Extraterrestrial Funds (ETFs)

Drama. ETFs (Exchange Traded Funds) are designer products created by the investment banks for retail consumer investors. With an ETF, which costs almost nothing to buy in terms of fees, we can buy “exposure”, “risk appetite” and “diversification” on exotic heavy metals such as global gold & silver mines (“precious metals” otherwise on the shelf); fading industrials distinguished largely by size such as “large-cap” or “small-cap”; emerging markets today but not necessarily tomorrow; hydrocarbon sludge and chemical waste of all sorts deemed oil & gas and industrials; and, foreign currencies deemed “money” while they last.

All right, we’re not fans of ETFs because there is no “risk management” for the buyer other than the Prospectus, which might not be what we want. We want 100% Capital Safety and 100% Liquidity and a hopeful return above the rate of inflation, and the only investment product that does that is the Perpetual Bond™, although we can get 100% Capital Safety and a guaranteed return at the rate of inflation by buying TIPS (Treasury Inflation Protected Securities) or RRBs (Real Return Bonds) and these cost nothing to buy in terms of fees – the government is glad to get our money without raising taxes or cutting benefits. The other problem with ETFs is that one really doesn’t know what’s in them, and the Prospectus, which is the only guarantee that we get, can provide the fund managers with a lot of flexibility, especially if they’re dealing with equities and are not responsible for the returns.

For example, if we were running an ETF instead of the Perpetual Bond™, then we could well afford to charge some small recurring fee next to nothing, because we can invest the capital in the companies or assets that are expected to follow the Prospectus, which is usually some index or standard AND keep both the dividends and the capital gains in excess of what we are required pay to the shareholders AND – the “best” part – if there aren’t any capital gains or dividends in excess of the Prospectus, or even losses, the shareholders will carry the risk but not the rewards. That’s the reason that a “retail consumer investor” is anybody – mutual funds, hedge funds, endowment and trust funds, pension plans, and so forth – who is not an investment bank – we carry the risk, they get the money. Investment Banks only go wrong in this type of deal, and others of their design, if they are investing their own money for themselves and a mutual fund of other peoples money which they own by control, for example, is certainly a “good place”, a dumping ground, to pass on their mistakes.

We can do better by “exposing” ourselves, so to speak, and just buying a piece of everything that we might be interested in. For example, we can buy the Dow today – all thirty companies – in blocks of 100 shares for $188,200 (an average of $63 per share – weighting is almost irrelevant), keep the shares for as long as we like, and just collect the dividends which will be about 4% of the capital ($7,500 per year) most of the time, in aggregate. That’s what we call an “Extraterrestrial Fund” – it radiates money at a low frequency at no more risk than “exposure” to anything else that we might buy in that class of investments that might otherwise be an ETF. For more examples in other markets, please see the Companies Line in any of the Cash Flow Summaries, such as The Dow Transports ($102,400) or “all of New York. Buy America.” The Wall Street Put ($1,334,500).

To do still better, we can manage these portfolios as a Perpetual Bond™ which not only tends to perform better for reasons that we understand and can reasonably expect to repeat, but also has 100% Capital Safety guaranteed at all times.

For example, for “exposure” to raw gold bullion (which is a “shiny”, heavy-looking, metal in the advertisements, but it’s not “shiny” and we would use it for a door stop or paper weight, but for the temptation to steal it.), the GLD SPRD Gold Trust is an ETF with a current market or asset value of $63 billion and a current stock price of $154 per share (405.7 million shares outstanding) and an estimated downside volatility of minus ($7.50) which trades in excess of 10 million shares a day on an average day, and pays no dividends. It’s committed to hold only gold bullion (and at current prices has about 60 tonnes of it, somewhere) and not the companies that produce it. But where does the gold come from and who wants to receive a “basket” of gold, or certificates for gold, which we have to sell to get our “money”?

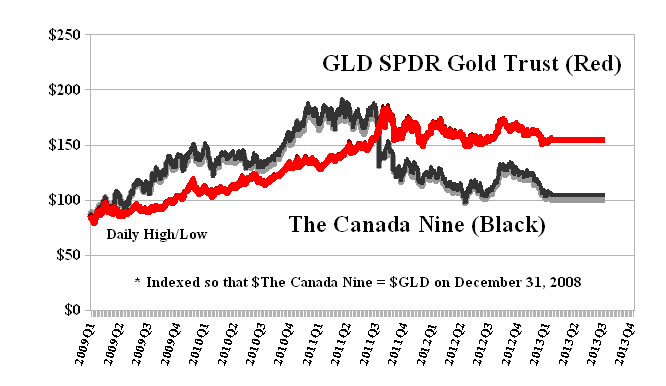

The Chart below (Exhibit 1) shows the actual price of the SPDR Gold Trust (Red Line) which is $154 today and up from $87 in early January 2009 for a gain of +80% over four years, but no dividends. The Black Line is “The Canada Nine” of the combined stock prices of the nine largest gold mines in Canada, calibrated to an equivalent purchase of the SPDR Gold Trust in early 2009, and simply held without change as stocks since then.

Exhibit 1: GLD SPDR Gold Trust and The Canada Nine (Gold Mining Companies)

(Please Click on the Chart to make it larger if required.)

(ETF Brief Prospectus) The SPDR Gold Trust seeks to replicate the performance of the price of gold bullion, net of expenses. The trust holds gold, and is expected to issue “baskets” of certificates in exchange for deposits of gold, and to distribute gold in connection with the redemption of baskets. The gold held by the trust will only be sold on an as-needed basis to pay trust expenses, in the event the trust terminates and liquidates its assets, or as otherwise required by law or regulation.

(The Canada Nine Brief Prospectus) We bought 1,000 shares of each of nine gold mining companies for $201,240 in early 2009. This portfolio was held without change since then and is currently worth $231,700 for a +17% capital gain and has paid $15,975 in dividends to date for a total return of +23% over four years (compared to the ETF of +80%).

But wait, what happened in the 4th quarter of 2011?

“On Monday, it (the price of gold) lost 2.5 percent for its worst drop in nearly two months in a global market maelstrom rattled by euro zone debt fears and the apparent inability of U.S. politicians to reduce government debt by $1.2 trillion.” – Reuters, Tuesday, November 22, 2011, Gold up over 1 percent on option bids, technicals weak.

And the Gold SPDR hasn’t done anything since, and although the Gold SPDR price is holding steady at more or less $160, nobody knows when it might next do something either up or down. In contrast to the SPDR, we know something about the companies that are in The Canada Nine and we can run the portfolio more proactively as a Perpetual Bond™ rather than as just a basket of stocks of companies with gold production.

The Cash Flow Summary (Exhibit 1 below) shows that by the time we got to December 2011, the portfolio that we bought for $201,240 in early 2009 and which held all nine companies (please see Exhibit 3 blow) has been reduced to just two companies (Count Line) worth $54,140 (Portfolio Line) and a cash account of $219,180 (Cash Line) for a capital gain of $72,080 and a three year return of +36% (+11% per year on average) plus dividends. Also, in practice, there is no need for us to maintain such a large cash account (which results from portfolio gains and selling stocks ex dividend) and the money could be used to buy more of what we have, or what re-enters the portfolio, or diversified into other markets. It’s also evident that even the portfolio of all nine stocks, if bought and held unchanged, outperformed the Gold SPDR to the end of 2011 (please see Exhibit 1 above). Moreover, whereas the entire gold inventory of The Canada Nine is $8.2 billion (please see Exhibit 3 below) and they have production options, the Gold SPDR is only exposed to gold, $63 billion of it, or nearly eight times as much. What can it do? Go to cash and unload its inventory so that it can buy it back at lower, or higher, prices?

Exhibit 2: The Perpetual Bond™ in The Canada Nine – Cash Flow Summary

(Please Click on the Chart to make it larger, and again, if required.)

The Portfolio Summary (please see Exhibit 3 below) shows the ambient stock prices at which we bought and held or might have sold (“selling” is a discipline that we discuss below) the companies in The Canada Nine. The $GAP is the difference between the current stock price and the Risk Price (SF); it is positive if the company is deemed investment grade, (B), and negative if trading in the volatility zone, (N), in which case it is not in the Perpetual Bond™. A company is in the Perpetual Bond™ if and only if the ambient stock prices appear to be above the price of risk which is calculated as the Risk Price (SF) and only updated as new balance sheet information becomes generally available (for example, we don’t really care about earnings reports or forecasts or market news; if, whatever it is, is not in the stock price now we don’t care). The Delta is our estimate of the reasonably expected downside in the stock price due to the demonstrated near-term volatility (the current quarter). If all the $Stop/Loss prices are executed and we are sold out of The Canada Nine completely, then the portfolio value drops to $203,000 from $235,000 for a loss of minus (14%), or if we are sold out for the two companies that are currently in the Perpetual Bond™, then the portfolio value would drop from $66,000 to $58,000 for a loss of minus (12%) and, obviously, for a lot less money. Because we’re long in those stocks, we could also “collar” the prices (please see below for an example). The CHG column is the stock price change since December 2008 (four years) and it is, dramatically, mostly negative for all of The Canada Nine with the exception of the Franco-Nevada Corporation (+29%) and Agnico-Eagle Mines Limited (+7%).

Exhibit 3: The Perpetual Bond™ in The Canada Nine – Portfolio Summary

(Please Click on the Chart to make it larger, and again, if required.)

Only Yamana Gold Incorporated and the Franco-Nevada Corporation have been substantially in the Perpetual Bond™ during the past four years, and are in it now, although others have come and gone, particularly in the early years until November 2011. Please see our recent Post, (B)(N) ABX Barrick Gold Corporation, January 2013, for more information on Yamana Gold (and the Barrick Gold Corporation) and The Canada Pension Bond, January 2013, for the Franco-Nevada Corporation. These companies have a market capitalization of $11.6 billion and $7.1 billion, respectively, but neither of them have a significant gold inventory (please see Exhibit 3 above).

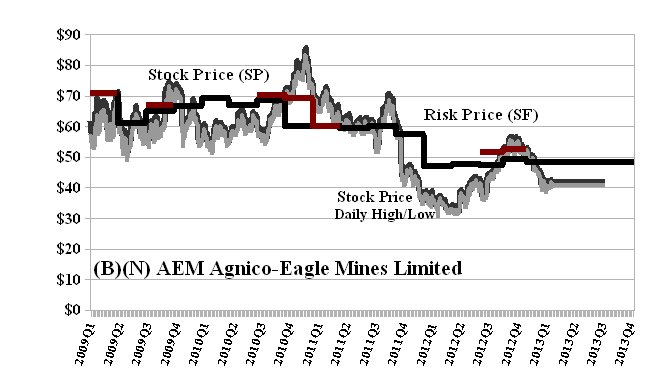

Agnico-Eagle Mines Limited was eligible for the Perpetual Bond™ in September 2012 at $49, increased to $56 by December, but has since dropped out at $41 which is below the current Risk Price (SF) of $45 (please see Exhibit 4 below). The indicated Delta is minus ($6) so that $49 less $6 ($43) would have put us below the Risk Price (SF), so we “collared” the stock price, instead, by buying the January put at $49 for $1.40 per share and shorting or selling the January call at $53 for $1.21 so that for a net cost of $0.19 per share ($1.40 less $1.21), we were sold out or “called” in December at $53.

Exhibit 4: (B)(N) AEM Agnico-Eagle Mines Limited – Risk Price Chart

Agnico-Eagle Mines Limited is a gold producer with operations located in Quebec and Finland, and exploration and development activities in Canada, Finland, Mexico and the United States.

(Please Click on the Chart to make it larger if required.)

From their Mission Statement: Agnico Eagle’s mission is to run a high quality, easy to understand business, that generates superior long-term per share returns for our shareholders, creates a great place to work for our employees, and that is a leading contributor to the wellbeing of the communities in which we operate.

Their five mines are 100% Company owned gold deposits located in the mining friendly regions of Canada, (northwestern Quebec and Nunavut), northern Finland and northern Mexico, and they produced a record 1.1 million ounces of gold in 2012 and almost 4.7 million ounces of silver. They pay a dividend of $0.22 per share per quarter for a total of $152 million per year and a current yield of 2.1% BUT the stock prices trade almost exclusively in the volatility zone, (N), of investor uncertainty, and 500,000 to 1 million shares (of 173 million outstanding) change hands every day. Please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the meaning of the “price of risk”.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

Exhibit 1: