(P&I) Bubblemania and The Working Poor

The Boggart Defense

Courtesy: Harry Potter and the Prisoner of Azkaban

Essay. The investment industry continues to create “spooks” and “phantoms” that just aren’t there unless we, as investors, embrace them, feed them, and give them flesh with our money (The Street, June 6, 2014, Bubble Risk With New Highs for Dow Industrials, Transports, S&P).

Figure 1: Smart Beta and The Boggart Defense

For example, apparently, 40% of investors, by “number” rather than “money managed” because there haven’t been any “smart returns” yet, who were surveyed in Europe and North America, have adopted “smart-beta” indexing strategies, a “new name” in bespoke investment management for want of a better name, they say, although we have a “charm” for it (Pensions & Investments, June 9, 2014, Smart Beta Supplement); please see Figure 1 on the left.

Figure 2: Long Term Capital Management 1994-1998 Exceedingly Alpha- and Beta-Smart – Not Safe, Not Liquid, and No Hope.

What’s missing are the three words – safe, liquid, and hopeful – none of which appear in this “powerful” and “new” investment strategy that is guaranteed to solve investment industry problems, but only add to ours. What will we say to the Board or to our investors? That “beta” was smarter than us, and costs a lot less, they say? And although we still don’t know anything about “alpha“, we didn’t lose all of your money, did we? Please see Figure 2 on the right for what it really means.

And the markets are “spooked” too, but we don’t pray for rain or “The Black Swan” to make it look like we’re needed, because we embrace these markets for what they are, whatever they are, and we know exactly where we are in them, and not out of them.

The compelling fact is that there’s far more money around than stocks to put it in, and money only has “value” when it’s “working”, and if it’s got nothing to work on, there’s going to be a vast transfer of money from the idle rich to the working poor.

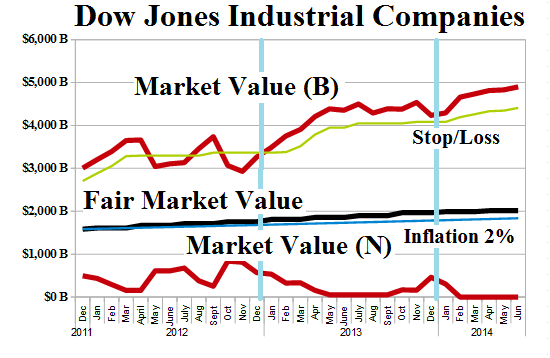

But our money in stocks is always working, and it only stops working when the dividend yield plus the price yield (which could be negative) is less than the rate of inflation; please see Exhibit 1 below for “money at work” for which our job is to make it work harder.

Exhibit 1: (B)(N) Major Markets At The Price of Risk

Figure 3: (B)(N) Dow Jones Industrial Companies – Risk Price Chart – June 2014

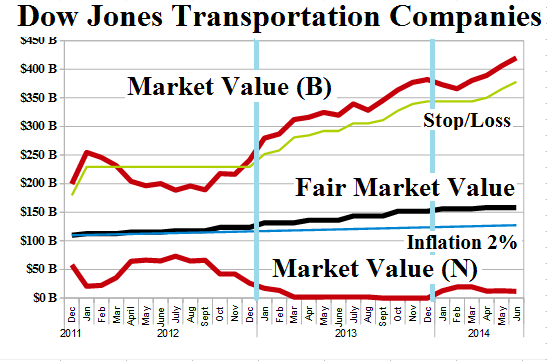

Figure 4: (B)(N) Dow Jones Transportation Companies – Risk Price Chart – June 2014

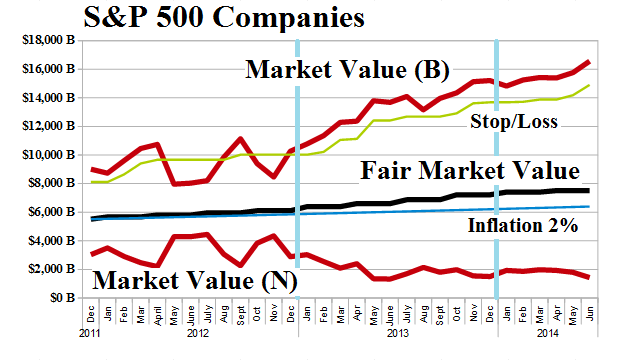

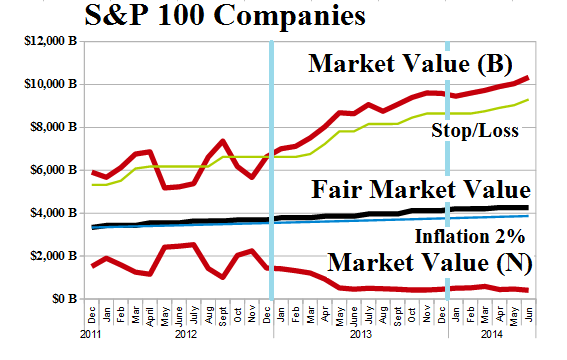

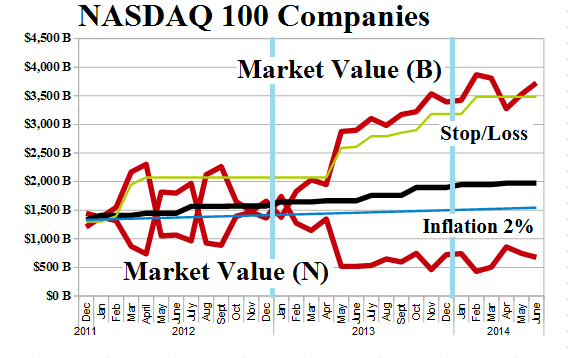

The chart on the left (Figure 3) shows the market value of the (B)-companies when they are (B)-companies, that is when the ambient stock prices appear to be at or above their price of risk.

The faint green-line below it shows a moderately effective stop/loss policy that is applied to the (B)-companies, and it never decreases; absent a need for liquidity, the (B)-companies are only “sold” when the market no longer wants them, and an attentive “stop/loss” policy is a “profit-making” opportunity for us to “re-fresh” our portfolios.

Figure 5: (B)(N) Dow Jones Utility Companies – Risk Price Chart – June 2014

The thick black-line is the “Fair Market Value” of all the companies in the Dow Jones Industrials, and it is the sum of 50% of the market value of the (B)-companies at their price of risk and 50% of the market value of the (N)-companies at their price of risk; it is the real “smart beta”, but please see below for further explanations.

The faint blue-line below it is the growth by inflation at 2% of the “Fair Market Value” since December 2011, which is indicative of the current situation, but it’s not hard to imagine how these relationships will change if inflation picks-up and the interest rate on bonds keeps pace.

And the red-line on the bottom shows the market value of the (N)-companies when they are (N)-companies, that is when the ambient stock prices appear to be below their price of risk, and in this case (Figure 3 above), it actually does go to zero because all thirty companies in the Dow Jones Industrial Companies are presently (B)-companies.

The “Fair Market Value” is an unbiased estimator of what the “market” is actually worth “as good as cash, but better than money”, and that is not the same as the sum of the “fair market value” of all the companies in it, which would be the sum of their market values when priced at the price of risk, which sum is usually (but not always) less than the sum of the market values of the (B)- and (N)-companies.

For example, the (B)-companies are always “undervalued” because the demand for them at those prices exceeds the supply, which is why they have those prices, whereas the (N)-companies are always “overvalued” because the supply of them exceeds the demand for them at those prices, which is why they are “overvalued”; hence, the “fair market value” of a company is its value at the price of risk, and the “Fair Market Value” of the “market” is the unbiased average of the two markets, such as they are, priced at the price of risk.

Figure 6: “Indicative Bubblemania” and The Boggart Defense

The (B)-companies tend to pull the “Fair Value Market” up, whereas the (N)-companies tend to pull the “Fair Market Value” down and, obviously, a surfeit of (N)-companies over (B)-companies will demonstrate a “recession” in the stock market, as well as everywhere else, likely.

Nor does the market “bubble” that is in evidence in the Dow Jones Industrial Companies (Figure 3 above), seem to be all that fearsome when we look at it that way, but we ought to look at some of the other markets, as well, and put some numbers on (B)- and (N)-company behaviour, in aggregate; please see Exhibit 2 below.

Exhibit 2: All Market – Fundamentals – June 2014

All Market Fundamentals – June 2014

Figure 7: (B)(N) S&P 500 Companies – Risk Price Chart – June 2014

Figure 8: (B)(N) S&P 100 Companies – Risk Price Chart – June 2014

Figure 9: (B)(N) NASDAQ 100 Companies – Risk Price Chart – June 2014

Figure 10: (B)(N) S&P TSX 60 Companies – Risk Price Chart – June 2014

Figure 11: (B)(N) S&P TSX Completion Companies – Risk Price Chart – June 2014

The “All Markets” portfolio is currently worth $30.2 trillion and paid $645 billion to its shareholders last year, for an aggregate dividend yield of 2.1% and a return of earnings of 39%; moreover, the aggregate debt is $39 trillion, although the bond market is said to be worth at least twice that, and all this money makes the US national debt look more like “petty cash” and very affordable, and there’s also a lot of money afloat in the CBOE options market.

Nevertheless, many pension planners are turning the screws on Brazil, Turkey, and so forth, to fund our pensions in the future, in excess of the $645 billion that is currently being paid-out by these companies this year and probably every year in the future, adjusting for inflation as we go; pension planners are also having problems “capitalizing” on the increase in market value of over $5.8 trillion and +26% last year, because it’s deemed to be “unreliable” and might not be there for us in twenty-years or so, although we would think that our problems would be a lot worse than “pension income” if they weren’t.

Moreover, investors have thrown in another $2 trillion and +7% so far this year, but could take it back at any time, we suppose.

However, despite all of these big numbers, we can’t afford to be too casual; for example, the dividend of $645 billion amounts to about $1,600 per capita, assuming about 400 million people in North America at this time, nor is it easy to “take profits” from the $5.8 trillion in capital gains.

On the other hand, it should also be clear that a pension plan with $30 trillion in assets can’t expect to fund pensions with dividends alone, even now, and if pension plans are expected to pay benefits in the future, they need to demonstrate some ability to do that now, and we need to know what that “ability” is, every year, for which increasing assets under management is not the answer; please see our recent Post on “The Pensionnaires” for more information.

Unlike “beta smart” and so forth, the Perpetual Bond™ conspires to return income every year, in any market, and has a very small vocabulary – safe, liquid, and hopeful – and if we don’t hear those words, it’s not an investment.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.