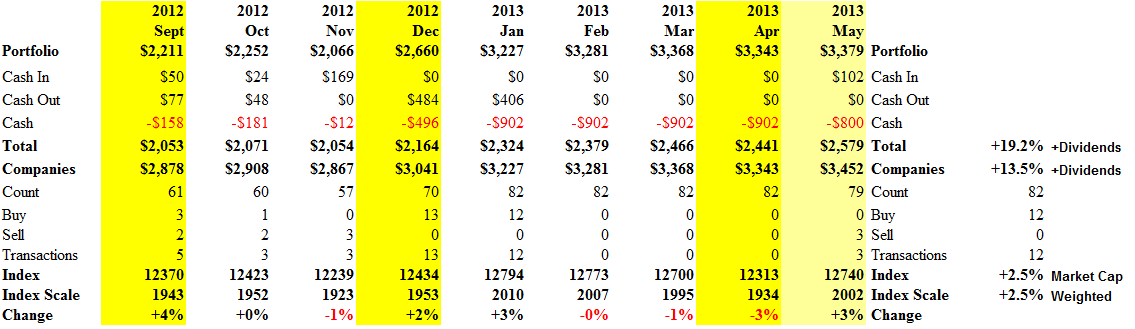

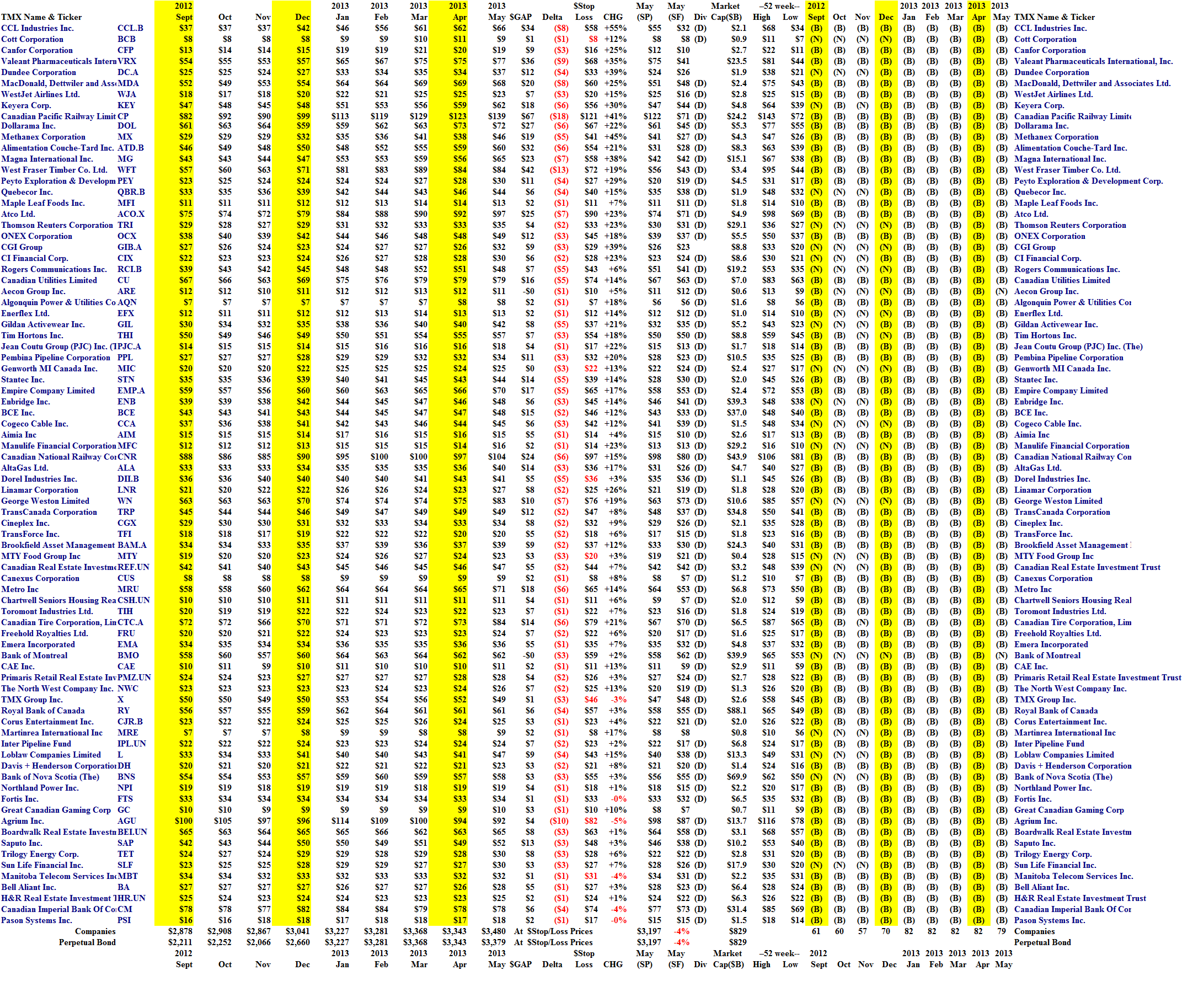

The portfolio that we posted at the beginning of the month (please see our previous Post) is up another +6% (plus dividends) to +19.2% for the year, so far, and the companies in it are still the same – we haven’t done anything for a month and even three months – except for three companies that we sold in May; Primaris Retail REIT was bought up at $28 (over $24 in September) by a group led by KingSett Capital (please see our Post, (B)(N) PMZ.UN Primaris Retail REIT, January 2013); and we sold the Aecon Group Incorporated and the Bank of Montreal on (B)- to (N)-transitions between April and May (please see Exhibit 2, and Exhibit 3 and 4 below for a brief recap of that situation).

Of course, we’re always in the Canadian market because we think that there’s always something to buy and hold in any market, and about half of the Canadian big-cap market of $1.7 trillion is already in our portfolio and up +19.2% for the year, in contrast to the whole market which is languishing at +2.5% (please see Exhibit 1 below).

So, if they’re looking for “low prices” and “cheap deals” then they ought to buy into the companies that we don’t own, at the present time, and boost their prices with fresh money. There are over two hundred (200) companies that we don’t own and which are trading now at discounts in excess of minus (-20%) since December, and they’re not all “commodities” and they’re not going away because their “stock prices” don’t really matter to them, absent a takeover or activist investor.

But if they’re looking for investments that are “as good as cash” and “better than money”, then they should buy more of what we already have (please see Exhibit 2 below) which would certainly encourage us to hold on to what we have, absent any “surprises” that could come from anywhere, or are already blowing in the wind.

Exhibit 1: (B)(N) S&P TSX Perpetual Bond™ – Cash Flow Summary ($000) – May 2013

S&P TSX Perpetual Bond – Cash Flow Summary – May 2013

(Please Click on the Chart to make it larger, and again, if required.)

Exhibit 2: (B)(N) S&P TSX Perpetual Bond™ – Portfolio Summary – May 2013

S&P TSX Perpetual Bond – Portfolio Summary – May 2013

(Please Click on the Chart to make it larger, and again, if required.)

Exhibit 3: (B)(N) ARE Aecon Group Incorporated – Risk Price Chart

(B)(N) ARE Aecon Group Incorporated

Aecon Group Incorporated along with its subsidiaries, provides construction and infrastructure development services to private and public sector customers in Canada.

(Please Click on the Chart to make it larger if required.)

Exhibit 4: (B)(N) BMO Bank of Montreal – Risk Price Chart

(B)(N) BMO Bank of Montreal

Bank of Montreal is a financial services provider based in North America. It provides retail banking, wealth management and investment banking products and services.

(Please Click on the Chart to make it larger if required.)

We only buy and hold the stock if the ambient stock prices summarized as the Red Line Stock Price (SP) appear to be at or above the Black Line Risk Price (SF), and for no other reason. Please see the notes and references below and any of the (B)(N)-Company Posts for more details.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.