(P&I) CPPIB 2nd Quarter

Another Accounting Error?

+1.8% on $180 billion

Drama. The difference between +1.8% and -1.8% is a whopping 3.6% but they are each still close enough to zero that either could be an accounting error and not an investment return at all (Pensions & Investments, November 8, 2013, Canada Pension Plan returns 1.8% in quarter).

Which gives us pause and raises a doubt because the Canada Pension Plan Investment Board (CPPIB) is successfully managing the plan to “spec”, that is, towards a +4% real return this year and every year for nominal (on paper) investment returns of +5% to +6% every year, on average, for the foreseeable future to 2021 and beyond, perhaps for the next 75 years.

No, thank you. We can’t.

We have a plan that doesn’t allow “donations” given or received.

But that’s hard to do this year – and is even an amazing result – because the markets are almost all showing double digit returns and writing a blank cheque for investors.

How does the CPPIB end up with only +2.9% for the last six months in a double-digit market and should we expect +6% for the year ending next March despite the markets?

And if they do a lot more than that such as +8% or +12% which is free for the asking in a buoyant market then they are “out of control” and subject to the usual “accident theories” of investment management that are “orthogonal” to the plan.

Efficient Frontier (B)(N) Boundary Open

Our Goal Is “100% Capital Safety And A Hopeful Return Above The Rate Of Inflation”

The problem is that the CPPIB’s goal is to “maximize investment returns without undue risk of loss” which sounds good (powerful) but is unprovable and has provably failed in the recent past, dramatically such as in 2008 and 2009, and it is failing now because it’s not making money in a double-digit market that is demonstrably “risk free” – that is, there is “volatility” as there always is but “volatility” is not an investment risk and we have to proactively look for “investment risk” to find some. And they do. Please see below.

The solution is to re-state the goal as “our goal is to provide 100% capital safety – we will not lose your money no matter what – and a hopeful but not necessarily guaranteed return above the rate of inflation” or in other words, to provide a guaranteed non-negative nominal return and a hopeful non-negative real return which leaves the positive returns open-ended but within “spec” and that is a provable rule.

A “new rule” you say?

The rule is open-ended and sets the floor against investment losses – we will not lose your money no matter what – but sets no limits on what might be achieved and doesn’t “ham string” the management to meagre returns in booming markets.

And it also prevents “booming” paper losses that might affect essential cash flow in failing markets which they are bound to do.

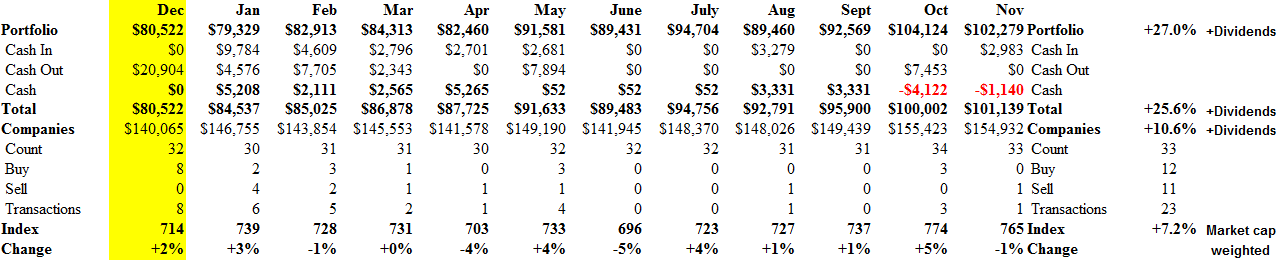

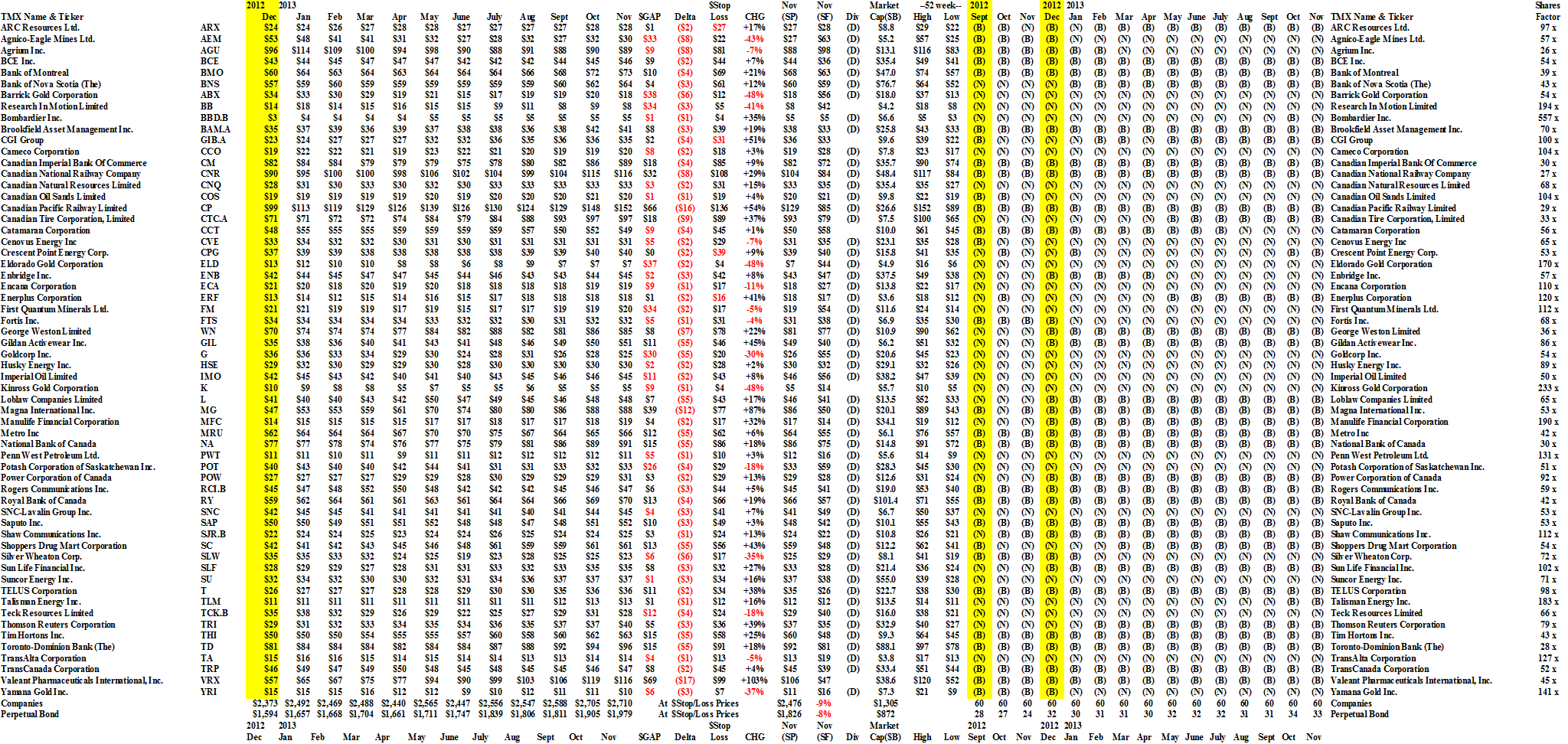

For example, $1 billion invested in each of the sixty companies of the S&P TSX 60 has returned +10.5% this year plus dividends of another +3.1% and the same investment managed as a Perpetual Bond™ with 100% capital safety has returned +25% plus dividends and will not return less than that for the rest of the year. Please see Exhibit 1 below and click on the links TSX 60 Prices & Portfolio and Portfolio & Cash Flow for more detail.

From just $60 billion in January, we can cash out $15 billion in capital gains and $2 billion in dividend income and still be as good as we were for the next year.

Exhibit 1: S&P TSX 60 – Cash Flow Summary – November 2013

S&P TSX 60 – Portfolio & Cash Flow Summary – November 2013 – In Brief

(Please Click on the Chart to make it larger if required.)

To us, the demonstration of that fact every day, every month and every quarter is more meaningful than investment assets in Brazil, Australia and Neiman Marcus, for example (ibid, P&I). How are those investments going to provide us with non-negative real returns in the future if they can’t do it now? And if they do more than that, then they are running out of “spec” and it can be said that we don’t know what we’re doing.

And what good is it that for the next quarter that we are now 33.4% invested in public equities compared with 31.8% three months earlier; or 32.3% fixed income versus 33.6%; or 17.2% private equity versus 17.7%; or 11.4% real estate versus 11.1%; or 5.7% infrastructure versus 5.8% three months ago (ibid, P&I)?

S&P 500 Total Real Returns – 20 & 30 Year

2% More Equities You Say?

Data Courtesy Of: Robert J. Shiller, Yale University, 2013

We ought to know that there is nothing that we can do about market volatility whether in bonds or equities in ours or other countries or in fixed assets anywhere that are already “rusting”.

Nor should we do anything about it. “Volatility” is not an investment risk. But “managing” it is.

For more information on the Chart elements and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}