(P&I) The Pensionnaires

Figure 1: The CPPIB Pensionnaires

Drama. This is our fourth and last Post on the plight of the Canada Pension Plan Investment Board (CPPIB) which is managing our money for the future, but not for now and will, therefore, fail with respect to all of its objectives and it’s failing now.

Figure 2: The CPPIB Performance

This year in their fiscal year 2014 which ended in March, they did much more than what they said they would do, and benefited from the boisterous markets in North America and Europe, as well as in other astute investments which have increased in value but not income.

And we ought to be happy with that – and we are because things could be a lot worse (please see Figure 2 on the left) – but we’re not, because even though the plan made $30 billion on paper in the investment market, they still took $5 billion from us, the pensionees, in cash, and they have no plans to anticipate an increase in the benefits for the pensioners, and despite all of that money, and all of that “income”, they can’t afford to do it; please see Figure 3 and 4 below.

Where are the benefits?

And that’s where the problem is and why they will fail and are failing now; if they can’t do it now, that is if they can’t demonstrate some benefits now and some ability to pay them if they wanted to, they won’t be able to do it then either.

The prescription for failure is the common and unfounded assumption that a large pool of invested capital will be enough to solve the problem of paying benefits with a possibly negative cash flow in which payable benefits exceed the then current contributions, because they believe that even if the investment earnings are meagre in any year or even for a few years, they will still be able to pay what is required of them for a few years until the plan is fixed.

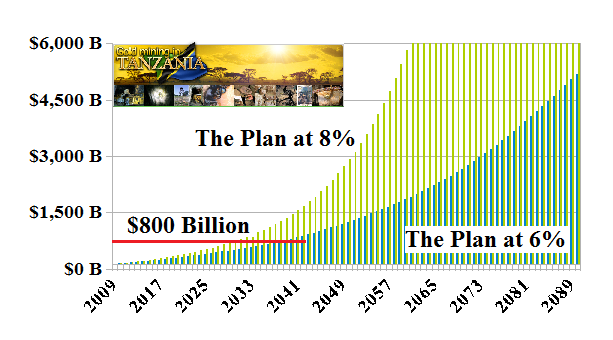

Figure 3: The Plan at 6% and 8%

However, that assumption including all of the anticipated expenses and contributions related to demographics and employment and the assumption that the investment returns will be about 6% per year on average (which is their assumption and geared to 4% plus inflation) gives us the chart in Figure 3 on the right for which the compelling and logical Figure 1 above is just the first part and takes us only to the often-cited $800 billion in 2040 but not to the amazing $5 trillion (which is more than the current market value of the Dow Jones Industrial Companies) in 2090 which is also a part of “the plan”.

Should the plan maintain +8% which is its long-term average annual return, we have the equally improbable +8% accumulation with those same assumptions and +10% is off the chart in thirty years but the CCPIB does not abuse our credulousness with either of those projections; please see Figure 3 above with 6% dark and 8% light (and click on the charts to make them larger if required).

Most investors would shun this projection as a “vision” and a “hockey-stick” and nothing more than a much-touted penny-stock – a gold mine in Tanzania that we can buy on any day on Bay Street. But that does not deter the “visionaries” who are responsible for these plans and endorse them with their signatures every year despite the evidence of experience.

Wealth Management and the Volatility Defence Against All Odds

Courtesy: Paramount Pictures “Beau Geste” 1939

But they’re not “good for it” at the end of the day and we, the “shareholders” of this enterprise and the ultimate “defenders” and dependants of the capital, will have to be; please see the “26th Actuarial Report on the Canada Pension Plan December 2012” for more details on the assumptions and data.

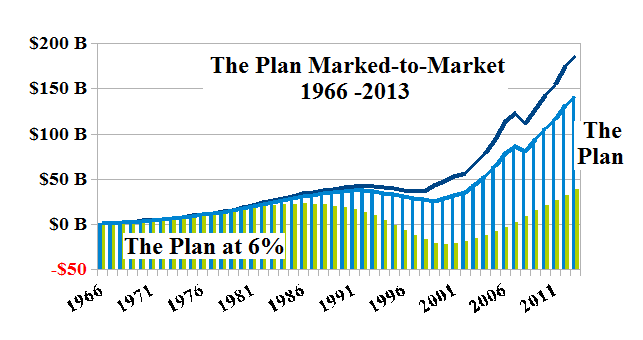

Figure 4: CPP Actual 1966 through 2013

The last time that the plan was in trouble was in 1983 through 1999 in which every year for fifteen years there was a negative cash flow that aggregated to a deficiency of $52 billion for the plan which then had assets of between $26 billion in 1983 and $43 billion in 1999 when it paid-out 7% of its assets but between 10% and 16% of its assets for each of the seven years previous to that (1992 through 1998); please see Figure 4 on the right in which the realized investment returns of the time are accumulated with the positive and negative cash flows of the time and fall short of the “marked-to-market” paper profits by $50 billion in 2013 and which paper profits they might not be able to pull-down when they need them (and that is already in evidence), as was the case in the “liquidity crisis” that affected the banks in 2008 and 2009 and which was ended by a multi-trillion dollar bail-out by the government that is still going on today and has rattled both the bond and stock markets world-wide.

The first expected payouts of the “new plan” (please see Figure 3 above) are expected to begin in 2023 with $731 million but are always required thereafter and the plan expects to payout $208 billion by 2046 and still have a capital of $1 trillion to (ah) “invest” from which it must payout between $20 billion and $160 billion per year to the end of the century in 2090 and which they anticipate to be only 2% to 3% of their assets in any year. Amazing! Would that the banks were so smart or almost any of the failing pension plans that report to us on almost any day.

Figure 5: Dead in Twenty Years At 10% More Benefit And 6% (dark) and 8% (light) Returns

However, it’s not hard to get the plan into deep trouble with a modest request or even a mis-calculation of just a few years; for example, if everything is the same as above but we try to increase the benefits by just 10%, then the plan is “dead” in twenty years after having “peaked” at $300 billion in 2032 and has no chance at all of reaching $800 billion in 2040; please see Figure 5 on the right in which the deficits would need to be paid by the taxpayers and which amounts eventually exceed the entire budget of the Government of Canada.

That simple result was overlooked in the rigorous and exhaustive “stress testing” of the portfolio, the “asset mix” and market returns which “stress testing” is largely irrelevant because “the market” and “volatility risk” which they think that they know how to control do not have anything to do with reliable investment returns (please see our Post The Seven Year Itch Since 1897 and The God Stock for an overview of what they fear and how they’re dealing with it) and “the market” per se will prefer to do nothing for the benefits of the pensioners or the relief of the “pensionees” who will need to pay those benefits even after paying for them for all those years.

Figure 6: The Perpetual Bond in the Dow Industrials “More nuts is not as good as an interest in the trees that make them.”

And, hopefully, that says everything that we need to say about “planning for the future” with a pension plan that just accumulates and never pays a dividend until it has to; if it can’t do it now, it won’t be able to do it then.

Read it. Learn it. Or live it.

The solution is called The Perpetual Bond™ which separates any market into a part that behaves like a “risk-free” bond for income and liquidity and its exact complement that behaves like an at-risk portfolio of stocks beset by uncertainty.

And that’s an understanding of the market that these “visionaries” just don’t have and they are, therefore, attempting to solve the wrong problem, a problem of their own design because they think that they have a solution for it despite the evidence of decades.

For example, the companies that are in the Perpetual Bond™ now in just the Dow Jones Industrials have been in it for most of the last three years and returned 43% of their earnings and $134 billion to their shareholders last year and, in addition, another +28% in capital gains some of which we could draw-down for a rainy day (or a wet market that might shadow our opportunities) and put it into an inflation-protected product such as Real Return Bonds (RRBs) in which we lend our money and some of our out-sized profits to the Government of Canada and we won’t have to travel all over the world to find somebody who might want it; or we could return capital and pay dividends to our shareholders like everybody else does; or we could increase the benefits including healthcare and something other than a pauper’s burial and next to nothing for those whom we leave behind; please see Exhibit 6 above.

Moreover, if the Dow is not big enough, then how about including the Dow Transports or the Dow Utilities or the S&P 500 or the NASDAQ 100 or the S&P TSX 60, all of which we have discussed in these Posts and each of which and all of which admit a Perpetual Bond™ which does not depend on the market per se for its returns or capital safety or liquidity.

We also note that the documented real-time performance of the Perpetual Bond™ in every market during the past five years since 2008, has demonstrated that +20% per year plus dividends is just “normal” and although that performance cannot be guaranteed, it can be expected with no risk to the capital and 100% liquidity and the “take-up rate” can be monitored every day so that there are no surprise endings.

Brazil! All that and funding for Canadian pensions too! They say.

In other words, the “markets” are nothing like what the visionaries think that they are and we would be much better-off (absent the Perpetual Bond™ which is better still) if they just bought and held the common stock of, for example, all the companies in the Dow Jones Industrials and the S&P TSX 60 equally-weighted by value without distinction and with an attentive (and profitable) stop/loss policy; a few primary brokers, a custodian, three clerks to handle the paper-work and daily reports, and two accountants to make the mandated decisions are all the staff that are required to run a portfolio of almost any size. And none of them needs to know anything about the “market” or the companies that are in it other than by name.

But such thoughts are decimating to the “investment industry” that runs these plans and what about Brazil and Turkey and so forth, they say? And what about “alternative investments”, they plead? Please see our Post on “The World According To Money” for the answer.

For more on this subject and the problem of portfolio management in pension plans, please see our recent Post, “(P&I) My Name Is Bond (James Bond)“.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The Market or the S&P 500 Sidewinders or older Posts whose future is already here such as The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.