(B)(N) The NASDAQ 100 Trifecta

Full, Half-full or Empty?

Drama. The demand for stocks continues to be high and analysts and pundits continue to wonder why the glass is not half-empty even as nothing, not good or bad news in earnings, good or bad news in employment, good or bad news from China, Brazil, Greece, Turkey or the Ukraine, for example, seems to cause this market to lose its step (The Street, February 25,2014, Jim Cramer: Waiting This One Out).

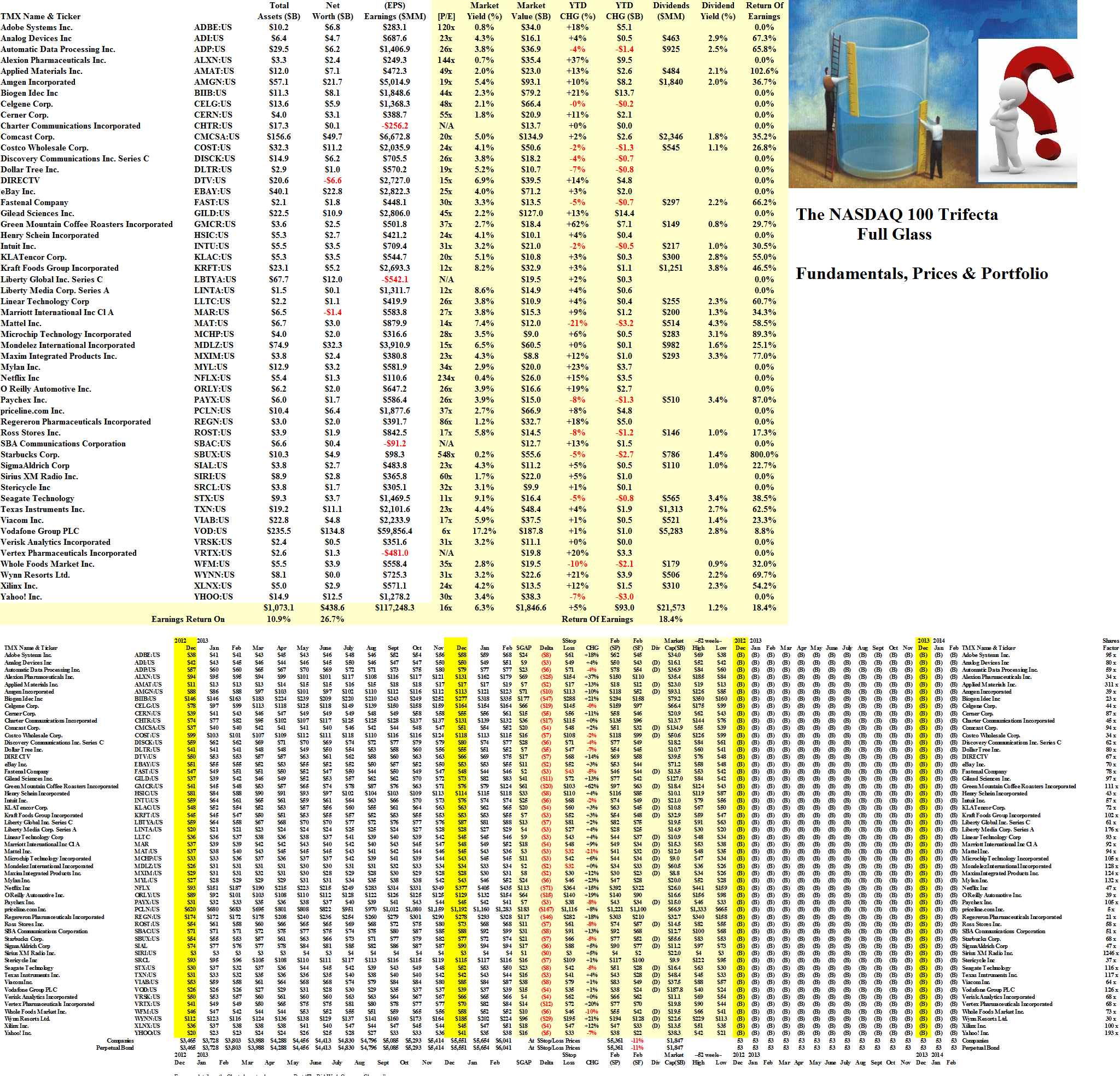

Our glass is full in the big-caps because we’re fully-invested in the Dow Jones Industrials (all thirty companies) and almost all of the Transports and Utilities but for three companies (Exelon, FirstEnergy, and Pacific Gas & Electric); and all but eight in the S&P 100 and all but fourteen in the NASDAQ 100.

So while we’re waiting for the next round of market volatility or a long-awaited “swoon” and in search of “liquidity“, we divided the NASDAQ 100 into three markets, “The Trifecta”, in order of liquidity: the “Full Glass” is all the companies that are in the Perpetual Bond™ now and all of last year (Full Glass); the “Half-full Glass” is all those now and some of last year but not all of last year; and the “Empty Glass” is all those in neither (Empty) and are the most illiquid (naturally).

Both the Full Glass and the Half-full Glass are highly liquid stocks for which the demand at the current prices exceeds the supply; however, the Half-full glass might have more room at the top and the Empty glass speaks for itself. Please see Exhibit 1 below for the Market Value ($B) and Risk Price (SF) for each of these three “glasses” and clink on the links (such as the Full Glass) below for more detail of their portfolios and fundamentals.

Exhibit 1: (B)(N) The NASDAQ 100 Trifecta – Risk Price Chart – February 2014

(B)(N) The NASDAQ 100 Trifecta – Risk Price Chart – February 2014

We can see from the Chart that the “Full Glass” group of fifty-three companies gained +46% and +$552 billion last year (Red line in the middle) and that the “price of risk” estimated by the Risk Price (SF) (Black line in the middle), has also been rising steadily; in addition, the “Full Glass” group has gained $93 billion and another +5% since the beginning of the year.

The Full Glass also earned $117 billion last year for a return of 27% on the shareholders equity and paid $21.5 billion in dividends for a dividend yield of 1.2% and an 18% return of earnings to the shareholders.

The current market yield is 6.3% (the inverse of the [P/E] at 18×) and they might be considered “undervalued” in the usual sense but they are definitely “undervalued” in terms of the Demand/Supply Equation and we ought to be able to sell large blocks of them without undue downwards pressure on the stock price; on the other hand, there aren’t any bargains and buying them in large blocks will be a trial.

The Empty Glass

In contrast, the seventeen companies (now fourteen because Cisco Systems, F5 Networks, and VimpelCom Limited ADR recently became eligible for inclusion in the Perpetual Bond™) in the “Empty Glass” were not hoisted last year (naturally) and didn’t do much of anything.

The current market value is $300 billion and they paid $8.4 billion in dividends for an aggregate dividend yield of 2.9% and a return of earnings of 40% on earnings of $21.3 billion and a 15.6% return on the shareholders equity. With a [P/E] multiple of 14× and market yield of 7.2%, they are still “overvalued” even though they gained $8 billion and +3% since December and our estimate of the downside in the stock prices is minus (11%) should the market “swoon”.

The “Empty Glass” companies are “illiquid” for the obvious reasons but also because buying them in large blocks will find grateful sellers who might sell for less; and selling them in large blocks will be a chore and likely put downwards pressure on the stock price. On the other hand, patient money might find some deals in vaunted names such as Altera Corporation, Bed Bath & Beyond Incorporated, Broadcom Corporation, and so on. Please Click on the link for more details.

The thirty companies of the “Half-full Glass” are the largest by market value, $2.3 trillion, but only because they include the out-sized Apple Incorporated at $474 billion (or whatever). These companies are all trading in the Perpetual Bond™ since December and have gained +$90 billion and +4% since December and gained $540 billion and +33% last year but they also gained +58% when worked in the Perpetual Bond™ as a portfolio of stocks and they’re already up +16% so far this year but they have not been bought and held with the same conviction as the companies in the “Full Glass” last year.

Our estimate of the downside in the aggregate stock prices is minus (11%) should the market “swoon” and absent any other surprises that might affect any of these companies. Please see Exhibit 2 below for more details.

Exhibit 2: (B)(N) The NASDAQ 100 Trifecta – Half-full Glass Fundamentals, Prices & Portfolio

(B)(N) The NASDAQ 100 Trifecta – Half-full Glass Fundamentals, Prices & Portfolio – February 2014

(Please Click on the Chart to make it larger and again if required.)

For more information on “risk management” and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}