(B)(N) The Easy (EC) Theory of the NASDAQ

Das Kapital by Karl Marx, 1867.

Drama. Karl Marx (1818-1883) was an economist and a serious player in the stock market, but the word “serious” really applies only to his losses, which he tried to cover by writing sensational books and pamphlets on “economics” – which he detested – but which also turned out to be seriously off-the-mark, and his theories have never worked in the industrial British and German economies for which they were intended, but they became a sensation with millions of people who didn’t understand them, or couldn’t read, but were anxious to “cast-off their chains”, which (indeed) were “binding” and far from “designer” at the time.

Our approach is more direct – we just buy and hold stocks that tend not to lose money and that meet our simple criteria – we want 100% capital safety and 100% liquidity and a hopeful but not necessarily guaranteed return above the rate of inflation, which, if we don’t get it, is just another way of losing our money.

In contrast, the prevailing economic theories of the stock market pursue a policy of losing money in order to pro-actively avoid the much smaller daily loses that are due to ambient volatility, but which cannot be avoided because that’s how the market makes, or discovers, prices, and so, in the long term, they just track the market, which is to be expected, and demonstrates no insight, or added-value, despite the huge energies and trillions of dollars that are expended on it.

The Difference Engine

We are minded of Charles Babbage (19th century) who invented mechanical calculating machines which were called “analytical engines”, to wit “Mr. Babbage, if your machine is given the wrong question, does it provide the right answer? Yes.”

The “extended” NASDAQ includes the NASDAQ 100 and an assortment of newsworthy companies, but it is still a “dark and fabled place” for most investors who are looking for extraordinary gains which are “unearned”.

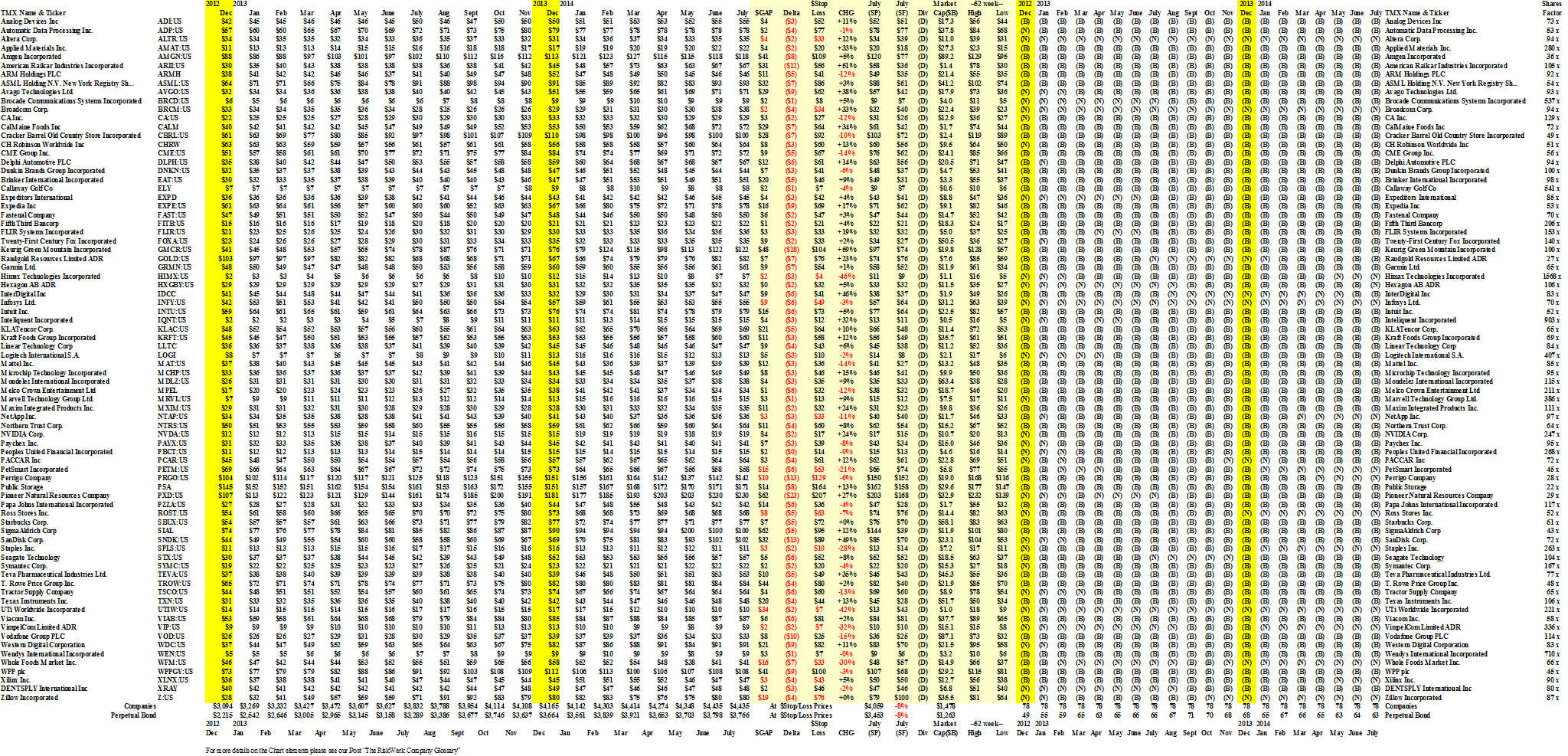

We cast our light there and developed a portfolio of the seventy-eight companies that had a market capitalization of less than $100 billion, paid dividends, and demonstrated adequate, and even excessive, financing in-place, which means that they have a modality for Company E or C, hence, “The Easy (EC) Theory of the NASDAQ”, which we also applied with remarkable success to the one hundred or so S&P TSX companies that meet those same criteria, within the constraint of more modest market capitalizations that are typical of the Canadian market.

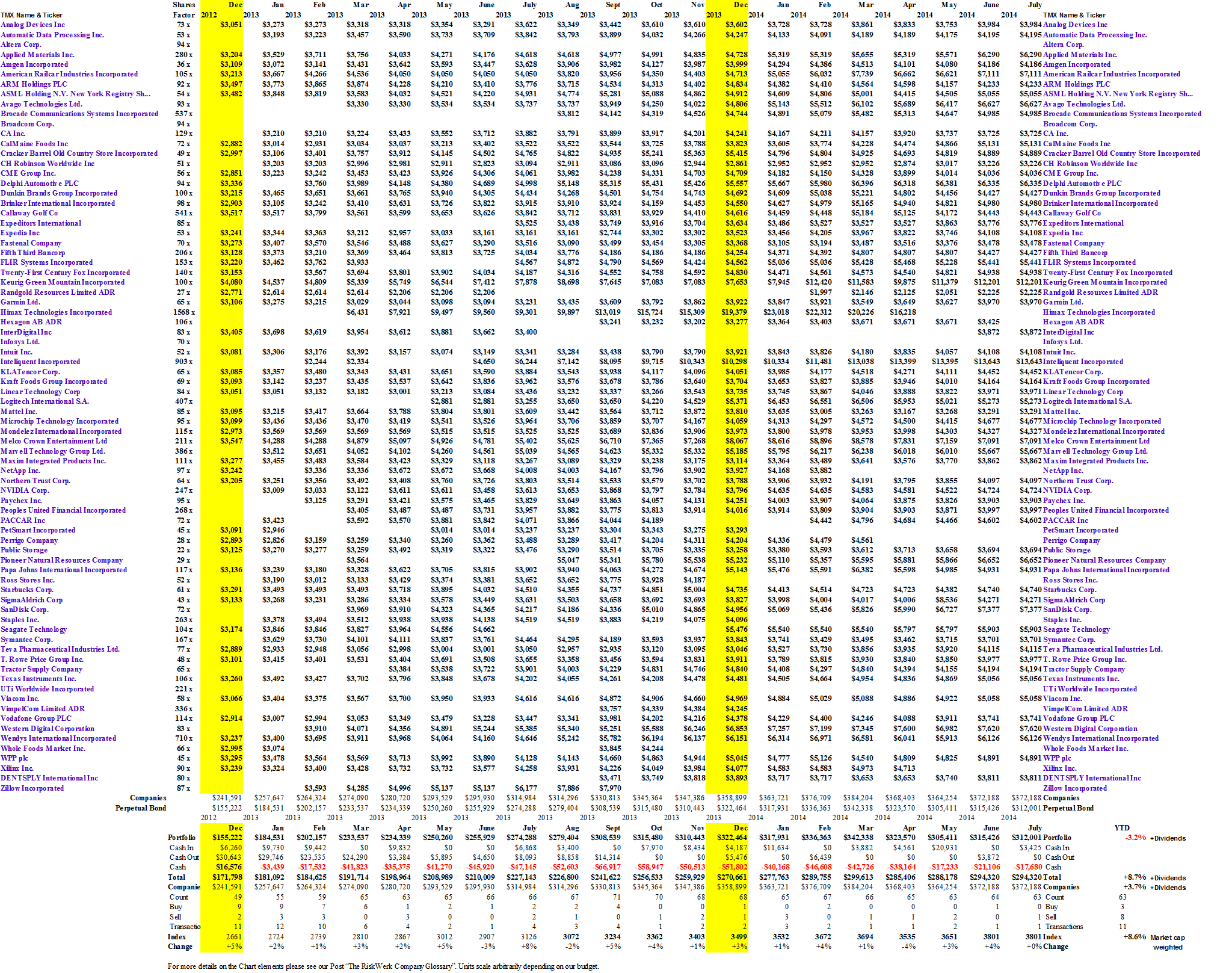

These companies, in aggregate, gained +37% last year and a further 3.5% so far this year, and they also paid $41.5 billion in dividends for a middling 27% return of earnings and an aggregate yield of 2.8%; but in the Perpetual Bond™, they were up a staggering +58% last year and have produced – or hung on to – a further +9% so far this year; please see Exhibit 1 below (and click on it, and again, to make it larger if required).

You didn’t build that on your own.

However, it’s not surprising that no matter how virtuous these companies are in terms of providing reliable dividends and conservative balance sheets, the stock prices don’t necessarily follow the “virtue”, and all that we can really expect from these portfolios is that they will follow the stop/loss, which breach is a “profit-making” opportunity for us because we will buy them back at lower prices if they are still trading above the price of risk, and that’s a more than adequate defence against a generally unfounded market angst, for which there is no cure – after all, it’s not the companies that make their stock prices, and the policy of rewarding managers for “good stock prices” is a delusion.

Exhibit 1: The Easy (EC) Theory of the NASDAQ

The Easy (EC) Theory of the NASDAQ – Fundamentals – June 2014

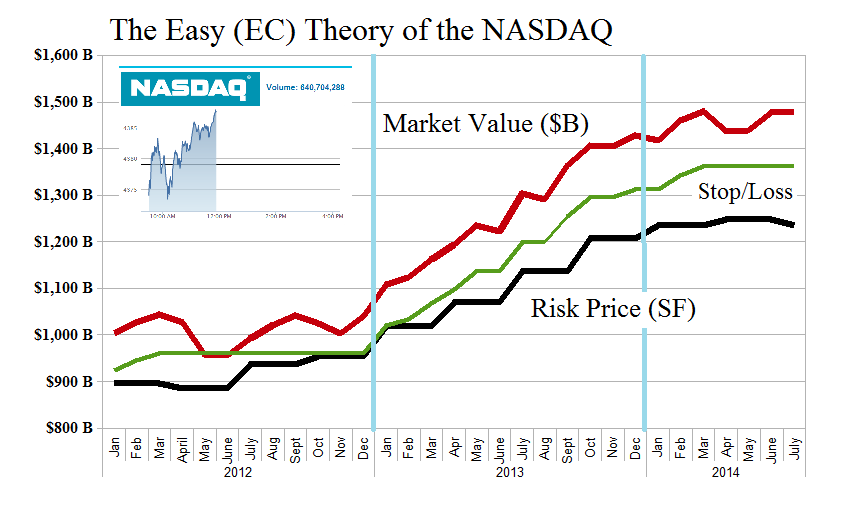

Figure 1.1: (B)(N) The Easy (EC) Theory of the NASDAQ – Risk Price Chart – June 2014

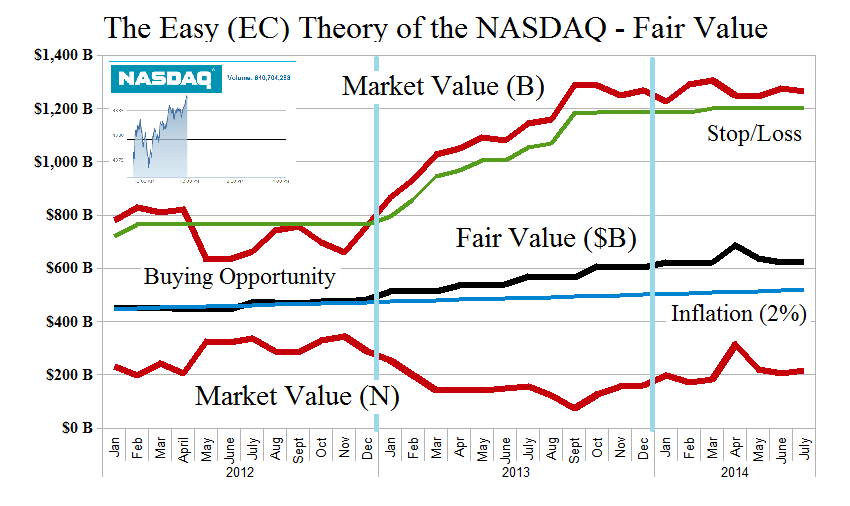

Figure 1.2: (B)(N) The Easy (EC) Theory of the NASDAQ – Fair Value – June 2014

The domain for this portfolio has 78 companies, each of which is an (EC); simply buying and holding the entire portfolio on an equal-weighted basis, produced +49% last year, plus a dividend yield of 2.8%, and obviously, there is no risk with a modest stop/loss policy in-place, which in the chart on the left, is 92% reflecting the demonstrated ambient quarterly volatility of minus (-8%), and if the prices are not rising, we’re still collecting dividends.

The Perpetual Bond™ is more aggressive because it respects more closely the price of risk; a company is in the portfolio if and only if it is trading at or above the price of risk, as shown in the portfolio “Market Value (B)” in Figure 1.2 on the left; it returned +58% last year, and required less money to implement.

Moreover, hitting the stop/loss creates buying opportunities at lower prices, so that, in principle, we’re earning more than the dividend rate when the market is, whatever, and trying to figure-out what it might do next – but we don’t really care what it does, because we’re always in the market, and the worst that can happen is that they’ll have to buy our stocks at higher prices. Oh well. We note also that there is no effective stop/loss policy on the N-companies, which could be trading at zero.

The “Fair Value” is the average of the (B)-companies at the price of risk and the (N)-companies at the price of risk (not the stock price) and it is based on the precept that the companies that are trading at or above the price of risk are “undervalued” because there is an excess demand for them over supply at the current stock prices; and the (N)-companies are “overvalued” because there is an excess supply of them over demand at the current stock prices.

Where’s the risk?

For more details, please click on the links (and again to make them larger if required) “(B)(N) The Easy (EC) Theory of the NASDAQ – Prices & Portfolio – June 2014” and “(B)(N) The Easy (EC) Theory of the NASDAQ – Portfolio & Cash Flow Summary – June 2014“.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}