(P&I) The Process – Commensurability

The In Process Game

Essay. If A and B are two sets of numbers (positive integers), we can imagine that if we take enough copies of A, say p-copies, then the sum of the numbers in p-copies of A will exceed the sum of the numbers in B, and similarly, if we take q-copies of B, then the sum of the numbers in B will exceed the sum of the numbers in A.

However, we can ask for a little bit more; suppose that there are n-numbers in A and m-numbers in B, and we choose p-copies of A and q-copies of B so that ∑p×a[i] ≥ ∑q×b[j], where the first sum is over 1≤i≤n, and the second over 1≤j≤m; similarly, we may also find p and q so that ∑p×a[i] ≤ ∑q×b[j] and the numbers d(p,q) = ∑q×b[j] – ∑p×a[i] can be both positive and negative and of any size because for any p and q, d(k×p, k×q) = k×d(p,q), k=1, 2, 3, … , and we also note that d(p,q) is a decreasing function of p, as p increases, and an increasing function of q, as q increases; in particular, if d(p’,q’)>0, we can increase p’ to p” so that d(p”,q’)<0, and then increase q’ to q” so that d(p”,q”)>0, but it’s not clear that, in any such case, there are any (p,q) with p'<p<p” and q'<q<q” such that d(p,q)=0, in which case we might say that A “covers” B by “replicating” itself p-times to cover B q-times, so that the sum of the “payables” (A) equals the sum of the “receivables” (B).

However, if a=∑a[i] and b=∑b[j], then a and b are integers, and if we put q=a and p=b then. obviously, p×a=q×b (=a×b=p×q) and d(p,q)=0, and if reduce the ratio p/q to its lowest terms, then the number d=log(p)/log(q)=log(b)/log(a) is the “fractal dimension” (or “Hausdorff Dimension”) of the set A in B in the sense that a^d = b and d is the smallest (and only, in this case) such number, in the same way as we say that R×R=R² covers the plane.

That result becomes more interesting in the context of The Process if we think of (a) as the set of payables of a company in-process with a set of receivables (b) with measures a=p((a)) and b=p((b)), respectively; since they are in-process, they satisfy the 1st- and 2nd E-conditions with a constant modality, 0<α<+∞, such that a×log(a)=α×log(b) and b×log(b)=α×log(a), respectively, and, therefore, all such (a) “cover” all such (b) with a “fractal dimension” that is proportional to the measures a and b, respectively; that is, if d=log(b)/log(a), then a=α×d and b=α×(1/d), and, similarly, all such (b) “cover” all such (a) with a fractal dimension, 1/d, that is proportional to b; please see Exhibit 1 below for an example of how this works.

Exhibit 1: The Cantor Set with Hausdorff Dimension

The Cantor Set

In its most basic form, the “Cantor Set” is a fractal with dimension d=log(2)/log(3)=0.63093… ; if we try to cover the set marked as “111” for three (top line in green) with the set marked as “101” below it (for which the “middle third” is missing), then we can get an exact cover of four copies of the former with six copies of the latter, or two copies of the former with three copies of the latter, if we shift the elements from “101” to “110”; or the same with “011” if we begin “payment” at the other end, which might be thought of as “collecting” the longest-dated “receivables” first, (b), and paying them out in (a).

This observation has other implications for the firm in-process; since 0≤a,b≤1 are measures (or probabilities), the fractal dimension of (a) over (b) is always very high for small α (Company A) and attains its minimum at a=1/e and its maximum on the “delivery of product” at a=b=1, whereas the fractal dimension of the corresponding (b) over (a) is 1/d and, therefore, very low, and it obtains its maximum on the delivery of product, and the reverse is true for α>1 (Company C) in which the fractal dimension of (a) over (b) is always less than 1, but (b) over (a) is always greater than 1 (discounting a and b near zero, which is less significant in-process, but quite significant at the “beginning of process” which is more like the Company D at α=1/e=0.368… before the modality is established); please see “The Process End of Process” for more information on this.

Moreover, if the sets (a) and (b), however selected, have a non-zero “fractal dimension”, and the company is in-process with modality α, the elements in them, which are “payables” and “receivables”, are not countable despite their humble origins in the σ-algebra within which they exist, and although a company with modality α=R/P calculated from any balance sheet will exhibit the properties of that modality, it will not actually “have” that modality. Nor does the modality, per se, suggest very much about how investors will “price” the company; please see Exhibit 2 below and click (and again to make it larger if required) on the link “All Market Fundamentals” for more details.

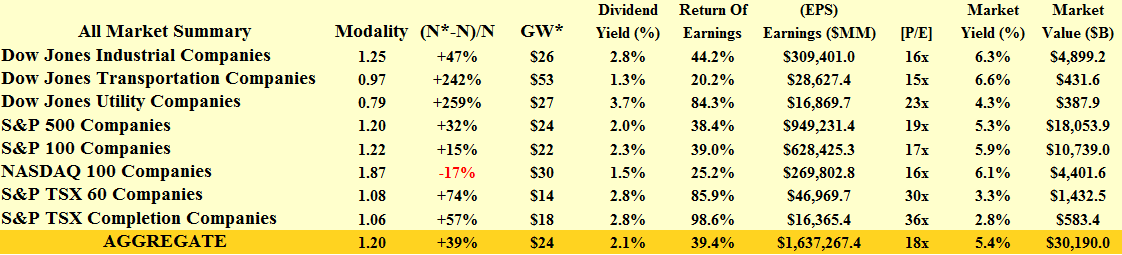

Exhibit 2: All Market Modality (Theory of the Firm)

All Market Modality – June 2014

(N*-N)/N is the expected growth in the net worth of the “firm” if it just continues to do what it does, every day, Monday through Friday, and, therefore, representative of the dividends that these companies will be able to pay.

GW* is the price that investors are willing to pay for $1 of the Coase Dividend which is the balance sheet worth of the trading connections and, therefore, the worth of the enterprise of the company when compared to $1 in cash; the “Market Yield(%)” is the inverse of the [P/E]-multiple expressed as a percentage, and it is comparable to the coupon-rate of a perpetual bond purchased at the market price; at the present time, the combined dividend yield (2.1%) and the market yield (5.4%) is 7.5% and that yield is mostly affected by what investors are willing to pay for stocks rather than the company earnings which are unlikely to change as quickly; for more details of these calculations, please visit our Post “The Theory of the Firm” and for a summary of the recent market behaviour of these companies, “(B)(N) Bubblemania and The Working Poor“.

A “Dynamical System”, imagine that?

However, the existence of a measure and σ-algebra (N), and the fractal sets that are usually realized as the “limiting sets” of stable and unstable orbits in system dynamics, does suggest that we can think about the “economy” in an entirely new way that is not so obviously linked to “prices” and “returns” and “volatility”, which have no foundation and are reactive, but to the balance sheet which provides us with a “Conservation Law”. Stay tuned.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}