(P&I) We Will Win. But Not Today.

Drama. The Canada Pension Plan (CPP) is an example of a Defined Contribution pension plan in which the clients or customers pay a certain amount of their income every year in order to secure “retirement benefits” when they choose to stop working which could be any age from age 60 to 70 notwithstanding a disability. This year, for example, the maximum contribution is $4,712.40 and it is usually split between the employee and their employer on maximum contribution earnings of $51,100 at the rate of 9.9% on earnings between a minimum of $3,500 ($346.50 per year) and the maximum.

A Tidy Capital Sum

The plan has not been around all that long (since 1965) and the contribution rate was originally 1.8% of annual gross earnings in 1965 and that has been increased several times with great debate to the current 9.9% in less than 50 years. One would think that if we were saving and investing 10% of our gross income every year (which we will take to be $51,100 now and the same when adjusted for inflation either backwards or forwards) that we would have a tidy capital sum in forty years.

And that’s where the trouble starts and ends.

For example, a real return of 4% a year on 10% of our income which, as above, we will always take as a real $51,100, although the actual amount doesn’t matter, will accumulate to a real 12× that amount in 40 years and 29× and 87× that amount if the real return can be boosted to 8% or 12% every year.

Moreover, a capital sum of that amount can be actuarially annuitized to pay any fraction of that amount for the rest of our lives. In fact, at age 60 with a capital sum of 87× our “income”, we can expect to draw down at least twice our income for the next forty years, which should just about cover it.

Fate

The problem is that no one, not even the government, can be trusted to allow that kind of capital accumulation across millions of citizens and, secondly, no one knows (they say) how to obtain a real return of 12%, 8% or even 4% every year for forty years on a large capital accumulation. For example, the last fifty years have been more or less benign as far as wars, pestilence and revolution are concerned, but try to remember the fifty years before that, since 1915, and how unlikely it is that the benevolent institutions and robust capital markets that we rely on will remain so for the next fifty years.

And the fears are already surfacing and the arguments are already beginning as the various parties and beneficiaries have their eyes on a large capital pool which they fear is not sufficient and will never be sufficient in a debate that has already been going on for several years (The Canadian Press, November 1, 2013, Ontario, PEI pushing CPP enhancements as finance ministers meet in Toronto and Provincial, territorial finance ministers agree that CPP needs improvements).

The problem is (in our view) that we can’t win only with promises of a better tomorrow. We have to win now and every year to prove that we can win tomorrow. Increasing the contribution rate from 10% to something else just defers the problem and is a job killer, a wage killer, and a spending killer, none of which are good for the consumers or the economy and, obviously, as already demonstrated by fifty years of bickering over the solution, it doesn’t solve the problem. There is just too much money there to be left alone.

For example, the Canada Pension Plan Investment Board (CPPIB) has the responsibility of investing CPP contributions that are in excess of the amounts required to pay CPP benefits and it has accumulated a large capital pool of $180 billion at the present time that is reasonably expected to grow to $800 billion in real and current terms in the next thirty years.

How does one invest $800 billion today in order to get a real 4% ($32 billion), 8% ($64 billion) or 12% ($96 billion) return in one year? Every year.

Trivial? You say?

$800 Billion

The answer is that it’s trivial to do that and to assuage the fears of the plan beneficiaries, amounts in excess of what it is deemed prudent or worthwhile to keep should be returned to the contributors, who are the future beneficiaries, now.

The pension funds, of which the CPP is just one example, are in a terrible dilemma but it’s one of their own design.

Pension fund managers, their Boards of Directors and their sponsors, and their clients (which are we), have quite naturally confused “capital” – great piles of cash and investment assets – with “income” and have assumed, hope, or believe that ever greater piles of cash and investment assets will be there in the future to produce an adequate income then which they can’t produce now.

Entropy

Courtesy: Creative Juice

If we as consumers of “pension plans” sponsored or overseen by governments and large corporations think that surely nothing “bad” can happen between now and then, in our retirement in ten, twenty, or thirty or more years from now, then we haven’t been listening to our parents, or talking to our grandparents, and we haven’t been paying attention in history class and we don’t know the laws of nature.

Surplus People

Courtesy: County Wicklow Heritage

And, of course, that’s why most of us are in Canada or the United States or Australia and many other places – because large capital pools of cash and investments didn’t do it for our parents and grandparents and great grandparents either.

There is no government controlled or sponsored “pool of liquid assets” that has survived more than one generation which we take to be between twenty to forty years but the money is usually gone in much less time. “Money” is always wiped out by theft, mismanagement, inflation and even hyperinflation in the course of the great societal events that move us. And the frontiers are getting smaller and smaller.

Why is this problem trivial?

Why is this “problem” trivial?

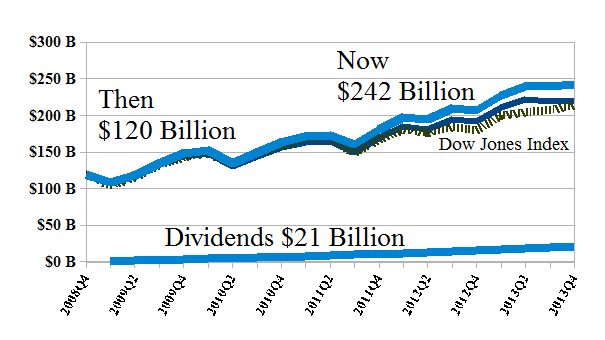

At the end of 2008, the fund was worth $120 billion but it hadn’t hit bottom yet. By the end of March (which was the end of the fiscal year called 2009), the fund was worth only $105 billion. All they ever had to do at the end of 2008 was “buy the Dow” – that is, invest $4 billion in each of the thirty Dow companies, no matter what price or alleged “condition”, and then do nothing else for the next five years. Please see Exhibit 1 below.

Exhibit 1: The Fund 2009-2013

The Fund 2009-2013

In other words, without putting in another one of our thin dimes, the fund today would be worth $60 billion more than the $180 billion that it is, subsequent to its investment results and net contributions that seem to be of the order of $6 billion per year.

(Please Click on the Chart to make it larger if required.)

And we would have earned $21 billion in dividends (roughly $4 billion per year and rising) which could be used to help with the current accounts.

Of course! it’s easy to do a lot better than that but then we have to know what we’re doing! We need to be “investors” – we want our money to be safe – 100% capital safety – and obtain a hopeful but not necessarily guaranteed return above the rate of inflation.

This year’s Dow is up a spectacular +18% because investors are buying stocks and have stopped waiting for “high yielding” government handouts. On the other hand, the Perpetual Bond™ which uses essentially the same strategy as above – we buy them all with an equal amount of money in each – but, in our case, not necessarily all of them at the same time, is up +33% plus dividends or +20% if we sell out now because we need all the cash. Please see Exhibit 2 and 3 below.

And, of course, if we had done that with $180 billion in January (which is less than 5% of the market), we’d have $4.5 billion in dividends to spend and we could take capital gains of $36 billion for even more money to spend, and still be as good as we were for the next year.

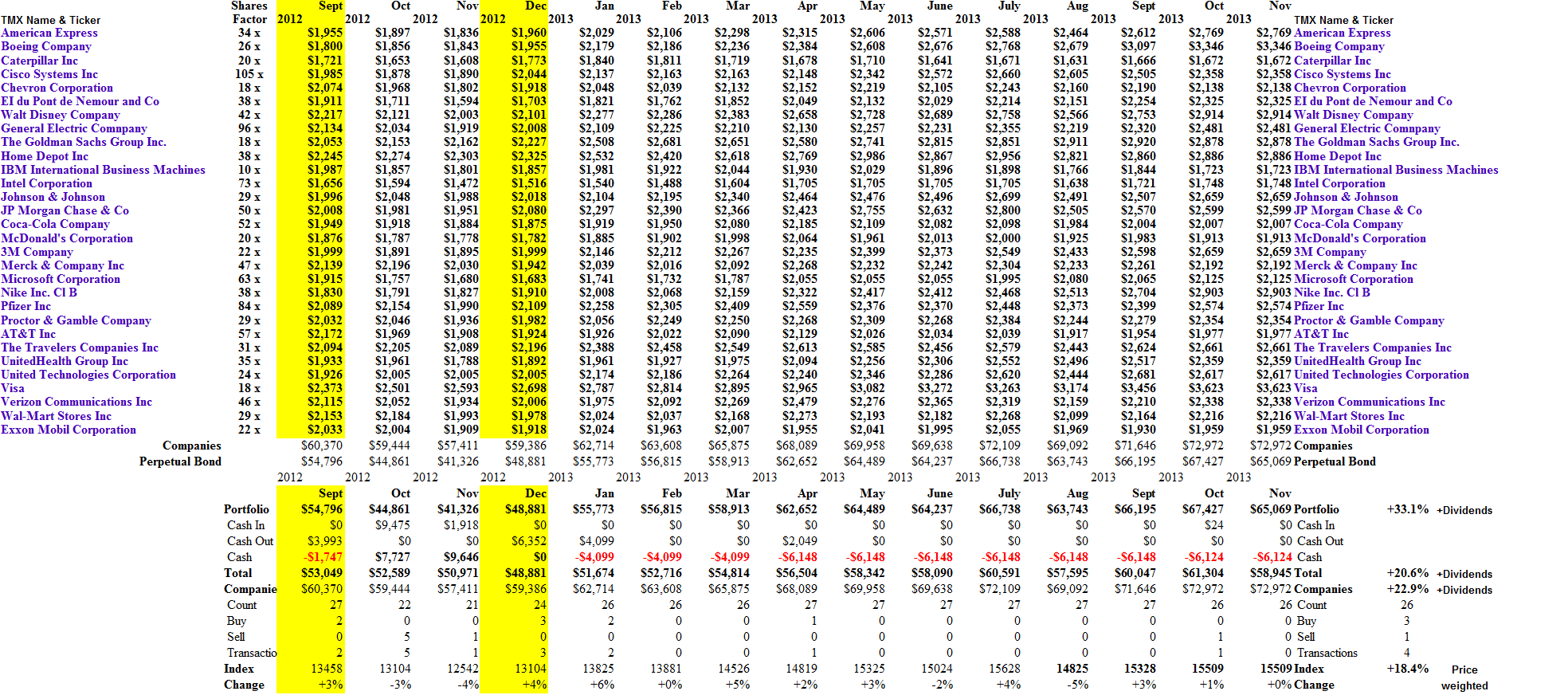

Exhibit 2: (B)(N) Dow Jones Industrial Companies – Prices & Portfolio – November 2013

The Dow Jones Industrial Companies – Prices & Portfolio – November 2013

(Please Click on the Chart to make it larger if required.)

Exhibit 3: (B)(N) Dow Jones Industrial Companies – Portfolio & Cash Flow Summary – November 2013

The Dow Jones Industrial Companies – Portfolio & Cash Flow – November 2013

(Please Click on the Chart to make it larger and again if required.)

For more information on the Chart Elements, please see our recent Post, The RiskWerk Company Glossary.

For more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.