(B)(N) Winners & Losers

The Black Swan…Is Here…But Only On Wall Street

Drama. The big-shots on Wall Street are praying for rain and “volatility” because they don’t know how to make money when the markets are calm and undecided for neither up nor down (The Wall Street Journal, May 19, 2014, Only a ‘black swan’ will bring back stock volatility).

They remind us of the “Sundance Kid” who could only shoot straight, they say, if he was moving too, and the market pariahs who tell us to buy what they already have because the price is going to go up, or to sell what they’ve already sold, short, because the price is going to go down, for which reasons they’ll find for want of pleading and “The Black Swan” if all else fails. Buckle up.

It needs to be moving.

Courtesy: Fox Studios

But, alas, we are unmoved and not moving, and all that we want is what is “fair”, and that simple idea works in every market, moving or not. We want our money to be safe – 100% capital safety – and available when we might need it – 100% liquidity – and we want to obtain a hopeful but not necessarily guaranteed return above the rate of inflation which, if we don’t get it, is just another way of losing our money. Those are the words – safe, liquid and hopeful – that move us.

However, many investors – maybe most – don’t share that view and seem to think that “the market” is their enemy and needs to be “beaten” and there are 10,000 self-help books by effusive “market beaters” to explain how they “beat” it and to earn extra income, we suppose. And so, like a lot of sand-lot players hoping to be discovered for the major leagues, they crave for uncertainty because that’s the only chance they’ll get to play and maybe win big, or small, and they prefer “big”, and maybe out of their league and leveraged with debt, but even small wins count if there are enough of them, net of their loses.

The “bespoke players” with better shoes and new uniforms, also play to win, but they play on “value” and pray that they’ll be noticed by the market, and get the “call”. But, in our view, hope, uncertainty and prayers, don’t count for much, because to win, we need to play the game, and the game is not about winning by chance, but it’s about not losing by necessity. Yes, those are the words – safe, liquid and hopeful – that move us.

Today’s hopeful and certifiable “market beaters” are TSLA, IQNT, VJET, APP and VNET (The Street, May 30, 2014, 5 Stocks Ready for Breakouts) and, they say, that the five companies GES, BDX, TCK, UAL and AXP are likely to be the “losers” (The Street, May 30, 2014, Sell These 5 Toxic Stocks Before It’s Too Late), although we don’t know for how long.

Figure 1: Do you see a vase, or is that just two faces? Or is it both?

“Technical analysts” (ibid., The Street) rely on the ruler and compass to see things, patterns, that might not be so obvious to the untrained eye.

But it’s difficult to chart one hundred or so companies, and after a few dozen, we would think that we’ve seen every chart that has ever been made up to a “scale” factor and a “translation” (the planar affine group). Maybe less, but nobody has bothered to count them, so we don’t really know how many different ones there really are, or even how many have yet to be discovered, although from what we’ve seen, there might only be four of them – positive or negative scale factor and positive or negative translation – but that’s enough to generate the “fractal geometries” from clouds to ferns and fig-leaves, and any stock price that we could imagine.

Moreover, if we had this kind of a “chart typology”, we could test them and see what predictive value they have, and for how long, and more investors could say something like “It’s a C4, buy it, or it’s a D2, don’t”, each of which support the desired outcome, and we could construct portfolios of today’s C’s and D’s, and expect that performance, which gets us closer to not losing.

Towards that end, but far short of it, we put all ten of them together to make a portfolio of sorts, and to see if there’s some bias in it, one way or the other, albeit with a rather small sample of alleged C’s and D’s, absent a more intensive “chart typology” which appears to be really needed for those of us less gifted with a ruler and compass, or prone to “blinking” or “squinting”; please see Figure 1 above.

But the “chartists” might not want to know the answer to that question, because we have looked at “breakout” stocks before, in February, and the results were “scary” then with an indicated downside volatility of minus (-24%) in the next quarter – which is exactly what happened almost as soon as we said it – and in aggregate all of those stocks, but for two (MNKD MannKind Corporation and SGMO Sangamo BioSciences Incorporated), are now in the minor leagues and trading in the (N)-zone of investor uncertainty below the price of risk; please see Exhibit 1 below for new evidence of the “flat-liners”.

Exhibit 1: (B)(N) The Broken-Down Breakout Stocks – Risk Price Chart – February to May

(B)(N) The Broken-Down Break Out Stocks

But mere facts seldom deter the true believers, and that creates opportunity for those of us who want merely to be “fair” and just play the game.

But again! it seems that somebody slipped-up, or blinked, because we’re buying what they’re selling – so keep selling – and we’re not buying what they’re buying – so keep buying, and maybe we will too, but not today.

And we checked the reports again, because maybe it was we who “blinked” inappropriately and have the “Figure 1”-problem, and we just couldn’t believe our own eyes, but, no, no, that’s what they said, and our “hearing problem” is not of the issue; please see Exhibit 2 below.

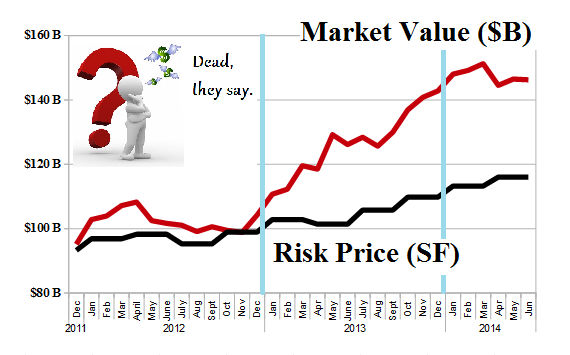

Exhibit 2: Winners & Losers – Fundamentals – June 2014

Winners & Losers – Fundamentals – June 2014

Figure 2: (B)(N) The Winners – Risk Price Chart – June 2014

Figure 3: (B)(N) The Losers – Risk Price Chart – June 2014

These companies (please see Figure 2 on the left) could be “alive” because they’re not “dead” yet.

Last year, they lost ($219 million) and only paid $10 million in dividends, which might be disappointing to those investors who bid-up their prices by $18 billion and +315% last year.

But maybe they just don’t have the “right stuff“, after all, although the “ruler and compass” says that it’s in there, somewhere.

In contrast, the “losers” (in Figure 3 on the left) have probably lived too long and are giving their money away, because they have a lot of it.

Last year, they paid $2 billion in dividends for an aggregate return of earnings of 28% and a current dividend yield of 1.4%, and they also gained $39 billion and +37% against all odds.

Baseball! Hot Dog! Let’s Play Ball!

Please click on the link (and again to make it larger if required) “(B)(N) Winners & Losers – Prices & Portfolio – June 2014” for more details of who we think might be dead or alive, still.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.