(B)(N) ABX Barrick Gold Corporation

Deal Book. Barrick Gold Corporation is a Canadian-based company with gold mining, exploration and development operations all over the world. It produced more gold last year (210 tonnes) than the next four Canadian competitors combined (Kinross, Goldcorp, Yamana and Elderado with 190 tonnes between them) but the industry as a whole lost $2.4 billion last year, a quarter of which was Barrick’s ($665 million) in a $5 billion reversal of fortune from the year before.

Barrick Gold Corporation

It’s still one the world’s largest gold producers, and a recent award winner in the Dow Jones Sustainability Indices, but it hasn’t been “investment grade” since 2010, three years ago, and it seems that some of its biggest shareholders are just finding that out now (The Canadian Press, September 17, 2013, Investors pushing for changes on Barrick Gold board: reports).

We don’t know how much they’ve lost but the $50 billion company in 2010 is now an $18 billion company and it recently slashed its dividend payments from $200 million a quarter to $200 million a year, for a current yield 1%.

Bigger Fish Have Lost Their Way

The alleged activist (and secretive) hedge fund, Two Fish Management LLC, which specializes in buying and managing short (that is, sold) put option portfolios for its clients and believes that volatility is an underutilized investment asset, might have had to buy a lot of Barrick for its clients at prices even lower than it might have anticipated, and it is now searching for “hidden value” in the break-up of the company (ibid, The Canadian Press, and Reuters, September 15, 2013, Barrick Gold shares could surge from activist interest-Barron’s).

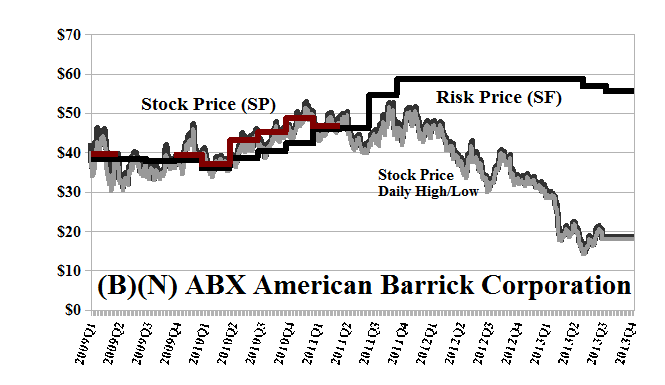

Although Barrick, despite its size and preeminence, has never been a compelling buy for us, we held it in the Perpetual Bond™ between $40 and $50 in 2010 and were sold out on a stop/loss at $45, and haven’t owned it since because it’s trading below the price of risk, Risk Price (SF), then $45 and now well over $50. Please see Exhibit 1 below, Red line Stock Price (SP) above the Black line Risk Price (SF) and for no other reason would we buy and hold it.

But the company has never, in its entire history, traded above $55 per share. How should we ever expect to buy it again?

Although it’s complicated, and just the highlights are 78 pages in length, the Two Fish co-principals, Mr. Mike Morris and Mr. J.R. Sauder, have a plan (please see the slideshare Two Fish Management’s Perspectives on Barrick Gold Corporation – An Empirical Study) to restore Barrick to “fair value” which they calculate at $44 per share from the current $18 to $19, and which, through the sale of off-shore assets, paying down debt, trimming operations, and buying in stock, returns the company to what it was in 2010, with a “risk price” of $44, in fact, and they estimate that the company would be worth at least between $40 to $50 per share, and possibly retail for as high as $70 per share to the latecomers.

It is, of course, quite difficult to find buyers for off-shore assets in the Congo, and therefore the Two Fish have suggested spinning-off the money-losing and capital intensive assets of African Barrick, Australia Pacific, and the Global Copper Platform, to its shareholders, and re-aligning the company (“a spinal adjustment”) to its North and South American properties.

All of that might be true, and it could be done in haste, more slowly, or not at all, but we believe that it is up to the management of the company to decide what they will do.

As investors, we already have a job – our only job is to weigh the companies, not to “scale” them (so to speak), and when it comes to weighing the companies for our money, there are many fish in the sea, not the least of which is The S&P TSX “Hangdog” Market portfolio and Perpetual Bond™ which currently has eighty-three companies in it (and more than one hundred and fifty that are not, including Barrick and none of all the golds this year) and has returned +24% (plus dividends) so far this year, and we know exactly how to make the next investment decision that might affect our investment returns, even though we know next to nothing about all of these companies, and hundreds of others that ply the capital markets.

Please Click on the links for an update of the Cash Flow and Portfolio (one page).

Exhibit 1: (B)(N) ABX Barrick Gold Corporation – Risk Price Chart

(B)(N) ABX Barrick Gold Corporation – September 2013

Barrick Gold Corporation produces and sells gold and copper. The Company business activities also includes exploration and mine development. It holds interests in oil and gas properties located in Canada.

(Please Click on the Chart to make it larger if required.)

From the Company: Barrick Gold Corporation engages in the production and sale of gold and copper. It is also involved in exploration and mine development activities. The company holds interests in the producing gold mines, which are concentrated in North America, South America, and Australia Pacific; producing copper mines located in Chile and Zambia; and a mine under construction is located in Saudi Arabia. In addition, it holds interests in oil and gas properties located in Canada. As of December 31, 2012, the company had proven and probable mineral reserves of 140.2 million ounces of gold, 1.05 billion ounces of silver contained within gold reserves, and 13.9 billion pounds of copper. Barrick Gold Corporation was founded in 1983, has 28,000 employees, and is headquartered in Toronto, Canada.

For more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}