(B)(N) BRK-B Berkshire Hathaway Incorporated Class B

Drama. Mr. Warren Buffett has been at the helm of the investment company, Berkshire Hathaway Incorporated, since its inception in 1962 when Mr. Buffett bought control and ownership of the merger of the historic 19th century Berkshire Fine Spinning Associates and the Hathaway Manufacturing Company of New Bedford, Massachusetts.

What was then worth a few 10’s of millions, say three, is now worth about 26,800 10’s of millions, or $268 billion in round numbers. The company is often in the news (please see our earlier Post, (B)(N) GS The Goldman Sachs Group Incorporated, March 2013, in which Mr. Buffett was paid by the shareholders to acquire a 2% interest in the bank for free and worth about $1.3 billion) and is in the news today because of its +51% gains in profit over the last three months (Reuters, May 3, 2013, Insurance Gains Help Push Profit at Berkshire Hathaway Up Nearly 51 %).

The market value of the company is $268 billion and divided between the “lower priced” Class B shares of which there are about 1.1 billion trading at $109 ($122 billion) and the Class A shares of which there are less than a million (892,657 shares) trading at $163,000 ($146 billion) today in small volumes of four to five hundred shares even with today’s announcement, whereas about 45,000 Class B shares will change hands on a typical day.

A Class A share can always be converted to 1,500 Class B shares, but 10,000 Class B shares are required in order to obtain the voting rights of one Class A share, and there are no conversions the other way around; that is, 1,500 Class B shares cannot be converted to one Class A share other than by buying it for a similar price (please see the Memo from Mr. Buffett, updated July 3, 2003, but reproduced below prior to the 50:1 split of the Class B common shares in 2010, so that 30 becomes 1,500 and 1/200th becomes 1/10,000th after the split; the Memo also provides a valuable insight into investment thinking and risk management) and about 1,500 of them ($163,000/$109 = 1,495) would need to be sold in order to buy one Class A share. Neither class of shares receives a dividend and we understand that a $0.10 per share dividend was paid only once, in 1967, on the Class A stock for $90,000 in total.

On the other hand, Mr. Buffett is careful to assure that the companies in which he has an investment interest (almost all of which are for a very long time) pay dividends; for example, just five of his long term holdings are expected to pay aggregate dividends of $17.5 billion this year: Coca-Cola $4.9 billion, IBM $4.2 billion, Wells Fargo $6.3 billion, American Express $1 billion, and Goldman Sachs $900 million. But the Berkshire Hathaway shareholders can only make money by buying and selling the stock to each other, or selling them to new investors who then become shareholders.

For example, 1,500 Class B shares can be bought today for $162,960 at $108.64 per share, whereas one Class A share can be bought or sold for $162,904 or converted to 1,500 Class B shares; that means that a Class A shareholder can derive an instant profit of only $56 by converting one of their Class A shares to 1,500 Class B shares and selling them at the market price (but not net of the transaction fees or the time that it requires to affect the conversion and sale); if we want to buy 1,500 shares of the Class B stock, then we should think about buying just one share of the Class A stock.

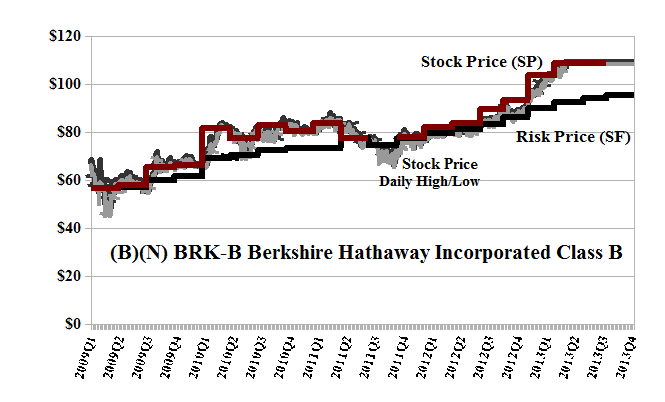

With reference to Exhibit 1 below, the Class B stock entered the Perpetual Bond™ at much lower prices of $60 in 2009 (Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason) but we were sold out on a stop/loss at $85 two years later and bought it back at $78 to $80 in late 2011 and have held it ever since.

Our estimate of the downside volatility is minus ($7.50) which is rather high for the $110 stock and reflects the price increase of $30 or nearly +50% in the past year. The September put at $105 can be bought for $2.70 today and the cost of that can be offset by a sold or short call against our long position at $110 for $3.45, so that we could be paid $0.75 per share today ($2.70 less $3.45) for holding the stock between $105 and $110 for the next five months; or, we could sell the call at a strike price $115 and be paid only $1.50 for it, so that for a net cost of $1.20 today ($2.70 less $1.50), we could hold the stock for between $105 and $115 for the next five months, absent working the options upward and forward as the summer unfolds.

Exhibit 1: (B)(N) BRK-B Berkshire Hathaway Incorporated Class B – Risk Price Chart

(B)(N) BRK-B Berkshire Hathaway Incorporated Class B

Berkshire Hathaway Incorporated is a publicly owned investment manager. Through its subsidiaries, the firm primarily engages in the insurance and reinsurance of property and casualty risks business. Berkshire Hathaway was founded in 1889 and is based in Omaha, Nebraska.

(Please Click on the Chart to make it larger if required.)

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory; and for our view of the current markets, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013. For a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

From the Desk of Mr. Buffett:

BERKSHIRE HATHAWAY INC.

1440 KIEWIT PLAZA

OMAHA, NEBRASKA 68131

WARREN E. BUFFETT, CHAIRMAN

Memo

From: Warren Buffett

Subject: Comparative Rights and Relative Prices of Berkshire Class A and Class B Stock

Date: February 2, 1999 Updated July 3, 2003

Comparison of Berkshire Hathaway Inc. Class A and Class B Common Stock

Berkshire Hathaway Inc. has two classes of common stock designated Class A and Class B. A share of Class B common stock has the rights of 1/30th of a share of Class A common stock except that a Class B share has 1/200th of the voting rights of a Class A share (rather than 1/30th of the vote). Each share of a Class A common stock is convertible at any time, at the holder’s option, into 30 shares of Class B common stock. This conversion privilege does not extend in the opposite direction. That is, holders of Class B shares are not able to convert them into Class A shares. Both Class A & B shareholders are entitled to attend the Berkshire Hathaway Annual Meeting which is held the first Saturday in May.

The Relative Prices of Berkshire Class A and Class B Stock

The Class B can never sell for anything more than a tiny fraction above 1/30th of the price of A. When it rises above 1/30th, arbitrage takes place in which someone – perhaps the NYSE specialist – buys the A and converts it into B. This pushes the prices back into a 1:30 ratio.

On the other hand, the B can sell for less than 1/30th the price of the A since conversion doesn’t go in the reverse direction. All of this was spelled out in the prospectus that accompanied the issuance of the Class B.

When there is more demand for the B (relative to supply) than for the A, the B will sell at roughly 1/30th of the price of A. When there’s a lesser demand, it will fall to a discount.

In my opinion, most of the time, the demand for the B will be such that it will trade at about 1/30th of the price of the A. However, from time to time, a different supply-demand situation will prevail and the B will sell at some discount. In my opinion, again, when the B is at a discount of more than say, 2%, it offers a better buy than the A. When the two are at parity, however, anyone wishing to buy 30 or more B should consider buying A instead.

Source: www.berkshirehathaway.com

From the Desk of The RiskWerk Company: Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.