The Flat World of Investing

Drama. Investing has been taken off the table as investors worldwide are waiting (it is said) for a new word on “tighter money” – that is, higher rates and less easing in government securities in the U.S., Japan, the U.K. and Europe (The Street, June 13, 2013, The Investment World Is Flat).

No Good, DOA & 0% unless it’s stolen, spent, or invested.

It’s a problem because “money” as “cash” is just no good and absent the spin, what are we supposed to do all day on Wall Street when the rent is due?

It’s also a problem because absent the spin, there’s far more money as cash than there are investments to buy if we can’t find enough that are “as good as cash” and “better than money”; that is, investments that are likely to obtain a non-negative real rate of return.

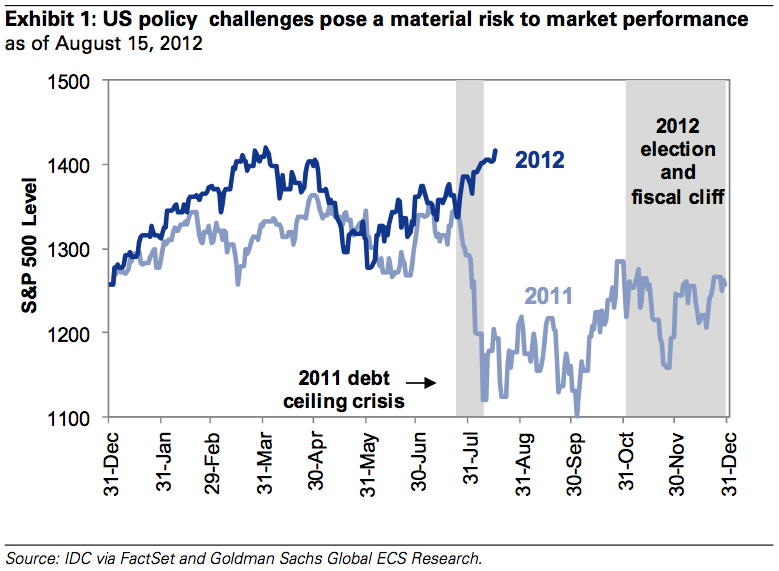

Debt Ceiling Fiscal Cliff 2012

Courtesy: Goldman Sachs

We understand the problem, of course, because if we are getting 50 basis points on $1 trillion guaranteed and the rate “jumps” to 75 basis points, we’ve just lost 50% of our return – poof, $2.5 billion in cash, gone in a twinkling of an eye.

But we have averted the worst excesses of the “fiscal cliff” and poured our money into the markets (which now stands at 1600 and not 1200 and is off the Chart), and we have drawn in any idle cash that was still out there, and now we’re faced – absent the spin – with the very real problem of investing our money; that is, of obtaining a non-negative real rate of return, other than by accident or by investment prowess reserved for the few, and at the end of day, reserved to mere 100’s of billions which is not nearly enough for the trillions of our otherwise idle cash.

But there are only three of those: Real Return Bonds (RRBs) or Treasury Inflation Protected Securities (TIPS) or The RiskWerk Company. Anything else is just a gamble.

To get involved with the trillions, absent risk-on/risk-off, we really need to look at the companies, and not just a few, or a few dozen, but hundreds of them. And for that, we need The Wall Street Put.

And what could have been bought for a mere $12 trillion in early April will now set you back $12.3 trillion or +2.4% more or +240 basis points, already. And it won’t get any cheaper. Please see Exhibit 1 below.

Exhibit 1: The Wall Street Put – March through June 2013

The Wall Street Put – March Through June 2013

The portfolio has hardly changed; there was some stop/loss selling but all of those companies are still (B) and so we bought them back at lower prices. The only company that is no longer in the portfolio is Primaris Retail REIT which was sold to KingSett et al.

(Please Click on the Chart to make it larger if required.)

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.