(P&I) S&P 500 Sidewinders

Become What You Are

Drama. Analysts and investors who are chasing the latest earnings reports and forecasts don’t realize that for many of the companies that they’re chasing, the future is already here and if these companies just keep doing what they do, day-in, day-out, Monday to Friday, then their future net worth will be less than their current net worth. That’s about a third of the companies in the market that are busily and actively and efficiently winding-down and there’s nothing that they can do about it because if they continue to be what they are, they will become what they are.

In the notation of the theory of the firm, the future is already here for those firms because their current net worth (N) is greater than their future net worth (N*); and we hasten to add that that doesn’t necessarily mean that they’re not going to make any money; it just means that it’s harder for them.

In the notation of the theory of the firm, the future is already here for those firms because their current net worth (N) is greater than their future net worth (N*); and we hasten to add that that doesn’t necessarily mean that they’re not going to make any money; it just means that it’s harder for them.

Nor does it mean that they can’t change their next future or even that they might want to or should; but it’s nonetheless helpful to know the future and to know why that future is theirs. And it also has meaning for understanding why a stock price is what it is because the performance or dynamic of the stock prices of the “Sidewinders” is systemically very different from the performance of the “Up-Winders” for which (N*) is greater than (N); please see Exhibit 1 below for the new fundamentals.

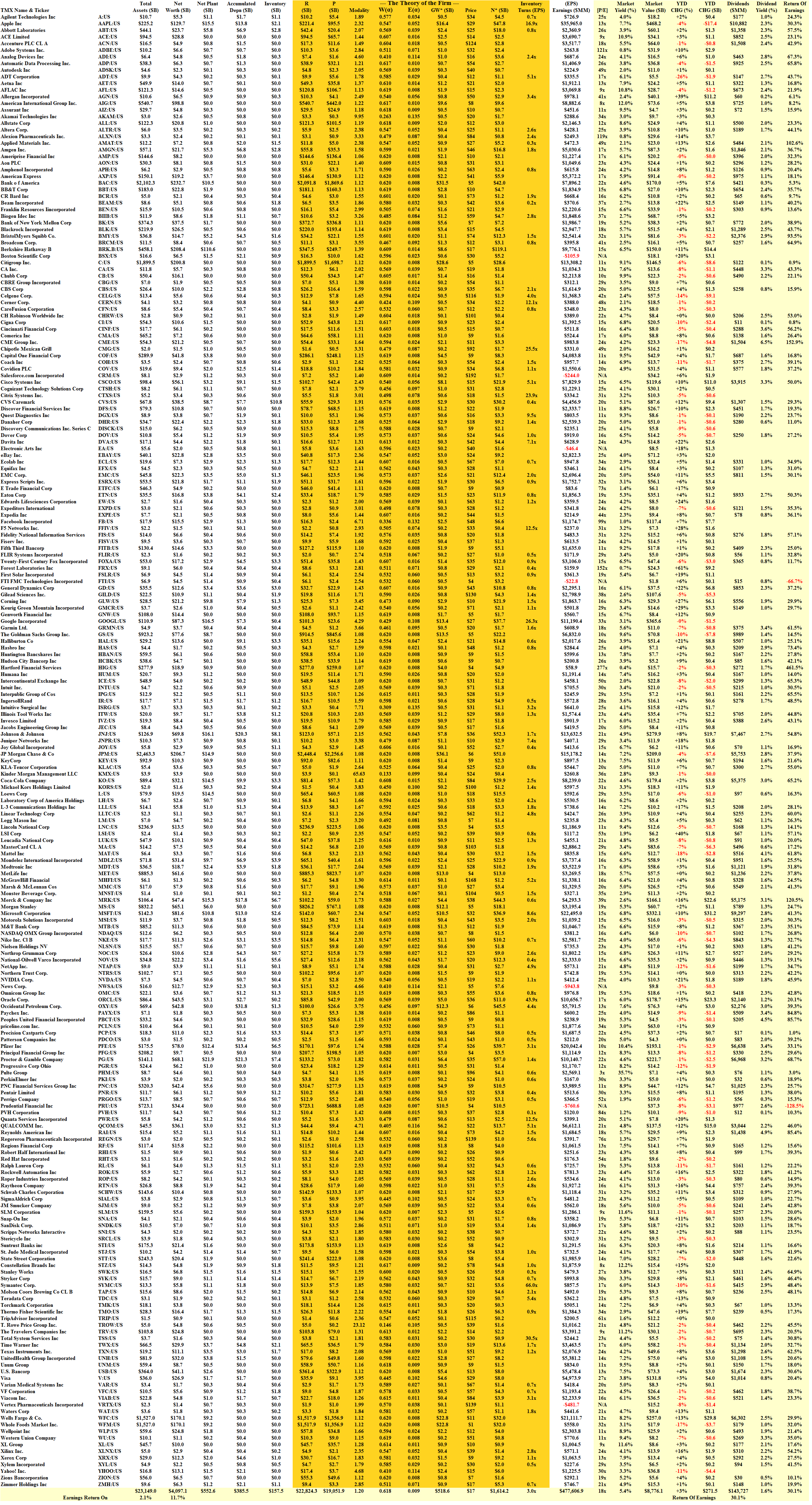

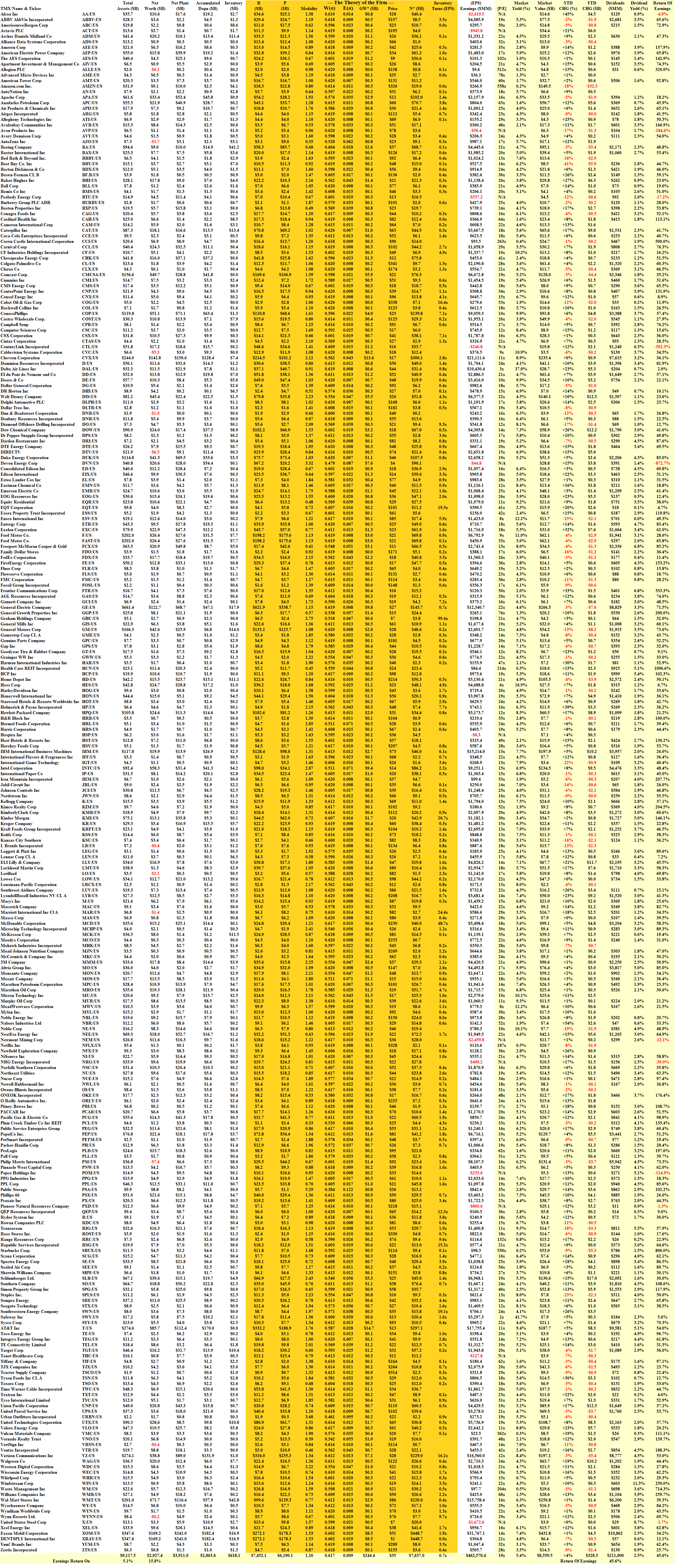

Exhibit 1: The S&P 500 Sidewinders – Fundamentals – April 2014

The S&P 500 Sidewinders – Fundamentals – April 2014

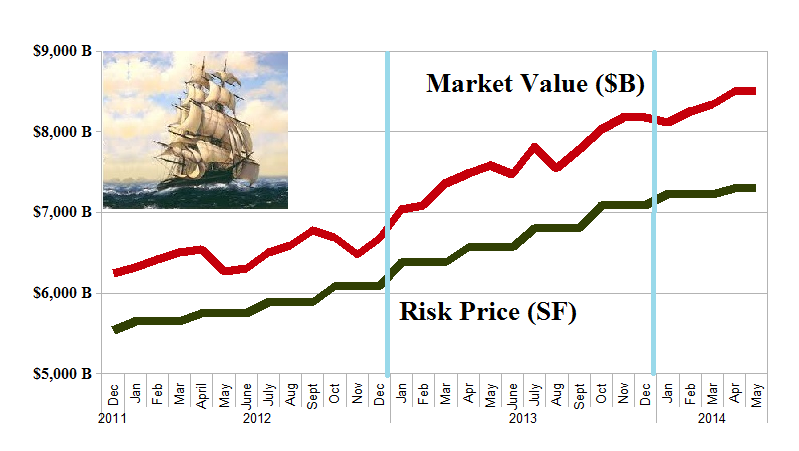

(B)(N) S&P 500 Sidewinders – Risk Price Chart – April 2014

(B)(N) S&P 500 Up-Winders – Risk Price Chart – April 2014

Both of these portfolios of companies did well in the stock market last year; the “Sidewinders” gained $2.1 trillion and +30% and the “Up-Winders” gained $1.5 trillion and +23%; they did even better in the equal-weighted cash-only Perpetual Bond™ where the numbers are +47% and +32% respectively.

But there are some differences that temper those results; the “Sidewinders” have demonstrated more volatility both this year and last year and they’re up only +3% so far this year; whereas the “Up-Winders” have demonstrated less volatility in general and they’re up +4% so far this year so that they have been able to keep more of the values that they gained and they are more likely to do so in the future because the “gap” is different.

The “gap” is the difference between the stock prices at the price of risk (Risk Price (SF)) and the market value and it is much greater and stays greater in the “Up-Winders” over that of the “Sidewinders” whose future is demonstrated by the “gap” in 2011 and 2012 before last year in which they were substantially boosted by the stock market enthusiasm to levels that they will not be able to maintain; if the market swoons or looses (20%) where should we think that will happen to a greater degree?

There are other differences as well that might explain why the stock market pricing of the “Sidewinders” is a triumph of hope over reality; and why stock market investors are so concerned over their most recent earnings reports and their forecasts; and why they might have reason to be.

For example, the “Sidewinders” returned +12% on the shareholders equity last year and paid 30% of their earnings last year for a dividend yield of 1.6%; but the “Up-Winders” returned +16% on the shareholders equity and paid 46% of their earnings for a dividend yield of 2.5% and there’s no reason to think that they might not be able to do it again this year and every year because (N*) the future is greater than (N) the present.

Investors are also willing to pay (whether they know it or not) $17 for $1 of the Coase Dividend in the “Sidewinders” but twice that amount $35 for $1 of the Coase Dividend in the “Up-Winders” even though the [P/E]-multiples are the same at 18× (please see Exhibit 1 above); but the Coase Dividend is always the “same thing” and measures the current “worth” in balance sheet terms of the “trading connections” of the firm which is the worth of its research & development, its patents and process, sales, marketing and administration benefits and the development of its production line (logistics and contracts for labour) and of the customers or markets for its products; in other words, it measures the “intangibles” and the ability of those “products” to produce earnings by working the matériel, so to speak, of the companies.

Sidewinders and Up-Winders

But the “Sidewinders” don’t have the wind at their back and they need to twist and slither a lot more in order to produce what they have; please Click on the links (and again to make them larger if required) “The S&P 500 Sidewinder Fundamentals” and “The S&P 500 Up-Winder Fundamentals” for more details on who they are and how big their problem is or is not.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice.

And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}