(P&I) The Process – The Guns of August

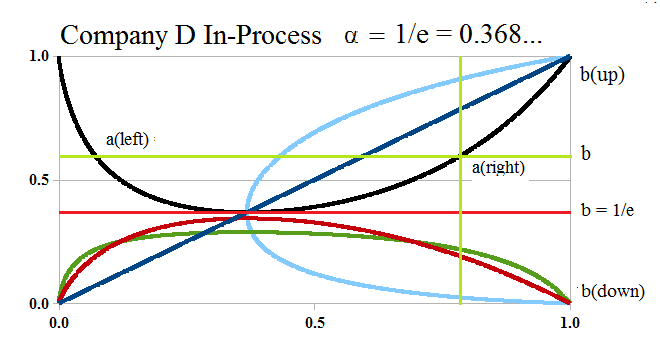

Figure 1: Company D In Process

Essay. We noted that in the case of Company D (α=1/e), with modality, or entropy, α=1/e, there are no implementing sets, a=p((a)) and b=p((b)), that would help us to leave the “death embrace” at a=b=1/e; please see Figure 1 on the right and our recent Post “The Process – End Of Process (E, C, D)” for more details.

Although the company and its trading connections are in-process at that modality, and with those sets, there is nothing, absent some “event” that is out-of-process, that will help us to leave, assuming that we want to leave.

The Guns of August

Courtesy: Barbara Tuchman

After all, we could dwell there forever by simply exchanging one set of payables and receivables for others, all of which differ by events of probability, or measure, zero, and are not “large” enough to move us to another place.

But, they don’t “produce” anything either – there’s no “product” – and payables and receivables just move from one pocket to the other, and back again, and again, and again … and they don’t “grow”, because they’re like “cash” (please see below).

And when we put it that way, we are minded of “governments” which usually dwell in, or inhabit, that space, and can’t leave it other than by war, civil or otherwise, pestilence, or debt-default, only to return to it another day.

We are compelled, therefore, to look at this space more closely, because those events are not at all uncommon, and the solution is “economic”, and not war, and not debt-default; please see Exhibit 1, below, and the explanations to follow, which we’ll try to present with “excessive” clarity.

Exhibit 1: The Guns of August (2014)

Figure 1.1: Company D In-Process |

Figure 1.2: Company D The Guns of August |

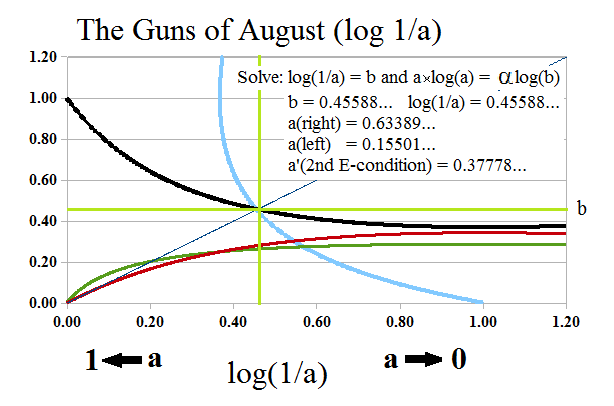

Figure 1.3: Company D The Guns of August log(1/a) |

The chart on the left (Figure 1.1 and please click on it to make it larger if required) shows what our problem is – there are no implementing sets that will help us to move our “production” from a=b=1/e to a(right) and b(up), and closer to the end-of-process, at a=b=1, in which we can exchange some “tangible product” as a result of our “production” in-process, while we still remain in-process with that modality, α=1/e, which is (generally) hard to change.

And, possibly, that’s just the way that we do the “business”, because the “death embrace” describes a “cash”, or even a “barter” economy, because log(1/a)=log(1/b)=1 (100%), and, therefore, there’s no risk in our payables and receivables, meagre as they are, and no credit, either.

Nor is the problem “academic” because governments always dwell in that region of modality; the reason is that if R is “what is owed to the government”, and P is “what the government owes” (its total liabilities), then it is typical that α = R/P<1/e=0.368…, signifying that the government “owes” about 3× what is owed to it, and the “situation” is often even more strenuous, and the government might owe 4× or 5× or more, than what is “owed to it”, particularly in times of war or other national emergency that will tend to increase the debt-burden, but not the realizable receivables.

The Cash Economy

And that is what we find in the balance sheets of most governments, today, and the political “craving” for a “balanced budget” just makes it worse, and it is the hallmark of an emerging “cash economy” with a high rate of under-employment.

However, problems like these are a “Company A”-problem in which the modality α<1/e; or even a “Company B”-problem in which the modality is 1/e < α <1, and they are commonplace in business because most companies are started-up deeply in debt, and some companies just operate that way; for example, the aggregate modality of the Dow Jones Utility companies is α=0.79 (Company B), and there are three companies in the Dow Jones Industrials with a similar modality (Home Depot α=0.84, Wal-Mart Stores α=0.75, and the Boeing Company α=0.68) although the aggregate modality of the Dow Jones Industrials is α=1.25 (Company C), and there are relatively few companies that operate with modality α<1/e = 0.368…, indefinitely, the exception being “real estate companies” that service debt from rents, and have a typical modality in the range of α=0.20, or less.

We have also shown in the Theory of Firm that it is quite reasonable – and “mandatory” in an economic sense – for a new company to be funded with (roughly) 40% equity, 60% bond-debt, and a “working capital loan” of 25% of the combined equity and debt, which we call the “N/B/W”-financing model at “40/60/25”, and the modality of such a firm is α= 0.40 × (1-0.25) = 0.30 < 1/e = 0.368… .

But a lot of debt is not a problem if it is an opportunity, that is, if the debt can be funded and used “productively”, and for that we need more than just “subsistence” levels of payables and receivables production that merely “change hands” and only look like a “production”; we need them to tend to one (1), and engage everyone in the “production space” (payables) and the trading connections (receivables); that is, we need them to tend to one (1), and not just lurk in the “basement”, so to speak.

Moreover, “capital” that is deployed in the “death embrace”, is not “productive”, because the “capitalization rates”, log(1/a) and log(1/b), are 100%, and there’s no reason that it should “grow”, because it’s just “cash” – there’s no risk, absent inflation (and banditry), and no credit.

Are you the one?

The government could tax us more, and raise the level of “what is owed to it” more permanently, and possibly even reduce what it owes by paying-down its debts, or not accumulating new ones, and “ascend”, so to speak, to the Company B- or C-level, which is commonplace in mature industrials, but these latter have “earned” it, and know how to maintain it, without just reaching into somebody else’s pocket.

However, because the government will tend to maintain its modality, we – as business people and citizens – can suggest another way in which the “risk” of additional debt to fund “growth” is shared fairly between the government and we, and, at the same time, help the government to “produce” some tangible product in the working of the economy that makes the debt more “recyclable” and “productive”, and likely to be paid-back.

For a closer look at this, please see Figure 1.2, above, which focuses exactly on the problem at a=b=1/e with modality α=1/e, and, for the solution, Figure 1.3, above, which re-states the problem in terms of the capitalization rate, log(1/a) and log(1/b).

Our object, in Figure 1.2, is to move the production to a(right) > a = 1/e, and b > 1/e, so that we might have a chance at a(right) → 1, and b(up) → 1, and move the production process towards the “end-of-process” at a=b=1, even though we can expect that our modality will remain at α=1/e, or so.

Figure 2: The Solution

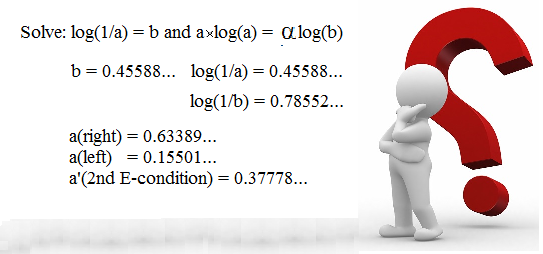

The reason that there is a solution is that there is exactly one level of payables, a=p((a)), and receivables, b=p((b)), for which the capitalization rate of “a” in-process is equal to “b”; please see Figure 1.3, above, and the table in Figure 2 on the right.

What that means is that in this modality (α=1/e), in-process, there is always a set of payables, (a), with measure a = p((a)) = 0.63389, with a “capitalization rate” of log(1/a) = 0.45588 (46%), that “commands” a set of receivables, (b), with measure b = p((b)) = 0.45588, with a “capitalization rate” of log(1/b) = 0.78552 (79%).

In other words, although the liabilities (or payables, (a)) are at-risk with a capitalization rate of 46%, and are much higher at a(right) =p((a(right)))=0.63389, they are matched by a set of receivables, (b), with a capitalization rate of 79%, and b=p((b))=0.45588, that is much larger that b=1/e = 0.368.

Since the “unit” is undefined in this context, it’s best to think in terms of percentages; the debt at (a(right), b) is increased by 72% (0.63389/0.368) with a capitalization rate of 46%, and the receivables are increased by 24% (0.45588/0.368) with a capitalization rate of 79%, all of which are better than 0% with a capitalization rate of 100% (certainty).

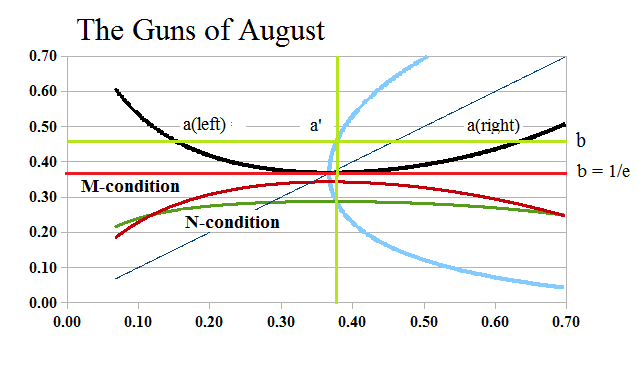

Figure 3: Company D The Guns of August

However, we should not be expected to empty our pockets and lend $12 trillion (+72%) to a government that already has a debt of $16 trillion, for example, because there is also a path to growth that increases the receivables by 24%, as indicated, but the debt by only 2.7% (0.37778/0.368), that is indicated at (a'(2nd E-condition), b), and is just a little to the right of the “death embrace”, and such (a) has a capitalization rate of log(1/a) = 0.97344 (97%), and looks just like “cash” even as the receivables are increasing by 24% with a capitalization rate of 79%; please see Figure 3 on the left.

But, if we like a’ and a(right), so much, why not a(left) which reduces the payables by 58% (0.15501/0.368) and has a capitalization rate of log(1/a(left)) = 1.86428 (186%), and is still good for (b)? That’s true, but the capitalization rate suggests that it creates “negative cash” and, therefore, a currency devaluation.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.