The Consumer Reports For Socks & Stocks

Drama. It’s anecdotal but often observed that economists and professional money managers tend to put their money into bonds and, of those, government bonds are preferred because the capital safety is 100% – we will always get our money back – even if it is somewhat depreciated, because, in general, the government bond rate is needy and will tend to lag the rate of inflation, and there would be an inquiry if it were otherwise.

Moreover, the banks, insurance companies, and pension funds will buy corporate bonds only through the elaborate and expensive system of ratings provided by the ratings services such as Fitch, Standard & Poors, and The Dow Jones Company; and the prices of the bonds are graded accordingly in a system that the professional money managers cling to, credible or not, because it greases the wheels, and what else could they have done?

However, there is no “rating system” for equities. And the only rating system that is meaningful and provably has the same or better authority than a government bond or well-rated corporate bond, is the “price of risk” (and, in fact, the same measure is correct for investments of all types).

At the price of risk, an equity is “as good as cash” and “better than money” and the price of risk between companies is as comparable as one foreign exchange rate might be to another, when traded as stocks, and that is all that we can hope for in our government bonds and bargain for within “the demonstrated societal standards of risk aversion and bargaining practice” which is the “common currency” and “numeraire” of the matter (please see the references below).

Courtesy: Paladin Socks Ability Superstore UK

And whereas the economists and professional money managers are likely to pour over the Consumer Reports™ before buying a new car or a pair of socks (please see our Post, (B)(N) JCP J.C. Penney Company Incorporated, April 2013), they are willing to cast our money in mutual funds and pension funds, and into the Wind with a reckless abandon and, as the economist John Maynard Keynes observed in 1935, as “slaves to some defunct economist” and now, “fashion”.

Please see our Post, The S&P TSX “Hangdog” Market, May 2013, and the references therein, as well as, The Yale Method, May 2013, for additional background or, in this context, the “shorts” of the matter.

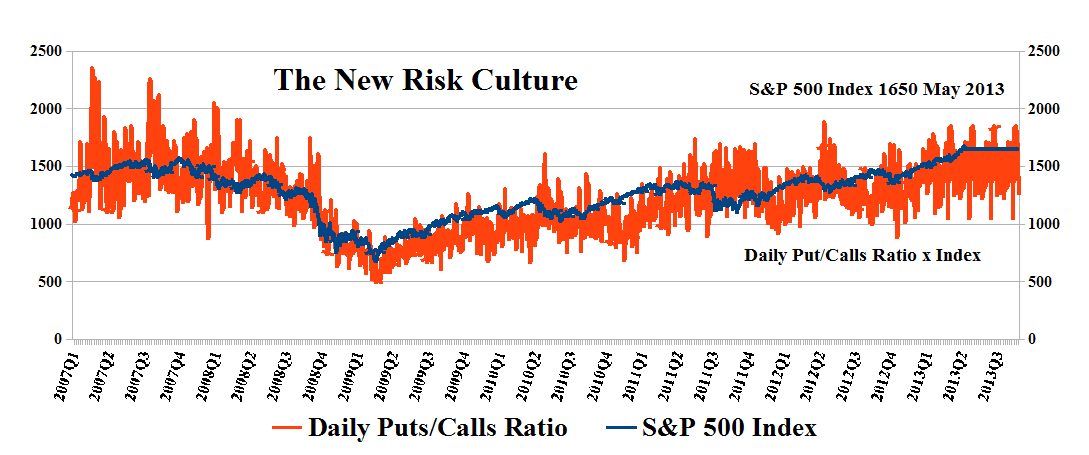

What Keynes said in 1935 is no less true today as the S&P 500 Index continues to soar, but the ratio of put contracts, effecting “price protection”, to call contracts, effecting the hope of lower prices to obtain higher priced goods, continues (on balance) to fall and the latter (calls) outruns the former (puts) and drags the ratio downwards. Please see Exhibit 1 below.

Exhibit 1: The New Risk Culture – The End Is Nigh When The Ratio Tilts To High

The New Risk Culture Data: CBOE Chicago Board Options Exchange

(Please Click on the Chart to make it larger if required.)

One sees from the Chart that the predilection of the professional money managers who ran our money before 2008, was that the market was going down as they bought more put contracts than call contracts – and they were not disappointed, but it took a long time to recover from that “joy” – 2009 through 2010 and the early parts of 2011, when we begin to see more aggressive call buying over put buying at the market low in the 3rd quarter of 2011, but not the year before, in 2010.

How does that end? Well, it ends in disappointment should the Feds Rate rise and declare an end to easy money, and the beginning of better bond rates and an appreciation of inflation, as the tide goes out (Buffett); and it’s an ill-wind that’s blowing, so to speak, as the elite investors allegedly “flee to safety”.

We might know that the end is nigh when the ratio tilts to high, and begins to rise again, absent a “surprise”. Although we also note that the professional fund managers tend to be too early, or too late; best to be always ready – 100% Capital Safety and a real policy of “risk aversion”.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.