(B)(N) MRO Marathon Oil Corporation

Drama. The Canadian Oil Patch continues to go begging as the Marathon Oil Corporation has failed to find a buyer for its 20% interest in the Athabasca Oil Sands Project with Shell Canada Energy (60%) which is the operator and Chevron Canada Limited (20%) (The Associated Press, May 23, 2013, Marathon Oil: talks tied to sale of part of stake in Athabasca Oil Project have ended and our previous Post, Black Gold in The Canadian Oil Patch, April 2013)

Athabasca Oil Sands Project

It’s evident that oil sands have become an “ugly duckling” as the “oil crisis” has waned, and the issue of who is going to clean-up the mess is far from resolved and will shadow any sales of these properties, as would a run-down or fully depreciated property depress the sale price, absent some new discovery of a use or “hidden value” for the debris by a hedge fund.

Revenue Canada has suggested that the cleanup costs should be treated as a “mortgage” during the sale of resource properties and added to the taxable sale costs, but has been overruled by the Canadian Supreme Court in a recent Court decision affecting the Japanese forestry company, Daishowa-Marubeni International Limited (The Canadian Press, May 23, 2013, Can’t tax reforestation, top court rules; case could affect oil, gas transfers).

The Alberta Government supported the company’s petition and argued that the obligation to reforest was embedded in the timber rights granted by the province. Indeed. But who will buy the mineral rights to depleted oil sands?

The Marathon Oil Corporation has most recently been in the Perpetual Bond™ since $30 early last year (please see Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason) but to keep it in has required some agressive maintenance, including an active put at $34 as the price plummeted to $25 in May of last year.

The indicated downside due to price volatility remains at minus (-$3) and we should not be surprised by any price between the current $35 and $32 or $38 in the next quarter. The current dividend is $0.17 per share per quarter for a payout of $120 million to the shareholders and a current yield of 1.9% which could, of course, be instantly erased should the stock price plummet again as the company continues to search for new ways in which to “maximize shareholder value”.

Or, we could do it for ourselves by buying the July put at $33 for $0.67 per share today and selling the July call at $37 for $0.75 today, and for a net cost of $35 to hold the stock and a small gain of $0.08 per share for the collar ($0.67 less $0.75), stay in the game at between $33 and $37 for the next several months, no matter what happens. Please see our recent Post, The S&P TSX “Hangdog” Market, May 2013, for a broader view of the active Canadian market.

Exhibit 1: (B)(N) MRO Marathon Oil Corporation – Risk Price Chart

(B)(N) MRO Marathon Oil Corporation

Marathon Oil Corporation is an integrated energy company with significant operations in the North America, Africa and Europe.

(Please Click on the Chart to make it larger if required.)

From the Company: Marathon Oil Corporation operates as an energy company worldwide. The companys Exploration and Production segment explores for, produces, and markets liquid hydrocarbons and natural gas in the United States, Angola, Canada, Equatorial Guinea, Ethiopia, Gabon, Kurdistan Region of Iraq, Libya, Norway, Poland, and the United Kingdom. Its Oil Sands Mining segment mines, extracts, and transports bitumen from oil sands deposits in Alberta, Canada; and upgrades the bitumen to produce and market synthetic crude oil and vacuum gas oil. As of December 31, 2012, this segment had rights to participate in developed and undeveloped leases totaling approximately 43,000 net acres. The company was formerly known as USX Corporation and changed its name to Marathon Oil Corporation in July 2001. Marathon Oil Corporation was founded in 1887 and is headquartered in Houston, Texas.

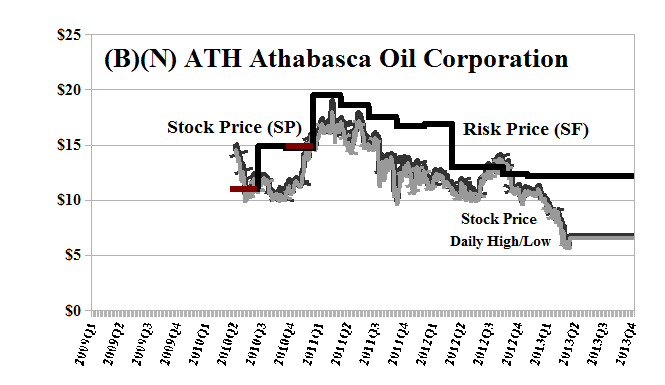

Exhibit 2: (B)(N) ATH Athabasca Oil Corporation – Risk Price Chart

Athabasca Oil Corp formerly Athabasca Oil Sands Corp is in business to explore for, sustainably develop and produce bitumen and oil and gas assets in Alberta, Canada.

(Please Click on the Chart to make it larger if required.)

From the Company: Athabasca Oil Corporation engages in the exploration, development, and production of thermal and light oil resource plays in the Western Canadian Sedimentary Basin in Alberta, Canada. Its Thermal Oil division produces bitumen from sand and carbonate rock formations located in the Athabasca region of northeastern Alberta. This divisions principal oil sands assets include Hangingstone, Dover West, Dover, Birch, and Grosmont projects. The companys Light Oil division produces light oil, natural gas, and natural gas liquids located in various regions of the northwestern Alberta. This divisions primary light oil development areas comprise Kaybob and Saxon/Placid with formation targets consisting of the Duvernay, Montney, Charlie Lake, Nordegg, Slave Point, and Muskwain northwestern Alberta. As of December 31, 2012, it held approximately 4.4 million net acres of mineral resource leases and permits, which include approximately 1.5 million net acres of oil sands leases and permits in the Athabasca region of northeastern Alberta and approximately 2.8 million net acres of petroleum and natural gas leases in northwestern Alberta. The company was formerly known as Athabasca Oil Sands Corp. and changed its name to Athabasca Oil Corporation in May 2012. Athabasca Oil Corporation was founded in 2006 and is headquartered in Calgary,

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

Hello there! I know this is kinda off topic however I’d figured I’d ask.

Would you be interested in trading links or

maybe guest writing a blog article or vice-versa?

My blog addresses a lot of the same topics as yours and

I believe we could greatly benefit from each other. If you’re interested feel free to shoot me an e-mail. I look forward to hearing from you! Awesome blog by the way!

LikeLike

http://tandtand.wordpress.com/2011/12/

Is that you? It’s in Danish and Inci-Dental, I guess? Best regards, Ernst.

LikeLike