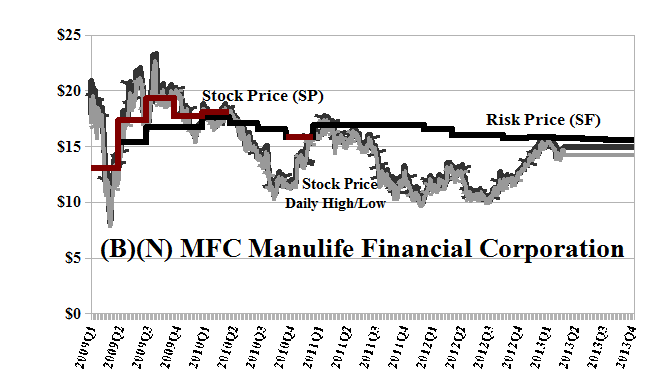

(B)(N) MFC Manulife Financial Corporation

Drama. The profit of Manulife Financial Corporation, Canada’s largest life insurance company and one of its largest “wealth managers” with about $600 billion of assets under management, dropped 56% in the first quarter of this year over a year earlier, and the company expects no improvement for the rest of the year and, it says, has “hedged much of its exposure to both stock markets and bond yields” (Reuters, May 2, 2013, Manulife, Great-West profits meet expectations, shares up).

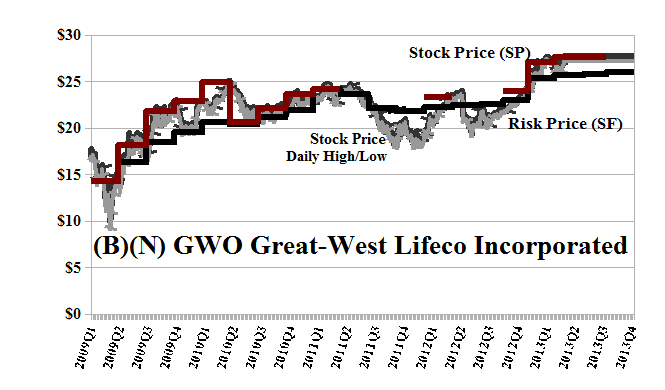

Defying the gravity of the situation, the stock price rose by about +6% to the current $15 to $16 on a volume of about six million shares which is two to three times the normal daily volume. Moreover, the stock price is up from $10 a year ago, but still well below $35 in 2008, and still not enough to qualify the stock for inclusion in the Perpetual Bond™ (please see Exhibit 1 below). On the other hand, Great-West Lifeco, Canada’s second largest life insurance company and also a substantial “wealth manager” with about $600 billion under management, posted a profit increase of +15% quarter over quarter, and the stock price increased by about +2% to the current $28 and it has been in the Perpetual Bond™ since much lower prices of $23 to $24 late last year.

These look like “random” results, but they’re not because investors, sensibly, tend to focus on what they call the “core earnings” which are policy- and business-related to the insurance products that they offer, rather on the “enhanced earnings” which are moderated by the investment returns that an insurer can obtain in the bond and equity markets on the managed funds, some of which are their own (ibid, Reuters).

But the cost of offering insurance products, and the price at which they can be sold, affects their competitive position, and an insurance company – like anyone else – can only afford to lose money or obtain low returns in the bond and equity markets for so long, after which they have to be acquired by someone with still deeper pockets, and the insurance companies have had the same complaint for years (Reuters, August 10, 2010, Manulife, Sun Life results hit by weak markets).

And now, they can’t seem to make money – or are loathe or afraid to make money using hedges, “belts” and “braces” – even in up markets, because they might be called upon to do it again and support the products that they’ve already sold without becoming bankrupt or insolvent, or under regulatory pressure. The Government is the insurance company of last resort, as it is today for many, and reportedly, almost all, pensioners who have had similar problems – insufficient assets to meet obligations or liabilities, or even a living – with dependence on the markets.

In the meantime, Manulife is paying a dividend of $0.13 per share per quarter for a total payout of $950 million per year to its shareholders and a current yield of 3.5%; and, equally generously, Great-West Lifeco is paying a dividend of $0.30 per share per quarter for a total payout of $1.1 billion per year to its shareholders and an even higher current yield of 4.5%.

How do they do that if profits are unreliable and the market is flat, as far as they’re concerned?

Well, the stock float for Manulife has increased by +20% from 1,510 million shares in 2009 to 1,830 million shares today; so that means that roughly 320 million new shares have come out of treasury with no par value – like printing “money” – and if they were sold at prices between $10 and $15 over the last several years, then the investors have, in fact, been paying themselves their own dividends, and taxes, at a great yield with their own money.

And similarly, the stock float of Great-West Lifeco has increased by +20% from 760 million shares to the current 950 million shares, or 190 million new shares issued at prices of between $20 and $25 per share and worth (in round numbers) $4 billion of new money.

In effect, both Manulife and the Great-West Lifeco, are living beyond their means – and might not have any choice in the matter – and if things don’t get better soon, “better markets”, “better bond yields”, they might soon expect a debit balance. One would think that they could really use some “better technology” to help them with their “better sales”. Please see below.

Exhibit 1: (B)(N) MFC Manulife Financial Corporation – Risk Price Chart

(B)(N) MFC Manulife Financial Corporation

Manulife Financial Corporation together with its subsidiaries, provides financial protection and wealth management products and services to individuals and group customers primarily in Asia, Canada, and the United States.

(Please Click on the Chart to make it larger if required.)

From the Company: Manulife Financial is a leading Canada-based financial services group with principal operations in Asia, Canada and the United States. Clients look to Manulife for strong, reliable, trustworthy and forward-thinking solutions for their most significant financial decisions. Our international network of employees, agents and distribution partners offers financial protection and wealth management products and services to millions of clients. We also provide asset management services to institutional customers. Funds under management by Manulife Financial and its subsidiaries were US$547 billion as at March 31, 2013 and the Company operates as Manulife Financial in Canada and Asia, and primarily as John Hancock in the United States.

Exhibit 2: (B)(N) GWO Great-West Lifeco Incorporated – Risk Price Chart

(B)(N) GWO Great-West Lifeco Incorporated

Great-West Lifeco Incorporated is an international financial services holding company with interests in life insurance, health insurance, retirement and investment services, asset management and reinsurance businesses.

(Please Click on the Chart to make it larger if required.)

From the Company: Great-West Lifeco has operations in Canada, the United States, Europe and Asia through The Great-West Life Assurance Company, London Life Insurance Company, The Canada Life Assurance Company, Great-West Life & Annuity Insurance Company and Putnam Investments, LLC. Great-West Lifeco and its companies have $582 billion in assets under administration and are members of the Power Financial Corporation group of companies.

And For Better Technology: Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, or, more lightly, Bystanders & Collateral Damage, April 2013, for more details; and for how we see the current market, The Wall Street Put, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.