(B)(N) The Insiders

Keyhole Profits. They did what?

Drama. They say that tracking “insider trades” is just “common sense” because insiders tend to know when “real stock-moving events like earnings surprises, corporate actions, and new products may be in the offing” (The Street, February 24, 2014, Top Insider Trades).

We’re not so sure because there is a lot of diverse information and personality that moves prices and markets.

For example, we like all the news, all the scuttlebutt, paranoia and anxiety or panic that tends to move the price but, of course, doesn’t move the company off its game. If the news is good, we can jack-up our stop/loss; and if the news is bad, we could be sold out at the stop/loss, take profits if we have to and maybe pick-up the stock later at a lower price if it’s still trading above the price of risk.

What is “good” and what is “bad” is, therefore, highly subjective in the market and not nearly everyone invests with the modest goals of 100% capital safety and a hopeful return above the rate of inflation even though one of the better ways to make money in the stock market is not to lose it.

Herd of Lusty Rabbits

Volatility Management

Courtesy: NSW Archives

We also like “value investors“, “technical analysts“, “activist shareholders“, “celebrity investors” and hedge funds for the same reason; and we just love the “60/40 and 40/60” guys who move markets; and the portfolio managers who treat their stocks like a herd of lusty rabbits in need of diversification and volatility management.

As far as we’re concerned they are all right, all of the time because it’s their money and they can spend it in any way they like. But to really appreciate them and how right they are, we need to be in the market all of the time. So we put together a portfolio of the recent insider traffic (ibid, The Street) to see how it does in the real world of stock market investing and what defences we might need (Reuters, February 6, 2014, SAC Capital’s Martoma found guilty of insider trading).

We don’t want to discourage anyone but what we found was a “net common nonsense” portfolio in which the purchases are “overvalued” and the sells are “undervalued”. What a surprise! Please see the fundamentals below in Exhibit 1 for purchases and Exhibit 2 for sales.

Exhibit 1: The Keyhole Prophet Profits – Insider Purchases $16 million – February 2014

The Insiders – Purchases – February 2014

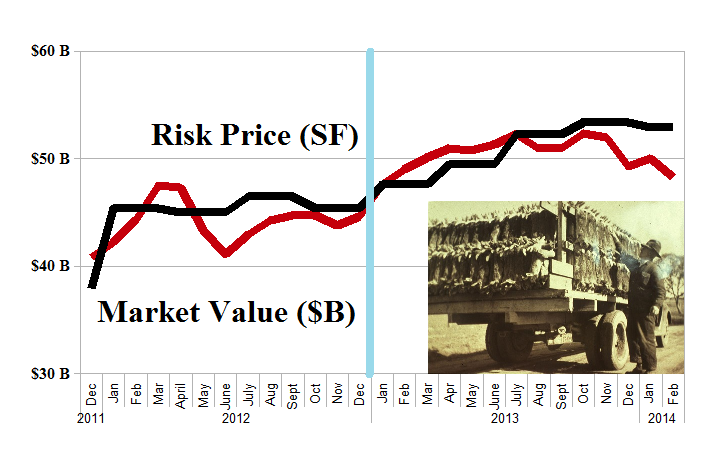

(B)(N) The Insiders – Purchases – Risk Price Chart – February 2014

The purchases amounted to $16 million which is not market-moving in a market capitalization of $48 billion (3000× as much) and two of these companies (Concert Pharmaceuticals and Semler Scientific) are recent IPOs; and Kinder Morgan Incorporated accounts for 80% of everything which distorts the picture.

Undoubtedly, the buyers are enthusiasts (or strategists in the case of Kinder Morgan) and think that the price is too low, that it is a bargain.

However, the Risk Price Chart (on the left) indicates that these companies are, in aggregate, “overvalued” because there is an excess of supply of the stock over the demand for it even at these prices, and they are unlikely to find a buyer at a higher price.

Our estimate of the downside in the portfolio due to the demonstrated volatility is minus (10%) in the next quarter and only two of them (Aircastle Limited and the SM Energy Company) qualify for the Perpetual Bond™ at the present time. Please see the chart below.

(B)(N) The Insiders – Purchases – Prices & Portfolio – February 2014

Exhibit 2: The Keyhole Prophet Profits – Insider Sales $55 million – February 2014

The Insiders – Sales – February 2014

(B)(N) The Insiders – Sales – Risk Price Chart – February 2014

The sellers, on the other hand, seem to be taking some money off the table and possibly don’t understand their good fortune even though it’s a miniscule amount that they’re cashing in, $55 million in a market value of $247 billion (5000×).

These companies are up +$100 billion in the last year and they are all (but for one, Talmer Bancorp) in the Perpetual Bond™.

Moreover, even at these “high” prices, they are still “undervalued” because the demand for them at these prices exceeds the supply.

Our estimate of the downside in the portfolio during the next quarter is minus (12%) due to the demonstrated volatility and that, of course, is easily defeated by setting the stop/loss appropriately with respect to the price of risk. Please see the exhibit below for further details.

(B)(N) The Insiders – Sales – Prices & Portfolio – February 2014

For more information on “risk management” and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.