Pension Envy

Drama. The large public pension funds appear to be preoccupied with executive salaries and benefits, and sometimes business, but are recently cloaked in governance issues and righteous, public, indignation over the seemingly high salaries, bonuses, and benefits that are being paid and renewed for the executives of the companies that they’ve invested in that have failed to deliver the returns that they need in order to pay out the benefits to their members that they promised to deliver, and vaguely, need to deliver, in order to keep and renew their jobs and multi-million dollar benefits, perks, and no risk salaries, one would think.

It’s tiresome and transparent and, in our view, the pension plan managers have no place in the Boardrooms of the Nation. It’s just noise and bread and circuses for their constituency, and helps neither the business that they’ve bought into as an investment with our money at their choice, nor their investment performance. What we need is more prowess on their battlefield – the investment arena – where it counts for us, and for which they were hired anonymously by another board to which they are responsible. Please see our recent Post, Bystanders & Collateral Damage, April 2013.

But, they say, “Jack” was there and he did it or didn’t; it was he who failed – how could we know? Well, they can know, and they are responsible for not knowing because they are the “investors” – they are charged to keep our money safe and to obtain a reasonably hopeful and provable return above the rate of inflation – and they are not the managers of the companies that are supposed to deliver those returns, for them, and every other shareholder of the company for whom they do not speak. Which includes us.

A number of easy examples come to mind; RIM Research In Motion, Apple Incorporated, Dell Incorporated, Hewlett-Packard, Sino-Forest, Yellow Media, Barrick Gold Corporation, Air Canada, Cliffs Natural Resources (“Ring of Fire”); hedge funds of all sorts that are colorful and promising when they’re sold, but are now being sued for fraud or malfeasance to recover dignity(sic) in the Courts for the money that can’t be recovered; and just about every second company that we’ve talked about in these Posts because we try to balance the good news, and what can be done, with the bad – and this is one of the “bad” news. For the “good” news, please see our recent Post on Berkshire Hathaway, (B)(N) BRK-B Berkshire Hathaway Incorporated Class B, May 2013.

Now comes the Occidental Petroleum Corporation (The Associated Press, May 4, 2013, Shareholders Oust Occidental Chairman) and Lululemon Athletica Incorporated (The Associated Press, May 4, 2013, Retirement Fund Sues Lululemon). Please see Exhibit 1 and 2 below.

The California State Teachers’ Retirement System, and 75% of the other shareholders, called the Chairman’s compensation for thirty years of his time “a waste of shareholder money” and have gone on to elect another board member since 1996 – only seventeen years – as the interim chairman, pending an executive search.

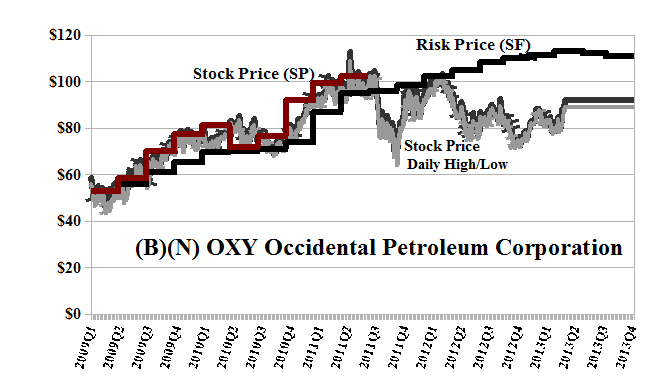

Under Mr. Irani’s leadership of thirty years, Occidental grew to become the fourth-largest U.S.-based oil company and its stock market value was $9 billion at $8 per share in 2000 and is $73 billion and $90 per share now. The company became eligible for the Perpetual Bond™ in 2009 at $50 and we sold the last of holdings at $100 two years later, and haven’t owned it since. Please see Exhibit 1 below. We buy and hold a stock only if the ambient stock prices summarized by the Red Line Stock Price (SP) tend to be above the Black Line Risk Price (SF), and for no other reason, with our usual “selling discipline” in force and effective. Please see almost any of the (B)(N)-posts for more detailed examples of the “selling discipline”.

We did, however, fail to buy it at the low, low prices of $80 in 2011, and at $80 or less four or five times since then, suspecting that there might be issues of “capital safety” and problems that the company could work through but which the stock market couldn’t. We tend to leave a lot of money on the table because it’s not really ours, yet. Please see our Post, Bystanders & Collateral Damage, April 2013.

Occidental will pay $2 billion of dividends to its shareholders this year, for a current yield of 2.8% that is well above the bond rate (1% or less) that the pension funds are used to, but, alas, we’re still not buying it right now because it’s trading below the Risk Price (SF) of $110 and our estimate of the downside volatility in the stock price is minus ($5), which is ±7% of the stock price and expensive to protect.

Exhibit 1: (B)(N) OXY Occidental Petroleum Corporation – Risk Price Chart

(B)(N) OXY Occidental Petroleum Corporation

Occidental Petroleum Corporation engages in the exploration and production of oil and gas properties in the United States and internationally.

(Please Click on the Chart to make it larger if required.)

From the Company: The Oil and Gas segment explores for, develops, and produces oil and condensate, natural gas liquids (NGLs), and natural gas. Its domestic oil and gas operations are located in California, Colorado, Kansas, Montana, New Mexico, North Dakota, Oklahoma, Texas, and West Virginia; and international oil and gas operations are located in Bahrain, Bolivia, Colombia, Iraq, Libya, Oman, Qatar, the United Arab Emirates, and Yemen. The Chemical segment manufactures and markets basic chemicals, including chlorine, caustic soda, chlorinated organics, potassium chemicals, chlorinated isocyanurates, sodium silicates, calcium chloride, and ethylene dichloride products; vinyls comprising vinyl chloride monomer and polyvinyl chloride; and other chemicals, such as resorcinol. The Midstream, Marketing and Other segment gathers, processes, transports, stores, purchases, and markets oil, condensate, NGLs, natural gas, and carbon dioxide. This segment also trades around its assets consisting of transportation and storage capacity, as well as oil, NGLs, gas, and other commodities, and is involved in the power generation activities. The company was founded in 1920 and is headquartered in Los Angeles, California.

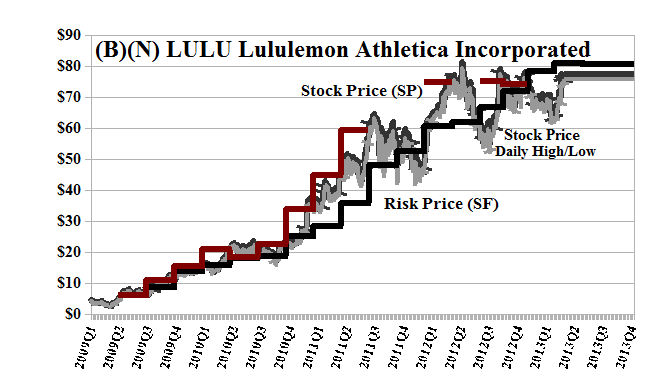

And now we must deal with Lululemon Athletica more proactively than in the case of “Hallandale Beach (Florida) Police Officers and Firefighters’ Personnel Retirement Fund vs Lululemon Athletica Incorporated” which is suing Lululemon Athletica Incorporated of Vancouver, British Columbia, and taking issue (but no grounds) with the decision of Lululemon’s compensation committee to boost the maximum payout of the executive bonus plan before a $60 million recall of its “yoga pants”. With respect to the complaint, we note only that Lululemon’s sales are expected to be $1.3 billion this year, or more than $60 million every two days, and that other instances of a “wardrobe failure”, when seen in the proper light, have created celebrity status which might be good for this elite brand-name producer of athletic apparel and has already led to “material” design changes.

Lululemon does not pay a dividend but was in the Perpetual Bond™ between $10 in 2009 and $60 two years later, and not since with any conviction although the stock price is up by +10% this year and +50% year-over-year which is undoubtedly a lot more than what the Plaintiff got last year, and likely this year absent more surprises. Please see Exhibit 2 below.

Exhibit 2: (B)(N) LULU Lululemon Athletica Incorporated – Risk Price Chart

(B)(N) LULU Lululemon Athletica Incorporated

Lululemon Athletica Incorporated and its subsidiaries, design, manufacture, and distribute athletic apparel and accessories for women, men, and female youth.

(Please Click on the Chart to make it larger if required.)

From the Company: The company’s line of apparel include fitness pants, shorts, tops, and jackets for healthy lifestyle activities, such as yoga, running, and general fitness. Its fitness-related accessories comprise bags, socks, underwear, yoga mats, instructional yoga DVDs, and water bottles. The company sells its products through a chain of corporate-owned and operated stores; direct to consumer through e-commerce Websites; and a network of wholesale channel, such as premium yoga studios, health clubs, and fitness centers. As of February 3, 2013, it operated 135 stores in the United States, 51 stores in Canada, 23 stores in Australia, and 2 stores in New Zealand under the lululemon athletica and ivivva athletica brand names. Lululemon Athletica Incorporated was founded in 1998 and is based in Vancouver, Canada.

Pension Envy

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory; and for our view of the current markets, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013. For a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.