(B)(N) MannKind and The Belviq Chronicles

Stock prices are made here – Bid & Ask & How Many

Drama. Analysts and investors keep trying to find “information” in stock prices, and they’ve been trying to do that for more than a hundred years, to somehow relate past and recent stock prices to what they might be tomorrow, or eventually (The Street, June 5, 2014, The Expected Rise and Inevitable Fall of MannKind).

They ought to have discovered, by now, that there is no information in a stock price, or even a bunch of stock prices, that could in any way suggest what the future stock price might be, or even within some “volatility”-based range, or even within a “reasonable expectation”. Nor is there any medicine or treatment that might cure them of that “bad habit”, the gambling habit, nor are we about to offer any, because we understand its nature.

However, we would think that the better question to ask and answer for any investor who actually buys and sells real stocks is “Why would we take our hard-earned cash and buy this “certificate”, this piece of paper or account entry, that says that we have a right, enforced by law, to an interest in the future dividends cum earnings, both of which are optional, and even ownership, of this company pro rata anyone else who owns such paper?”

But we also note that that is not a question that is asked by investors who buy “markets” and use some variant of Modern Portfolio Theory (MPT) and the Capital Assets Pricing Model (CAPM) to buy a piece of everything, according to some grander “vision” to which individual stocks are expected to respond, or be driven to respond, for which reason we also don’t know, because for all that, we’re provably better-off by just buying, holding or selling the actual stocks of that same entire market without trying to “parse” our vision with assorted “fractions” that depend on “expected returns” which are a guess, anyway, and anyway, don’t drive the prices. Nor can we help them (The Wall Street Journal, June 5, 2014, Morningstar to stock pickers: You’re worthless – which author has an agenda and “sells” ETFs and takes comfort in that fact by alleging that there is some kind of “science” involved – alchemy?).

Figure 1: The Value of $1 Since 1776

We can, however, offer a reason that we might buy a stock, rather than some vaporous paper in a mutual fund or ETF.

The reason is that our money is certainly (that is, for sure) better-off invested in the stock than it is invested in our pocket, where it’s likely to melt-away into nothing unless we do something to make it work for us; please see Figure 1 on the left.

And we also know, and can prove, that our money invested in a stock that is trading at or above the price of risk is “as good as cash and better than money” and working hard for us because in addition to 100% capital safety and 100% liquidity (which is what we have in cash), we are hopeful, and have reason to be, of a return on our money that exceeds the rate of inflation and therefore, preserves or betters its worth.

And as we’ve said before, those are the words that move us – safe, liquid, and hopeful – and if we don’t hear those words, we can stop listening because the next offer won’t give us what we want.

And we can also give a reason, the same reason, that we might not buy or hold a stock if it’s trading below the price of risk and therefore, it is not safe, not liquid, and although it might be hopeful, we can wait until it demonstrates a reason for such hope, and until that time, it’s just a stock and a piece of paper that is trading in the (N)-zone of investor uncertainty.

So-armed with our own bias, but a reasonable understanding of above and below, we can now examine today’s straw-men for the words that we want to hear – safe, liquid, and hopeful.

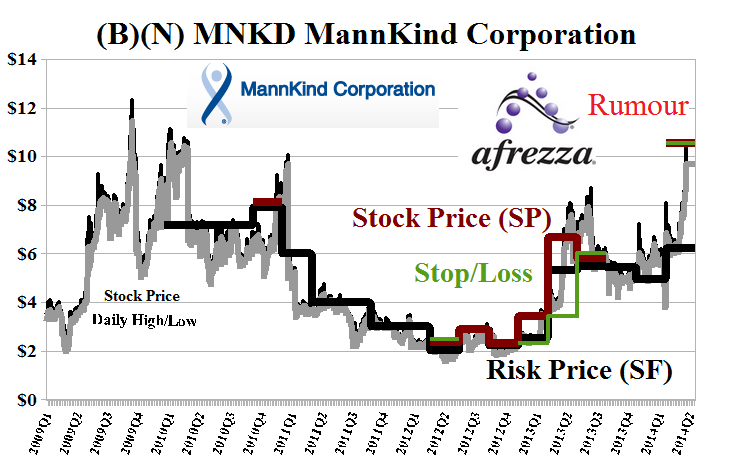

First-up is MannKind Corporation (please see Exhibit 3 below), which is now waiting for an FDA-approval announcement that is scheduled for July 15 on its new product, Afrezza, and the stock market, being a team sport, is also waiting and watching and stirring at the doorstep – Yes, we win – No, we lose – on July 15. It’s true (please see Exhibit 3 below) that MannKind at $10+ is trading above the price of risk ($6) right now, and we can buy it on that basis at any price above $6, but we’ve jacked-up and set our stop/loss at $9.50 currently, because we have no idea what is going to happen on July 15, which is a Tuesday, and the day before a local celebration of “World Snake Day” which we also need to prepare for.

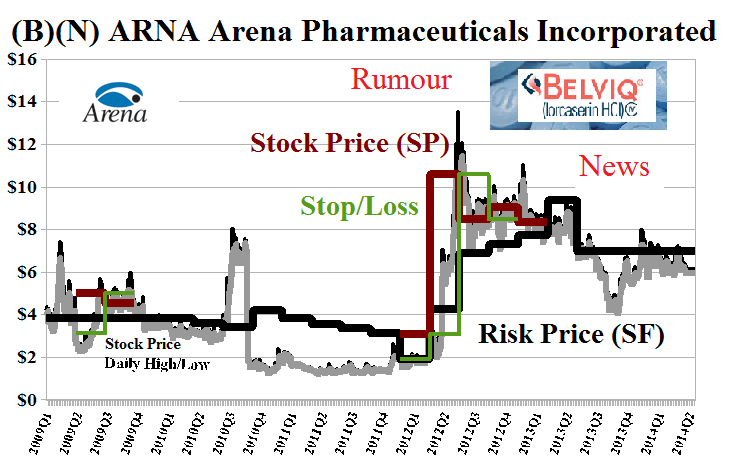

Of course, when rumour becomes news, investors might sell again, as in the case of Arena Pharmaceuticals which went through a similar trauma and elation, twice, before its new drug, Belviq, was approved and is now in production as its one product; please see Exhibit 2 below.

Exhibit 1: MannKind and The Belviq Chronicles – Fundamentals – June 2014

MannKind and The Belviq Chronicles – Fundamentals – June 2014

Figure 2: (B)(N) MannKind and The Belviq Chronicles – Risk Price Chart – June 2014

A normal person would easily be excused from the hunt for “profit” and dividends in these two companies, whose demonstrated interest is elsewhere; please see Exhibit 1 above.

It’s also evident, from the Risk Price Chart, Figure 2 on the left, that the net investor interest does not stray far from cash, as the aggregate market value of these two companies “snakes” its way around the price of risk

We also note, however, that investors are willing to pay $276 for $1 of the Coase Dividend, which is 10× the going rate for the ordinary companies on Wall Street, and the expectation must be that these companies will someday be “worth” at least five-times what they are now (N* $0.5 billion compared to N $0.1 billion), and so they must be expecting future earnings well in excess of last year’s losses of ($274 million); please see Exhibit 1 above for the details and click on the link (and again to make it larger) for the latest news on “(B)(N) MannKind and The Belviq Chronicles – Prices & Portfolio – June 2014“.

Exhibit 2: (B)(N) ARNA Arena Pharmaceuticals Incorporated – Risk Price Chart

(B)(N) ARNA Arena Pharmaceuticals Incorporated

Arena Pharmaceuticals Incorporated is a biopharmaceutical company engaged on discovering, developing and commercializing drugs that target G protein-coupled receptors to address unmet medical needs.

From the Company: Arena Pharmaceuticals Incorporated a biopharmaceutical company, discovers, develops, and commercializes novel drugs that target G protein-coupled receptors. The company offers BELVIQ, a drug used to treat chronic weight management in adults. Its products under development include APD811, an agonist of the prostacyclin receptor, which has completed single- and multiple-ascending dose Phase I trials for the treatment of pulmonary arterial hypertension; and temanogrel, an inverse agonist of the serotonin 2A receptor for the treatment of thrombotic diseases, which has completed single- and multiple-ascending dose Phase I trials. The companys products under development also comprise APD334, an agonist of the sphingosine 1-phosphate subtype 1 receptor for the treatment of conditions related to autoimmune diseases, which has completed Phase I single-ascending dose trial; and APD371, an agonist of the cannabinoid receptor 2 that is in Phase I single-ascending dose trial for the treatment of pain. It also manufactures drug products under a manufacturing services agreement for Siegfried AG. The company was founded in 1997, has 310 employees, and is based in San Diego, California.

Exhibit 3: (B)(N) MNKD MannKind Corporation – Risk Price Chart

(B)(N) MNKD MannKind Corporation

MannKind Corporporation is a development stage company engaged in the discovery, development, and commercialization of therapeutic products for diseases such as diabetes.

From the Company: MannKind Corporation, a biopharmaceutical company, focuses on the discovery, development, and commercialization of therapeutic products for diabetes and cancer in the United States. Its lead product candidate is AFREZZA inhalation powder, an insulin that is in late-stage clinical investigation for the treatment of adults with type 1 or type 2 diabetes for the control of hyperglycemia. The company is also developing MedTone and Dreamboat inhaler devices. MannKind Corporation was founded in 1991, has 265 employees, and is headquartered in Valencia, California.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}