(P&I) The Process – The 1st Real Dollar

Essay. Most of us, and probably all of us at one time or another, have wondered where the “dollar” comes from, especially if we’re wondering where the next one is coming from. Mr. Einstein (Albert) has suggested that “compound interest” is a miracle, but most of us don’t have that insight and so, it’s just another day, another dollar.

Essay. Most of us, and probably all of us at one time or another, have wondered where the “dollar” comes from, especially if we’re wondering where the next one is coming from. Mr. Einstein (Albert) has suggested that “compound interest” is a miracle, but most of us don’t have that insight and so, it’s just another day, another dollar.

Which causes us to wonder where the first one came from? And now that a bar of gold, or a bushel of wheat (Adam Smith, 1776), is no longer the “gold standard”, how might we determine what it’s “worth”, other than by trying to buy something, for which we would be well-advised to know what it’s worth.

Figure 1: The 1st Real Dollar

Figure 1: The 1st Real Dollar

However, we can say that the 1st Real Dollar emerged when whatever preceded it was no longer an “investment” for those who had it, whatever “it” was then (or is now), but “it” was an investment for those who were willing to receive it, and give something else in return to those who accepted “it”, and offered a different “it”.

And that’s still true today, although negotiating skills were then, and are still now, a factor, even though things can happen much more quickly today than in the “old days”, and today, for example, we can use our cash, which is not an investment, to buy stocks which are, or could be (please see below).

Since we’re dealing with 1st princples, we ought, first of all, to know that an “investment” is just and only the “purchase of risk”, and, accordingly, if there is no risk, it’s not an investment, although “risk” alone does not make it one either, until we know what “risk” is.

The “risk” that we’re thinking about is that we might not be able to sell it for the same or more than we paid for it, which is why we have only three rules for making an “investment” and “buying risk” – we want 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation which, if we don’t get it, is just another way of losing our money, for which the “market” has developed even more ways.

But those are the words that move us – safe, liquid, and hopeful – and if we don’t hear those words, it’s just a gamble, and falls short of what we want in the “purchase of risk” (although not everyone agrees with that and Wall Street has a different view of “risk”).

We’re here. What have you got for us?

Although Figure 1 looks like a “sail boat” from this distance, and might have been one, approaching the coast of England more than a thousand years ago, we’ll also need to go into the “corner” at (0,0) and (1,1), but it’s in the long view from which the 1st dollar emerged, not just for six and seven, as shown on the chart, but in the even more distant, log(1/a) = +∞, when we had “nothing” (a=0), and they had “everything” (b=+∞), but it was “worth” nothing (log(1/b) = -∞), because nobody else wanted it, or could get it without a sword – and they had food, wine, tools, fabrics, numbers, letters, … and, eventually, they learned how to use a sword, too, and levelled the playing field.

Indeed, you are the one we want.

So, the 1st real dollar emerged when we began to accumulate some a>0, and it was decided that it was “worth” (1) when “they” took it and gave us a (1), which we also agreed was a (1), at that time, and satisfied our disparate interests.

To be more precise, we developed “payables” (a) because we were building something, or making something, or we had a service to render (such as “arms” and “weaponry”), and while we were doing that, the “trading connections” developed (b), a “package” or set of “receivables” to us, but “payables” to them, took notice, and eventually they decided that what we had was worth (1) to them, and we decided that what they had to give us was “worth” (1) to us.

Hence, at the point of exchange, a=b=1, and log(1/a) = log (1/b) = 0, and that’s a “fair deal” because the “risk of ownership”, which is 1 – log(1/a) and 1 – log(1/b), was equal, and “total” and 100% for loss on both sides of the trade, and to reverse that “fact” of ownership, we needed to do something with what we got, and they needed to do something with what they received, although chances are they had a lot more of (b), but we had only one (a), and it was gone! So we had to make more.

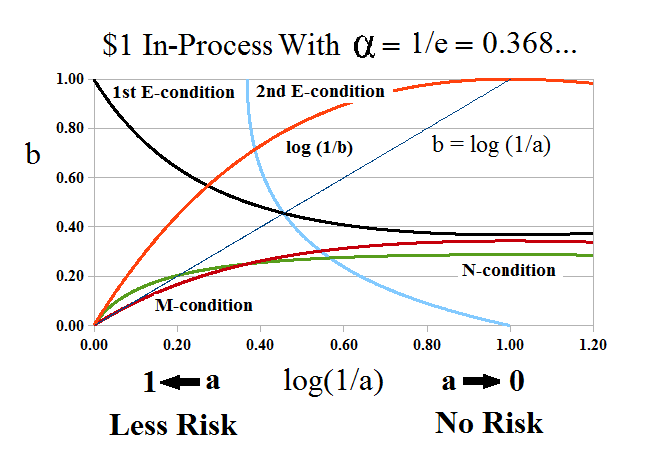

Figure 2: The 1st Real Dollar In-Process

Figure 2: (a) and (b) in-process

But we are hopeful that what we received would help us to produce more (a), and we know how to do that with whatever materials and skills we have left – we surely didn’t give them everything for their (1), of which they seem to have so many more; please see Figure 2 on the left, and note that our post-trade starting point is near (0,0) after nearly (1,1), and the difference between (1) and (0) is influenced by our negotiating skills and the opportunity to use them (please see below).

This chart is the same as the one above, but it’s in the corner at, (0,0) and (1,1), and we’ve added log (1/b) (red line), and the M- and N-conditions, which will help us to decide how we trade in the future, now that we know what’s wanted, and how much they’re willing to pay for it.

A Call To Arms

The chart is also for the modality, α=1/e (Company D), which describes a “subsistence economy”; please see our recent Post, “(P&I) The Process – The Guns of August” for more information on that, and how governments tend to dwell in that space, and can’t leave it unless there is a state of “emergency” that will be paid-for by the “governed”.

In the chart, the trade at a=b=1, created the “benchmark” for our dollar, and it is represented at (0,0) which is log(1/a) = log(1/b) =0, for which the “fair value” is, a=b=1; also, b=1 is in-process in the 1st E-condition (black line, upper left), a×log(a) = α×log(b), and the 2nd E-condition (blue line), b×log(b) = α×log(a), both of which are represented in the co-ordinates of log(1/a), which is the “capitalization rate” of the set of payables, (a), with a=p((a)), as usual, and our business and that of the trading connections, has now developed – after many trades – to a σ-algebra, (N), of possible sets of payables, (a), and receivables, (b), that are in-process with respect to the 1st and 2nd E-conditions, which, at the end of the day, will help us to decide what “things” are really worth as we trade more and more of them; please see our Post, “(P&I) The Process – Commensurability” for more information on what these sets are really like.

We also note that as a→0, we have “No Risk”, whereas as a→1, we have “Less Risk”, and it might be hard to understand how “Less Risk” could be better than, or preferred to, “No Risk”, because our object is to increase our set of payables from 0=a=p((a)) to 1=a=p((a)), for different sets (a), of course, of which the latter is “larger”.

With reference to Figure 2, above, the reason is that if a<1/e, and (a) “gets smaller”, and even as a→0, in-process, the implementing sets of receivables, (b), are such that b=p((b))→1, even as a→0; hence, “No Risk”, for the producer, but lots of risk for the trading connections, for which the receivables are growing and not being paid-out with “receipts” from the producer, absent receivership which is a controlling factor in that relationship, at that stage of the “production”.

On the other hand, if a=p((a))=1/e, then log(1/a)=1, and b=p((b))=1/e=0.368, as well, and as, a>α=1/e, and a→1, the receivables sets grow as b×log(1/b) = α×log(1/a) < a×log(1/a) (2nd E-condition), so that “a” is always “out-of-pocket” until they deliver at a=b=1, and not before; hence, a→1, means “Less Risk” for the producer and the trading connections, and the “risk” only begins at a=1/e, or log(1/a)=1.

Also, in the same context, both (a) and (b) are “fully valued” at a=b=1/e, with “capitalization rates” 1=log(1/a)=log(1/b), and “risk” only sets-in when a>1/e, and it can be defined as “risk” = 1 – log(1/a), which is positive if a>1/e, and negative if a<1/e, and zero if a=1/e.

Clearly, there’s a lot going on before we can “do the deal” and count our money, but, despite the equations, it’s intuitive and informed by the “societal standards of risk aversion and bargaining practice”, for which “volatility” has no credibility in the common-sense of “things”, and is nothing more than a trivial mathematical legerdemain for which the “market” has developed no sensible response; please see our recent Posts, “(B)(N) The Market At Rest” or “(P&I) Bubblemania and The Working Poor” for more information on this.

The (Real) Risk Equations

The M-condition, 1+log(a) = lim (1/b^α)×log(1+b^α) as b→0, and the N-condition, 1+log(a) = -lim(1/b^α)×log(1-b^α) as b→0, are then the “risk equations”, because the left-hand sides are equivalent to, 1+log(a) = 1 – log(1/a).

Hence, “Trading Connection Risk” (M-condition) – “Producer Risk” (N-condition) = (1/b^α)×log(1+b^α) + (1/b^α)×log(1-b^α) = (1/b^α)×log(1-(b^α)²) <0 for b→0 as a→1, and we need both conditions (both b→0 as a→1, or b→1 as a→0), because, in general, the sets a=p((a)) and b=p((b)) are not the same in both equations (and so it doesn’t simplify in that way for all (a) and (b), which are symbols and not facts), as can be seen in the chart (Figure 3) below, but the difference is made to nearly vanish at the point of trade, that is, at a=1 and b=1, although it cannot vanish entirely, else there would be no profit, and a hopeful return above the rate of inflation.

Figure 3: The Real Risk Equations

Figure 3: The Real Risk Equations

We can see from the chart that the “Trading Connection Risk” (red line) was greater than the “Producer Risk” (green line) when the payables are accumulating at log(1/a) near 1, but the “receipts” against, or payments to, the receivables aren’t.

However, the tables are turned as a→1 and b→0, and the “Producer Risk” begins to exceed the “Trading Connection Risk”, and the producer has developed payables near one, and the trading connections have developed receivables near one, to effect the trade, which ends with (a) and (b) near zero, but not at zero.

We also note that in the remote past, when a→0 and log (1/a)→+∞, the “Producer Risk” tended to exceed the “Trading Connection Risk”, because at that time, they weren’t trading, and the producers were producing products for which they did not yet have a customer.

Contract

It’s not surprising, then, that “buyers” in a subsistence economy, have “bargaining power” and that, eventually, the “pen is mightier than the sword”; on the other hand, there is “bargaining power” on both sides of the equation, and the “producer” might need some help to get past the “death embrace” at a=b=1/e with modality α=1/e, for which the producer and the trading connections have similar interests; please see our recent Post, “(P&I) The Process – End of Process (E,C,D)” for more information on that and how the trading situation is resolved at the end-of-process.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.